We begin this piece thinking that the reader has had the opportunity to peruse our earlier article on www.modernghana.com on “Agyapa Royalties Ltd: The Myths Surrounding Agyapa Royalties – Is it a case of Good Strategy but Wrong Tactics?” If you have not, please appraise yourself on that via this link

Read More: Election2004: Bagbin to run; Mahama may Not

Today we want to take the reader through the mundane but not too complex world of a Special Purpose Vehicle (SPV). To emphasise, it is a company or a corporate entity just like any limited company you know. It is not a mythical construct at all. In Company law, a company is a legal person as opposed to a natural person like you and me. A company has a date of incorporation, country of incorporation, place of operation, shareholders, share capital (equity and or debt), source of funds, directors, management, amongst others.

Now that we have managed to demystify the concept of an SPV, we can proceed to explain a few things.

Why Do We Create Special Purpose Vehicles/SPVs?

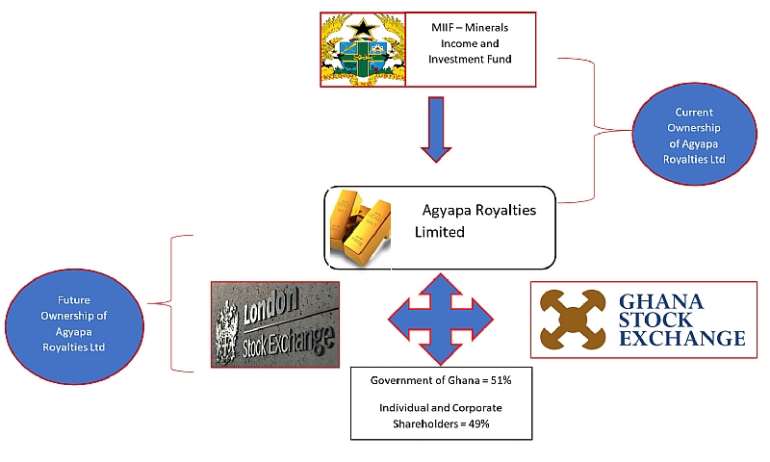

SPVs are usually created with a specific objective in mind. In the case of Agyapa Royalties, the primary reason for its creation is that; The Government of Ghana (GoG) wants to monetise its mineral royalties received from Mining companies operating in Ghana. By law, the Minerals Income and Investment Fund (MIIF), is the recipient of these royalty payments on behalf of the Republic of Ghana. The GoG through MIIF, has set-up Agyapa Royalties Ltd as a company. This new corporate entity will now be the custodian of all future royalties. Currently, the GoG owns 100% shares in Agyapa Royalties Ltd through MIIF.

The GoG wants to divest 49% of the shares it currently owns to investors. It wants to list these shares on the London and Ghana Stock markets. Ghana hopes the funds generated from the sale of shares of Agyapa will be for investment purposes. That in essence sums up all the cacophony there is to know about Agyapa, nothing more nothing less.

Orphan and Non-Orphan SPV’s

There are two types of SPV, an orphan and non-orphan SPV. An orphan SPV, Ogier Global (Jersey) Ltd. According to the Jersey Register of companies, the registered address of Agyapa Royalties Ltd is also the registered address of its nominee company Ogier Global.

Ogier Global (Jersey) Ltd apart from acting as the management, and corporate directors, they are the nominee shareholders of Agyapa. As nominee shareholder, they are the Legal Owners of Agyapa Royalties Ltd. As legal owners they hold the shares in trust for MIIF or GoG the Ultimate Beneficial Owner (UBO). Usually, the shareholders of an Orphan SPV are not known. In the case of Agyapa, we know of the UBO, because the GoG has openly declared that it is the 100% owner.

A nominee company usually specialises in Trust services. They tend to be accounting or law firms who assumes the shareholding and management of other corporate entities including but not limited to SPVs. The person who sets up an SPV is known as a Sponsor or Originator. In the Agyapa SPV scenario, the GoG, through the Minerals Income Investment Fund (MIIF) is the Sponsor or Originator.

With regards to Agyapa, the GoG through MIIF will, transfers its assets i.e. Royalties to Agyapa. Agyapa in turn will receive these payments or royalties as its Source of Funds per annum. The liabilities of Agyapa will therefore be on the books of Agyapa as it is a separate entity from that of the Republic of Ghana. To re-iterate any debts and liabilities of Agyapa will be Agyapa’s liabilities only and not that of MIIF or the Republic of Ghana. The Republic of Ghana in turn will not guarantee any debts of Agyapa.

On the other hand, a Non-Orphan SPV is created if the entity continues to be part of the Originator’s corporate group. Were the GoG to guarantee the liabilities of Agyapa Royalties Ltd, and assumed responsibilities for its assets and liabilities, then Agyapa will be classed as a non-orphan SPV.

The ownership Structure of Agyapa reads as follows for the purpose of illustration.

Ownership Chain of Agyapa Royalties Ltd

THE GOOD

Many established companies around the world use SPVs. Some use debt and others use equity SPV to raise capital. The funds raised are used to fund acquisitions and growth. Other times they are used to make repayments as per the purpose of which they have been set up for.

Should the Initial Public Offering go well as planned, the GoG will be able to raise between $500 million to $1 billion. These funds will enable the government to carry out its strategic objectives of raising funds to execute infrastructural projects.

GoG will have another avenue to generate extra revenue for development as and when dividends are paid to shareholders of Agyapa Royalties Limited

Looking at the Structure of Agyapa Royalties Limited, as an Orphan SPV, its activities will not reflect on the books of Ghana. If anything, it will show that GoG owns 51%, and may be receiving dividends from time to time. Any future shares that are sold by the GoG may also reflect as Income for Ghana. Ghana will not be liable for any liabilities save our annual royalty payments to Agyapa.?

Furthermore, whilst the liabilities of Agyapa will not be on or in our books, the GoG will have enough room and leeway to raise extra funds on the capital markets. Indeed, Agyapa Royalties, will free up space on the national budget for Ghana to raise funds for development, without it affecting Ghana’s bottom-line.

In the unlikely event that Agyapa Royalties Limited as a company fails, the shareholders including the Republic of Ghana will not be saddled with any more liabilities. As a company with a distinct and separate personality, shareholders liability is only limited to their investments. There will be no knock-on effect on the Sovereign risk-rating of Ghana. On the flip side, any future appreciation and demand for Agyapa shares could only swell the coffers of Ghana. No matter how you slice and dice this vehicle, it is a win-win situation.

Within the realms of regulation, Agyapa has to comply with the Listing Rules and disclosure standards of the Financial Conduct Authority in its capacity as the UK Listing Authority (UKLA). These rules are very stringent, and they cover a whole gamut of Due Diligence requirements. If Agyapa manages to clear the UKLA hurdle, it then has to comply with the London Stock Exchange’s Admission and Disclosure rules, as another round of Due Diligence. After these two limbs have been fulfilled, Agyapa will be able to float shares on the London Stock Exchange. It will now become a Public Limited Liability Company, with the moniker ‘PLC’ attached to it.

For people who have been shouting from the roof tops, once Agyapa Ltd is listed on the Stock Exchange its activities will be subject to strict scrutiny. It must subscribe to the transparency and disclosure standards of the FCA-UKLA and London Stock Exchange. Agyapa Royalties PLC must abide by its on-going commitments and obligations to submit information that is accurate and timely to market participants. Furthermore, the company has to subscribe to applicable UK and Jersey laws in addition UK Corporate Governance and takeover Code.

Back here in Ghana, Agyapa intends to list on the Ghana Stock Exchange. It must comply with provisions of Company law in Ghana, The Listing rules of Security and Exchanges Commission, Ghana. It has a duty to abide by the admission rules of the Ghana Stock Exchange. Not least, Agyapa also must subscribe to other regulatory regimes and framework including Bank of Ghana and other statutory regulators.

Even though it may not be listed on any American bourses, if any statements and representations are made to American entities and individuals, then Agyapa PLC may be subject to the provisions of US Securities Act 1933 sections 10b -5 , 11 and 12.

Under Rule 10b-5, It is unlawful for any person offering the purchase or sale of any shares to make truthful statements and representations. Statements and representations made must not be misleading, and they ought not to omit any material facts and engage in fraud or deceit. Under Section 11 of US Securities Act of 1933 - which deals with False registration statement(s). Liability arises if the contents contained in a prospectus are untrue and a statement of a material fact is also omitted which should have been included. Under Section 12 of US Securities Act of 1933, a buyer of shares can sue any person who both offered or sold the underlying shares to a buyer in violation of section 5 of the Securities Act.

These rules are designed that any person involved in the production of the prospectus or offer document will be held liable for any acts of omissions, misrepresentations fraud and deceit.The list is exhaustive and may include directors, management, accountants, lawyers, under writers and any person both natural and legal person (entities).

Companies listed on the London and Ghana Stock Exchanges also have a series of actions that they must comply with as part of their Continuing Obligations. Companies have of Disclosure to the stock market on Inside Information, Significant Transactions, Related Third Party Transactions, Substantial Property Transactions. Meaning that such information should always be made public. Minutes of board and shareholder meetings should be recorded and filed appropriately.

Directors, employees and connected persons must refrain from: Insider Dealing, Market Abuse, money laundering, fraud, and a host of financial and economic crimes. Failure to adhere to these directives will elicit criminal prosecution, civil enforcement, fines and sanctions under United Kingdom and Ghanaian law.

Under UK law, directors both Executive and non-executive owe a fiduciary duty to Agyapa. Their job entails that they must do everything within their power to ensure that Agyapa succeeds. They must exercise reasonable care, skill, knowledge, and diligence in furtherance of the objectives of Agyapa.

As a listed Company, there will be no political Interference in the affairs of the SPV. Any change of Government in Ghana or anywhere else will not affect the operations of Agyapa, save as a shareholder, the GoG may want to either appoint directors or partake in actions within their capacity as shareholders. However, any actions will be subject to UK or Jersey and Ghana law, FCA and London Stock exchange regulations as well as Agyapa’s own byelaws and Articles of incorporation.

Normally the CEO will, and a few members of the board will be part of the day to day operations of the company and are the management. The Shareholders of Agyapa is GoG (51%) and the other 49% will appoint the Board of Agyapa. The Board will exercise complete oversight of Agyapa and is answerable to the shareholders. The Board will usually be headed by a chairman and there will be executive and non-executive board members.

These Executive directors will be employees of Agyapa. They will have a specific role (such as finance director etc.) and as such will be responsible for day to day running of company. The Non-executive directors however are not employees of the Agyapa. They will be appointed for their expertise and as such will be required to constructively challenge and help develop proposals on strategy.

Having enumerated these points above, we as writers believe that we have allayed and assuaged any concerns that Ghanaians and any potential investors may have. There is no myth to the Agyapa story. It is all plain and sailing and should be sufficient to allay any investor concerns.

If everything were to work well, the SPV as a template could be replicated to raise funds for sectors in Ghana like a proper Public transport network which is primed to a be a multi-billion-dollar industry. The issue of Public transport opportunities and possibilities will be discussed in a future article by us. If done right, Agyapa Royalties Limited, could ensure that Ghana will experience a boon and will be the yardstick for future development in different sectors of the Ghanaian economy.

THE BAD

Like all human endeavours, best laid plans are always wrought with bottlenecks. Our sojourn, on the Agyapa Special Purpose Vehicle, has encountered a series of roadblocks.

As Richard Withington of Said Business School, University of Oxford opines, Strategy must be communicated period. We must add for emphasis, that not only must all best intentions be communicated, it must be well-understood by all stakeholders.

The brouhaha surrounding Agyapa is due to lack of communication and stakeholder engagement. As Dr. Ekow Spio-Garbrah has rightly stated, the government of Ghana lost the PR war. Had the government engaged enough with the people, all niggling concerns could have been laid to rest. As things stand the average Ghanaian does not understand what Agyapa all is about.

Agyapa has also been criticised for its lack of Openness. Until a few weeks ago, not many corporate finance lawyers, practitioners and financiers were aware of such an initiative. Ghanaian professionals are crying out for more information on the ins-and outs of the Agyapa SPV.

Even when GoG made amendments to the MIIF Act, it did so through a certificate of urgency in the legislature. The GoG sought to railroad the SPV without much public consultation and discussion. Civil society groups and the opposition parties are demanding answers on series of questions. As we speak, those issues have not been resolved.

Furthermore, names have been peddled as managers and directors of Agyapa. When these names were mentioned, we have had officials at the ministry of Finance saying that a thorough process of recruitment took place. And these individuals were selected based on their expertise and qualifications. We are not able to say, they are not being truthful.

We have perused the profiles and credentials of the individuals whose names have come up. At this moment we will not discuss whether they are qualified or not. As regulatory professionals we are much more concerned about the impact of Politically Exposed Persons (PEP) the ongoing regulatory Due Diligence.

In Financial Regulation, a person is classed as Politically exposed if he holds a significant public position or function. Such individuals are deemed to be susceptible to bribery and corruption. The concept of RCA -Relatives close Associates also comes in to play. Where a person is close to a public figure whether as a relative, friend or close associate, such individuals together with the Politically exposed person are deemed to be high risk. Considering that Banks and regulators are involved as part of the mechanism for listing on the stock exchange, it will be more prudent to make appointment with PEP and RCA considerations in mind.

Share prices of companies on bourses are extremely sensitive to politics and economic vagaries. As a soon to be listed company where the GoG will still retain about 51% of ownership, indeed there will be a political cloud hanging over Agyapa. How to manage the politics as a people will very much weigh on the share price. We can extract much value from this vehicle if we keep political considerations to the barest minimum.

The Ministry of Finance has not managed to comfortably educate Ghanaians and to show us the prospectus and how they arrived on the final valuation. We as a people therefore are only caught in a circle of speculation. As writers, we have previously queried, the financial strategy behind Agyapa. We have stated in our previous article that, Agyapa is Good Strategy but with wrong Tactics. We floated suggestions that the GoG, could get a better deal by doing the following:

‘‘Different Classes of Shares -The shares owned by the Government of Ghana could be given a different class let’s call it ‘’Class A or Golden Shares’’. And this represents 51% of Agyapa. Investors on the other hand will own Class B shares, which they can purchase via the stock market.

Voting Rights - The Class B shares could also retain 24.5% voting rights, which is a dilution of their 49% free float, that is stock market listing. Class A shares of the Government of Ghana will then retain voting rights of 75.5%.

Dividends - Class B shares should be non-dividend paying. That is the prospectus or offer document should clearly state that no dividends will be paid to shareholders for a given time, say 5-10 years or not all. (Manchester United did not offer investors any dividend repayment during their IPO on the New York Stock Exchange).

Investors will be able to sell their shares minus dividends. The value of their shares will appreciate or depreciate based on the vagaries of demand or supply and the underlying value of the Company and its cash flow.’’

THE QUESTIONS

The Attorney general has raised questions on ‘’conscience’’ and “perpetuity”. How did the Transaction advisers resolve and assuage those concerns? Even after The Attorney General’s questions and opinion were leaked

Why is the Attorney General’s department not in charge and taking the lead as the Advisor- in chief with regards to this deal? Are there not competent lawyers in that department to draft and execute such a deal? How resourced is the Attorney General’s department?

We have not been told how much the transaction Advisors charged. We have not been told in full who the transaction Advisors are, and how we procured their contract for services. We have only had wind of local personalities and law firms involved all because of political talk, and not out of a genuine desire to share information with the public.

On the issue of invoices paid to local firms, we have only heard a few government-friendly media personalities telling us that they have seen the invoice. As regulatory experts and financial crime professionals, which firms in the chain made the payments to the local firms? If payments were made from firms involved in the deal, it is all well and good. But if third party firms are involved, then we should raise questions on why they are involved.

Since the GoG has decided to incorporate Agyapa in a tax haven, and not in Ghana, whereas government, they could have given the SPV all the tax incentives that Jersey provides. How can we say to future investors that Ghana is ripe for business when we do not even believe in ourselves?

How effective will the GOG be in combatting tax avoidance, if it is also complicit in such schemes? As Writers we believe, the Government of Ghana has missed a fine opportunity to advertise Ghana as a good investment destination and one with a competitive tax regime.

We can look at Ashanti Goldfields Corporation (AGC) to give us an insight to how things could have been, had Agyapa been set up in Ghana. AGC was incorporated in Ghana, had its operations in Ghana and yet still managed to list on the London and New York Stock exchange (first African Company to do so) and was the goose that lay the golden eggs for years, question is why can’t Agyapa follow in the foots steps of AGC?

We have heard in the grapevine that Agyapa may either have a subsidiary or branch, and an office in Ghana. From sources, Ghana may become the operating jurisdiction for Agyapa, their offices in Jersey may only serve as a corporate hub. If this information proves to be correct, then it re-enforces our opinion above that there was no need to set up in Jersey. The tactics as opposed to Strategy is wrong from the beginning.

Conclusion

We hope our readers have enjoyed the ride and walk through on Agyapa as a Special purpose Vehicle. Countries like Canada, US, India have set up SPV to manage acquisitions and to raise capital which has been to their greatest advantage. We as a country can follow these great footsteps and help Ghana to raise enough funds for development. As a vehicle, we can replicate its success and learn from its failures also.

We should do our best to learn lessons from Enron and its demise. Enron set up a SPV where they were able to hide their losses from investors. In the end the house of cards tumbled, and it led to fraud and regulatory infringements. In a n increasing dynamic world, Ghanaians should encourage creativity and innovation. We should endeavour to provide 21st century solutions to 21st Century problems. Special Purpose Vehicles, and Special Purpose Acquisitions Companies can go a long way for us to raise funds to for instance resolve issues like Okada and to build a robust and efficient transport network. For now, the once Gold Coast must start with Gold, and our Gold resources and mineral royalties could be the keys to unlock our hidden gems and possibilities. Like the first iPhone, Agyapa may not have started off very well, but we hope it becomes a cash cow and a resounding success for the good people of Ghana.

Written by Kwadwo Kusi-Frimpong, a Financial Crime, Governance and Regulatory Expert, who has extensive experience working with banks and financial institutions in UK, Switzerland, and The Netherlands. He holds an LLM from University of Law and is a graduate of University of Ghana and Said Business School, University of Oxford. Affiliate member of (ICA) International Compliance Association.

George Amparbeng is a Financial Crime, Governance and Regulatory Expert. He has experience working for Banks in UK and Europe. He is a Graduate of University of Ghana and associate member of ICA (International Compliance Association).

Emmanuel Ghunney (MSc), a Securitisation and Regulatory Reporting SME, with extensive experience working with leading Investment Banks in London, Switzerland, Netherlands and Paris.

The team can be contacted at: [email protected] and [email protected]

GTEC questions dismissal of Bolgatanga Technical University Vice Chancellor

GTEC questions dismissal of Bolgatanga Technical University Vice Chancellor

'You can't come and abuse Ghana's resources and run away to avoid accountability...

'You can't come and abuse Ghana's resources and run away to avoid accountability...

Dr. Adutwum Campaign Aide appeals for calm as Ken Agyapong row deepens

Dr. Adutwum Campaign Aide appeals for calm as Ken Agyapong row deepens

Mahama demands strict quality checks before road payments

Mahama demands strict quality checks before road payments

Turmoil in NPP as Ken Agyepong supporters blast executives over alleged dismissa...

Turmoil in NPP as Ken Agyepong supporters blast executives over alleged dismissa...

June 27: Cedi sells at GHS12.30 on forex market, GHS11.30 on BoG interbank

June 27: Cedi sells at GHS12.30 on forex market, GHS11.30 on BoG interbank

Odaw River dredging to be completed by December 2027 — Works Minister

Odaw River dredging to be completed by December 2027 — Works Minister

Appointees must stay in Ghana for one year after office — Kofi Bentil proposes

Appointees must stay in Ghana for one year after office — Kofi Bentil proposes

2026 World Cup: Africa sets new record with seven teams reaching knockout stage

2026 World Cup: Africa sets new record with seven teams reaching knockout stage

2026 World Cup: Black Stars secure Round of 32 qualification ahead of Croatia cl...

2026 World Cup: Black Stars secure Round of 32 qualification ahead of Croatia cl...