Ghana has one of the most vibrant and competitive telecommunication (telecom) industries in the sub region. As one of the earliest countries in Africa to liberalise and deregulate its telecommunication sector in the early 1990s, Ghana has seen very rapid technological transformation, growth and intense competition across the mobile, Internet and fixed-line services.

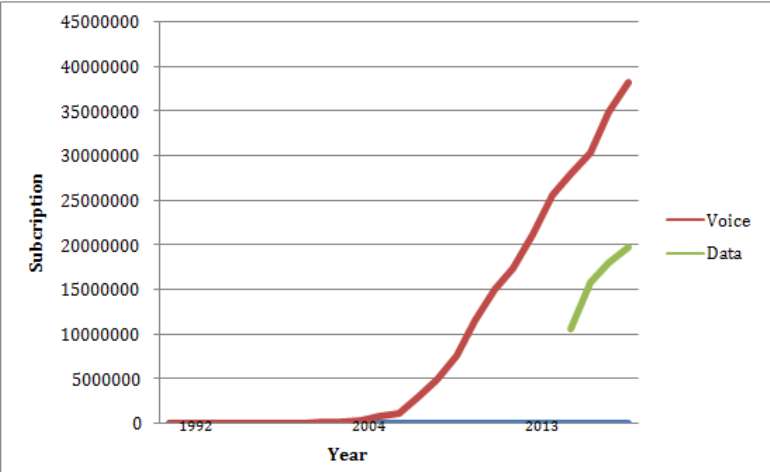

Currently there are two fixed line service operators, six mobile network operators, four mobile broadband access providers, 52 authorised Internet Service Providers (ISPs) and over 100 value added service providers[1]. At the end of April 2017, the total number of mobile voice subscriptions was 35,984,280 while the total subscriptions of mobile data in the country was 21,584,899 with a penetration rate of 76.22%[2].

The table below illustrates the growth in voice and data subscription since 1992.

In spite of the steady growth in the telecoms sector, introduction of new technologies and services is unusually delayed due to Ghana’s licensing regime, which requires operators to acquire new set of licenses to deploy new technologies and services. The delay and denial affects telecom service operators as well as consumers who are denied improved service quality and affordable prices.

Evolving License Regimes

Telecommunication market regulatory frameworks are hinged on licensing.[3] License is an official authorisation given by a communication regulatory body to service providers to operate networks or other value added services. It is usually a regulatory code that defines the terms and conditions under which the licensee may operate as well describe the rights and obligations of the service provider[4]. Licensing is also a means for Governments to generate revenue from network and service providers.

There are several frameworks for authorising telecommunication operations in a country. The type of licensing regime adopted has significant implications for barriers to entry for new providers and ease of introduction of new technologies. The table below summarises existing frameworks and with example of countries using it.

| Type | Description | Example |

| Specific license | Licenses are developed and awarded to individual service providers, with specific terms and conditions. | Many initial fixed and mobile telephone licenses. |

| Uniform license | All similar service providers have the same licenses, terms, and conditions. | Ghana |

| Unified license | Licenses are combined into a single license covering a wide range of services, effectively technology- and service- neutral. | Kenya’s licensing regime uses a unified, technology-neutral licensing framework that allows any form of communications infrastructure to be used for any communications service Other countries in Africa include Nigeria, Cote,Divore, Egypt, Tanzania, etc. |

| Class license | Technology-neutral licenses that include broad types of services under a single license. | Malaysia’s framework consists of 4 class and technology-neutral licenses, down from 31 in the older setup. |

| Notification | Operators are free to provide services subject to regulatory obligations and only have to notify the regulator before, or shortly after, initiating service. | EU members are moving toward an authorization regime using minimal regulatory intervention and requiring individual licenses only if strictly necessary (as with the use of finite available resources such as radio frequencies and telephone numbers). |

| No license | No license is needed to provide communications services. | In some countries like Japan, value added or Internet services do not require licenses. |

Source: ICT regulation toolkit, “MainTypes of Authorisation Regimes” ( www.ictregulationtoolkit.org )

License regime in Ghana

The license framework in Ghana is designed to encourage widespread entry into the telecommunication market place. The license regime is based on the various market segments and services provided in Ghana’s telecommunication value chain[5]. These are broadly categorised into international services, domestic public telephone services and dedicated transmission networks, internet services, and broadcasting services according to the 2007 National Telecommunication Policy.

Specifically, the National Communication Authority has issued the following licenses and authorisations across the telecoms market landscape: ISP/ Public Data Network, Television, FM Stations, UHF/VHF/HF Radio Networks, VSAT network, Dealership license, Aeronautics, Studio-To-Transmitter Link (STL), Maritime, International Submarine Cables, Tower Infrastructure Companies, Broadband Wireless Access, Fixed Network license, Mobile Network (GSM), and others.

This means vertically integrated mobile network providers in Ghana have multiple licenses to provide various services in the market landscape.

Limitations of existing license regime

Technological advancement is blurring the boundaries between wired telecommunications, wireless telecommunications and broadcasting services. The networks and systems supporting voice, data (internet) and content transmission to the end user has become interchangeable. This phenomenon, referred to as convergence[6]is gradually disrupting telecom business models, regulatory and license frameworks across the world.

The existing regulatory framework in Ghana played a significant role in encouraging healthy competitions, resulting in nation wide network coverage, improvement in quality of service as well as competitive pricing of voice and data services.

However the licensing framework in its current form is convoluted and is slowing down convergence happening in the telecommunication market. The service-based license regime as we have now is not technology neutral. This means introduction of new technologies into the market will always require new set of licenses to be issued.

The current license framework delay existing service providers from entering new markets and also creates an unfair competitive playing field for other service providers.

The network of existing service providers are far advanced to provide services beyond the current requirements of their license. The restriction of license requirements is hindering them from utilising and expanding the range of services they can offer.

For instance, Broadband Wireless Access (BWA) licensees are permitted to implement 4G services only until they are able to meet the 50% coverage threshold, before they can offer voice service[7]. This license regime is depriving the BWA licensees the opportunity to share in the voice market segment revenue.

Additionally, the six Mobile Network Operators (MNOs) in Ghana have the capability of delivering fixed telephone service to diversify their client base. But due to the limitation of the GSM license, only three (3) have been authorised in the wired market segment with two currently operating.[8]

Denying the full use of a network’s capabilities reduces its financial viability.

Similarly, a license regime that denies some operators the opportunity to enter new markets is unfair in terms of providing a competitive playing field for all players. In the award of the Broadband Wireless Access (BWA) 4G licenses in the 2500 – 2690 MHz band in 2013, only Ghanaian companies were permitted to bid for the spectrum.[9] Existing multinational MNOs were denied the opportunity to compete for the 4G license in the bid to ensure local content in the telecoms sector. Though the need for local content is important, a more innovate policy option should have been proposed to empower more local entrepreneurs into the telecom value chain. Ultimately, it is the Ghanaian consumer that loses out on the benefits of competition among multinational MNOs who already have the capacity to deploy 4G Internet faster across the country at much more affordable prices. Long delays by the regulatory authority in permitting expanded or better service choices to customers, slows innovation and makes network investments in infrastructure less attractive for network operators.. The limitations of the existing license regime can be addressed with a natural migration to a unified license - a global trend in regulatory frameworks.

A case for new license framework- Unified license

Unified license framework combines a wide range of service licenses into one set, which is technology and service neutral[10]. The objectives of unified licensing are to encourage the growth of new applications and services; simplify existing licensing procedures to ease market entry and operations; regulatory flexibility to address market and technological development and efficient utilisation of network resources, so that individual networks may be used to provide a broad range of ICT services [11]. The cardinal principles guiding unified license include; lack of distinction between mobile or fixed services, satellite or terrestrial services, data or voice services among others. Instead, licensees will be categorised based on whether they are Network Facilities Provider, Network Services Provider or Content Services Providers.[12]Unified license framework promotes technology and service neutrality in spectrum management, which enables convergence in telecommunication. This ensures effective and flexible utilisation of spectrum to the benefits of consumers..

Technology neutrality

Uniform license framework ties service operators to specific technologies to specific spectrum bands. Mobile network operators pay a lot of money to acquire these spectrums. The rapid evolution of telecommunication technologies means spectrum bands portfolios become devalued overtime at a fasterrate. This is a disincentive to investment into the sector. When 3G technologies were introduced for instance, most countries including Ghana authorised its operation in 2.1GHz band, separate from 2G technology bands. Service providers paid a lot of money to acquire this spectrum. 3G technologies later become available for commercial deployment in the bands used by 2G systems. Service providers that paid large sums to acquire spectrum in the 2.1 GHz band for 3G services now have to devalue their spectrum holdings and face higher capital costs because lower 2G frequencies have better propagation characteristics. In Australia, a network operator estimated that it would cut capital costs by 40 percent using the lower frequencies.[13]

Unified license framework makes it possible for Mobile network operators to efficiently manage and deploy new technologies easily within existing spectrum bands.

Service neutrality

Many countries (Australia, EU, UK, Japan Singapore etc.) have adopted a service neutral approach to allocation of telecom spectrum. This allows mobile network operators to decide the bundle of services to provide to their customers in a given band of spectrum to maximise digital dividend.[14]

For instance, in the United States of America, the Federal Communications Commission, the regulatory agency has allowed service providers to use the 700 MHz spectrum for a variety of broadcasting and telecommunications uses including fixed and mobile wireless commercial services; fixed and mobile wireless uses for private, internal radio needs; mobile and other digital new broadcast operations[15].

Benefits of unified license regime

Migrating to a unified license framework is a win-win for telecommunication companies, regulatory agencies, customers and a country as a whole. The removal of artificial distinctions between telecommunication services that unified license promotes affords MNOs and other operators the opportunity to choose technologies and systems in providing a variety of services to their customers in order to maximise returns on investment in infrastructure. It facilitates competition, innovation in service delivery and encourages the introduction of new technologies quickly. Ultimately the end user is the greatest beneficiary with better services at affordable prices. Botswana for instance moved nine (9) point up from 23rd position to 15th position in Alliance for Affordable Internet’s Affordability Driver Index[16]. According to the report, the improved performance is attributed to the simplification of existing multi-service licensing regime towards a unified license in 2015.The positive externalities of affordable telecom services are key determining factors in the growth equation of every country. License unification will also benefit the National Communication Authority. It will simplify the licensing structure thereby reducing the burden in monitoring and enforcing multiple license conditions and obligations. An efficient regulatory environment ultimately promotes growth and advancement of the telecoms sector.

Transitioning to a new licensing framework

In September 2014, the Minster of communication hinted the National Communication Authority (NCA) created four new license categories, a unified license inclusive.[17] This was followed by an advertisement by the NCA in December 2014 for the opening of a public consultation on Unified Service License on its website[18]. Since then, nothing has been heard about a unified license. With barely two years to the expiration date of the current GSM license it is important for the NCA to provide clarity on steps being taken towards a transition to a unified license besides past rhetoric.

The argument for the need to transition Ghana’s regulatory license regime to a unified one is now trite. The conversation should now be about the procedure and terms for the transition to a unified license regime. Key issues the NCA has to consider in transitioning to unified regulatory framework according to the International Telecommunication Union’s regulatory guidelines and principles for converging services include: whether to overhaul existing system all at once or phase the process; remapping services to be included in unified license and a decision on whether existing license holders will be compensated in the move to the new license regime. Finally, the unified license fees, compliance costs, management fees and others should not be exorbitant to facilitate an easy and efficient migration[19].

Conclusion

Convergence is the future in the telecommunication sector. It is opening new opportunities for innovations in the telecommunications in the fourth industrial revolution. Forward-looking countries have already developed policies and new regulatory frameworks to exploit the benefits of convergence, that is encouraging healthy competition in the telecoms sector, quality service and affordable broadband pricing.

The Ministry of Communication and the NCA, as a matter of urgency must state its position on the way forward on unified license framework in Ghana, modalities and timelines for transition.

The bus has already left the station and Ghana is late.

IMANI’s Centre for Science, Technology and Innovation Policy produced this paper. For interviews, please call Mr. Brian Dzansi on 0554 309 966 / 0302 972 939

[1] National Communication Authority (2017)

[2] Ibid.

[3] Scott W Minehane. (March 2015). What, who and how to regulate? Best practice licensing

frameworks in Asia and globally. Thailand. Retrieved from Windsor Place Consulting via https://www.itu.int/en/ITU-D/Regional-Presence/AsiaPacific/Documents/Events/2015/March-DigitalEconomy/Session1-1_Scott_Minehane.pdf

[4] Ibid.

[5] Ghana’s telecommunication value chain attached as appendix i.

[6] Convergence- “The coming together of previously technologically and commercially distinct markets such as broadcasting, print publishing, cable television, fixed wire voice telephony and cellular mobile and fixed wireless access.” International Telecommunication Union (ITU)

[8] National Communication Authority Annual Report. (2008) Ghana.

[9] Myyoyonline (Feb, 2014). 4G LTE coming on stream in Ghana this year. Available at

http://www.myjoyonline.com/business/2014/February-5th/4g-lte-coming-on-stream-in-ghana-this-year.php

[10] Telecommunication Development Sector (July, 2009). Regulation for licensing and authorization of converging services.ITU. Available at https://www.itu.int/ITU-D/treg/Events/Seminars/GSR/GSR09/doc/STudyGroup_draftreportQ10.pdf

[11] Ibid

[12] GSM Association (May 2012) Licensing to support the mobile broadband revolution. GSMA . Retrieved from https://www.gsma.com/publicpolicy/wp content/uploads/2012/03/gsma_licensing_report.pdf

[13] Rajendra Singh and Siddhartha Raja. (June 2008) Convergence in ICT services: Emerging regulatory responses to multiple play. World Bank. Accessed via http://bit.ly/2vocxFp

[14] Digital Dividend- the broader development benefits from using these technologies. World Bank.

[15] Federal Communications Commission (2000). FCC affirms rules for the 700 MHz band.. Accessed via https://transition.fcc.gov/Bureaus/Wireless/News_Releases/2000/nrwl0017.html

[16] Internet affordability index measures the range of policy and regulatory steps that countries are taking to drive down broadband prices and effectively tackle the affordability barrier to access.

[17] GhanaWeb (Sept 2014). Four new telecom license categories soon. Accessed via https://www.ghanaweb.com/GhanaHomePage/business/Four-new-telecom-license-categories-soon-324684

[18] National Communication Authority (Dec, 2014). NCA Opens Public Consultation on Unified Service Licence

It's alarming how SHS students have the courage to sell marijuana on campus; let...

It's alarming how SHS students have the courage to sell marijuana on campus; let...

Mahama charges new Auditor-General to be bold, fair and independent

Mahama charges new Auditor-General to be bold, fair and independent

Dr. Pamela Graham sworn in as Ghana’s first female Auditor-General

Dr. Pamela Graham sworn in as Ghana’s first female Auditor-General

Government appoints Brig. Gen. Okae-Yeboah to lead nationwide flood mitigation t...

Government appoints Brig. Gen. Okae-Yeboah to lead nationwide flood mitigation t...

South African Police link killing of Ghanaian national in Cape Town to extortion...

South African Police link killing of Ghanaian national in Cape Town to extortion...

GMet forecasts moderate rainfall over the weekend

GMet forecasts moderate rainfall over the weekend

Gov't to build 10 new SHSs, rehabilitate 150 existing ones — Haruna Iddrisu

Gov't to build 10 new SHSs, rehabilitate 150 existing ones — Haruna Iddrisu

GH¢100m allocated annually for special needs education — Haruna Iddrisu

GH¢100m allocated annually for special needs education — Haruna Iddrisu

Dada Joe Remix pleads guilty in US Court to multi-million-dollar romance fraud

Dada Joe Remix pleads guilty in US Court to multi-million-dollar romance fraud

Comments

Other companies must be allowed to compete with Vodaphone in providing Landlines. They are too lapse in their duties. They only serve the so-called big People. Since they don`t meet me at home in suit, they think I am Mr. Nobody. How Long does it take to fix a 100 meter line.? May the LORD have mercy on them.