Bank of Ghana (BOG) together with other regulators in recent times took punitive actions that saw some banks and non-bank financial institutions losing their licenses.

There have been several schools of thought which question whether the actions taken by the BoG and other the regulators were done in accordance with the laid down procedure.

While others believe that it was a good move and were even long overdue, others hold the view that they could have used a different approach; but these arguments are not the focus of this article.

There is an old adage which says that “The beauty of a woman is not in the clothes she wears… True beauty in a woman is reflected in her soul” .

In the same vein, I have seen and heard a lot of people equating what makes a bank good to simply good customer service and products. In my candid opinion, these are good qualities that every bank must possess.

However, a good bank goes beyond just a magnificent ultra-modern head offices premises, robust online channels and buzz words, good customer service and product delivery.

Banking is a serious business and we must continue the education to protect the financial sector for key actors, stakeholders, and depositors and further to improve the economy.

Stronger economies like Singapore, United States of America, and the United Kingdom reflect its robust and efficient financial sector. So, in a real business sense, what characterizes a good bank?

Level of Capital Adequacy

A bank’s capital is fundamentally more important to its existence. No wonder the Bank of Ghana, for instance, required all commercial Banks in Ghana to raise capital levels from Ghs120m to GH¢400m by 31st December 2018.

Indeed this was welcoming news especially looking at the low capital levels of some banks at that time. A high level of capital permits management to pursue higher-risk business opportunities while a low level restricts management`s scope for manoeuvre.

In simple terms, Capital Adequacy refers to the amount of shareholders` fund that should be available to support the business of any bank and the amount largely depends to the size of the balance sheet and types of activities in which the bank participate. To a large extent, a bank must have the capital for three major reasons:

- to absorb unexpected credit losses;

- to provide safety for depositors and creditors, and

- to satisfy regulatory authorities’ ongoing concern with depositor protection and a stable banking system.

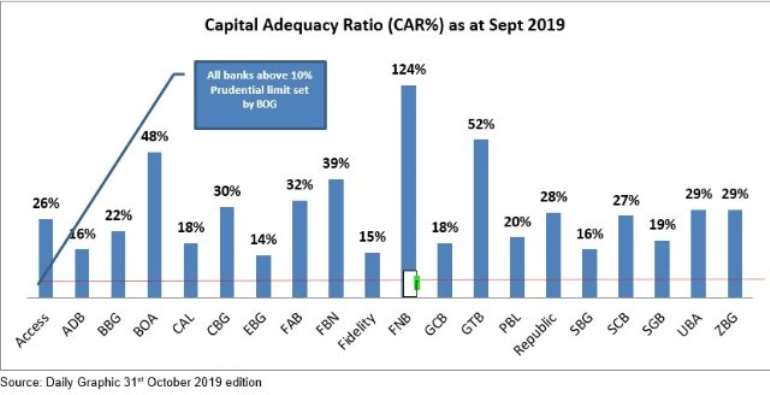

Although there is a general market approach in accessing a bank’s capital, the regulatory approach of the BOG is the most acceptable; In Ghana, the BOG has set a minimum 10% prudential limit Capital Adequacy Ratio (CAR). In essence, the source, quality and quantity of capital are very important for a bank to be considered as a good bank.

Asset Quality

It`s an undeniable fact that poor asset quality has been the major cause of most banks’ failure and this is mainly due to inadequate management in lending policies. Market knowledge of poor asset quality often leads to pressures on a bank`s short term funding positions which usually results in a liquidity crisis of an ‘outright run on the bank’.

To determine if a bank is good, it is critical to assess the bank`s credit risk management strength and weakness and also evaluate the quality of the investment and loan portfolio using trend analysis and peer comparison. In recent times most banks have instituted a tight credit stance resulting in a flat loan book growth in Ghana.

Again, for most banks, investments in marketable and trading account securities and interbank deposits form a chunk of the lending book. This is important to monitor because many financial institutions will be declared insolvent in periods of high-interest rates if they were required to adjust loans to market value.

Good financial institutions are those who provide accurate information on;

- low loan concentration;

- problem loans and past due amounts;

- the true size of loan reserves;

- details concerning the period`s loan loss allocation; and

- details on loan write-offs or recoveries.

So, in effect, based on an industry average of Non-Performing Loans (NPLs), Banks with low NPLs are deemed to be doing well in the sense that the higher the ratio the more capital a bank will normally require to support the loan portfolio. Relatively high NPLs are not so bad so far as there is an adequate provision to the loan loss reserve account to absorb further losses.

Experienced Management Team

The management of a good bank possesses the technical competence, leadership and administrative ability to run a bank. The calibre of some bank officials who were running financial institutions in Ghana left much to be desired. No wonder the BOG came out with the ‘fit and proper’ guidelines aimed at ensuring that the right persons with the requisite qualifications and experience become managers of the Banks.

The quality of management for me remains the single most important element in sustaining a bank, as decisions invariably impact the success of the bank.

It`s not just in enough to have so-called individual`s sitting on various boards of a bank without the requisite understanding of basic banking practices, they should be able to make a decision that impacts directly or indirectly on asset growth, asset quality, earning levels and funding strategies. All these influence investor confidence as well as providers of capital adequacy.

A financial institution that respects the basic principle of corporate governance where the functions of the Chief Executive Officer (CEO) and the board chairman are separated have a sense of long term growth.

Earnings or Profitability level

A good bank must make a profit over a period of time. Indeed profitability is the supreme indicator of management`s success or failure in its strategic and leadership.

Bank earnings provide capital formation and they need to attract new investor capital which is essential for the business to grow. But how do banks make profits? There are four principal sources of bank revenues which are Interest income, Fees and Commissions, Trading Income and other income. The most important expenses are interest expense, staff and provision for loan losses.

Earnings are important three major reasons:

- They help absorb any potential losses,

- They are necessary for a balanced financial structure

- They provide shareholders reward.

In all these, what is also important to check is the ‘quality’ of earnings taking into consideration, how stable and reliable they are comparing to peers within the same industry. It`s important to note that individuals seek to understand the dynamics that drive a bank`s profit and uncover the strength behind a bank`s prospects to stay competitive

Amount of Liquidity

If we recall, one major reason that led to the financial sector challenges for most of the banks was their low level of liquidity. Funds were locked up because some of the banks not liquid.

Liquidity in bank management is needed for two major reasons: first, to satisfy the demand for new loans without having to recall existing loans or realize term investment such as bonds holdings and second, to meet both daily and seasonal swings in deposits so that withdrawals can be met in a timely and orderly fashion.

Good banks make money by riding on the yield curve that is mobilizing short-term deposits at lower interest rates, and lending or investing these funds in a longer-term asset at higher rates.

This liquidity mismatch is very dangerous and this means that banks who may not be able to keep 20 and 30percent of total assets to meet normal liquidity needs to meet their customer needs may fail. Good liquidity position for banks inspires depositor and lender confidence but it important to note, the more liquid asset, the less it will earn. Bank managers strike a balance and determine the ideal comfortable level of liquidity that will respond to customer needs.

Sensitivity to market risk

Lastly, banks are sensitive to various market risks. Banks must address the extent to which changes in interest rates, foreign exchange rates, commodity prices or equity adversely affects a financial institution`s earnings or capital. Banks must therefore carefully identify, monitor, manage and control its market risk and provide bank management with a clear and focused of supervisory concern in this area.

In summary, a good bank is measured by its safety, profitability and liquidity levels. Safety of a bank is interpreted in terms of ability to cover costs and meet all obligations and it`s also evaluated looking at the level of capital adequacy, asset quality and management efficiency.

We shouldn’t look at financials institutions on the face value, the advertisements and media campaigns. Those who have stood the test of time are those who have been able to put robust structures to mitigate any potential loss. Let`s protect what we have and rather make them stronger.

Credit : Daily Graphic, 31st October 2019 edition, Miriam Amoako, Raymond A. Grier.

Disclaimer: The views expressed are personal views and doesn’t represent the institutions the writer works for.

About the writer

Carl Odame-Gyenti is a third-year PhD (Financial Management) candidate, a Finance and Telecom enthusiast, managing local and global Investors, Intermediaries, Non-Bank Financial and Financial Institution relationships with an international bank in Ghana. He has embarked on several international assignments in London, Singapore, Dubai, Kenya, Nigeria and Southern African markets. He has a passion for youth and community development.

Gov't to invest GH₵2.5bn into second-cycle education infrastructure

Gov't to invest GH₵2.5bn into second-cycle education infrastructure

NDC to rename national headquarters after Rawlings, unveil bust on 79th birthday

NDC to rename national headquarters after Rawlings, unveil bust on 79th birthday

V/R: Two dead, farmlands destroyed as floods ravage Ketu North

V/R: Two dead, farmlands destroyed as floods ravage Ketu North

V/R: Flood waters submerge acres of farmland in Anloga

V/R: Flood waters submerge acres of farmland in Anloga

Al-Qaeda-linked jihadists attack Niger airport, 11 soldiers killed

Al-Qaeda-linked jihadists attack Niger airport, 11 soldiers killed

Ghana pushes for concrete slavery reparations

Ghana pushes for concrete slavery reparations

Fire destroys five-bedroom house; family, tenants rendered homeless

Fire destroys five-bedroom house; family, tenants rendered homeless

Timber Millers accuse, demand arrest of trade association members behind attack ...

Timber Millers accuse, demand arrest of trade association members behind attack ...

Two Christ the King SHS students injured in machete attack by suspected gang in ...

Two Christ the King SHS students injured in machete attack by suspected gang in ...

Controller plans salary deductions of 4,000 public sector workers who still owe ...

Controller plans salary deductions of 4,000 public sector workers who still owe ...