The debate around the depreciating cedi has resurfaced, following recent claims by Vice President Dr Muhamadu Bawumia that the local currency has performed better in 2018 than in the entire eight years of the National Democratic Congress (NDC) administration.

As an ardent believer that currency depreciation is caused entirely by weak economic fundamentals, vice president had, in the past, sought to blame every glimpse of the cedi depreciation on weak economic fundamentals.

This is evident in his now infamous 2012 pronouncement that“you can engage in all the propaganda you want but if the fundamentals of the economy are weak, the exchange rate will expose you.”

However, now faced with a reality check – an abysmal cedi under his watch as Head of the Economic Management Team (EMT) – Dr Bawumia has tried to invent alien methods and use same in foreign exchange calculations in other not to bust his ego.

In one such attempt, he famously used rate of change to calculate currency depreciation contrary to the approach used by the Bank of Ghana (BoG) over the years. Beyond contradictingBoG, the rate of change method that Dr Bawumia used was also alien to internationally-accepted methods of calculating currency depreciations.

Disservice to BoG

Before I expose the flaws of the New Patriotic Party's (NPP) economic wizard, let me be upfront that the Vice President, in his attempt to appear and remain the 'best economist in Ghana,' has driven the country into virtually politicising the operations of the BoG, whose duty it is to independently and sacredly manage the performance of the cedi against its trading partners.

As one of the delicate tools available to central banks for economic management, the BoG uses market-sensitive information to manage the strength or otherwise of the cedi. If not properly contained, this sensitive information can lead to undesired outcomes, key among them being speculation.

For instance, if the BoG at a point is suffering from depressed reserves, leading to liquidity challenges, and the market is unaware, speculative or panic behaviour may be absent. However, if the market is aware because the BoG's management of the currency has been exposed through a Dr Bawumia-induced scrutiny, the country would have been revealing the challenge over a period to market participants.

The result will be an uptick in speculative behaviour to the detriment of the currency. Once this is made a cycle, it becomes difficult to manage.

Therefore, politicising currency management is the worse that should ever happen; it deepens the scrutiny of BoG's currency management role in a way that creates further fear and panic, especially when the information from the central bank does not give comfort. Sadly, that information is neither what the government nor the BoG say but what is available to analysts and market participants.

Closely related to that is the fact that Ghana needs a stable currency, not a strong one, as Dr Bawumia would have us believe.

As a lower middle-income country, Ghana needs to import less and export more. To do that we need to maintain a fairly stable, not strong currency to make our exports cheaper abroad, similar to what makes Chinese exports a toast of the world.

So, for a vice president, who heads the EMT of a government that touts industrialisation as the center of its economic policy, to be obsessed with a strong currency leaves much to be desired. It calls into question the commitment of the government to its sloganeering 'One District, One Factory' agenda.

Unfortunately, Dr Bawumia has brought it upon us, first while in opposition and now as Head of EMT.

While I do not expect BoG Governor, Dr Ernest Addison, to openly rebuke the vice president, given Dr Addison's depth on the matter, I expect that he smartly points Dr Bawumia to the dangers and disservice his continuous, inaccurate and needless politicisation of currency management is bringing to the nation and the BoG in particular.

Worsening cedi

A review of data from BoG show a worsening depreciation of the cedi. As a matter of fact, the cedi is on its worse performance against the major trading currencies in the last three years.

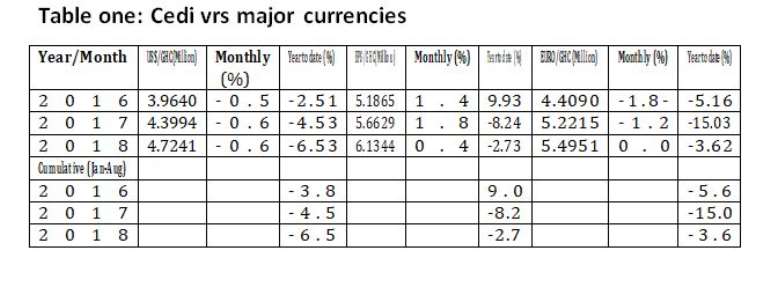

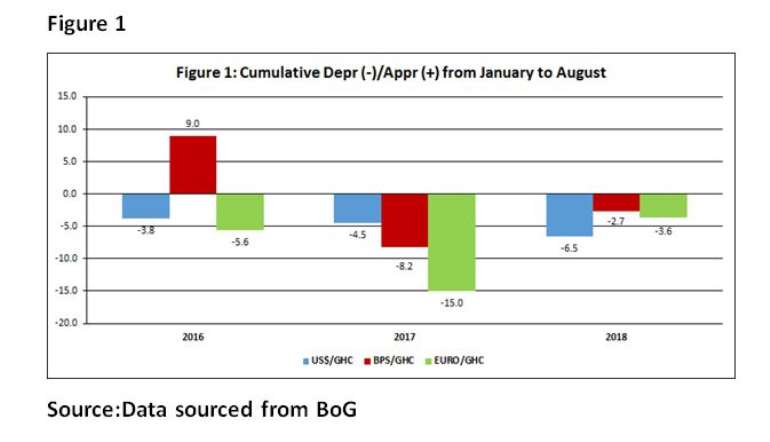

Since Dr Bawumia picked the performance of the cedi as at August 2018, let us look at the year-on-year performance of the cedi in August 2016 to 2018 as well as the cumulative performance for same period – January to August 2016 and January to August 2018.

It is clear from the exchange rates, cedi depreciation and appreciation data in table one that the cedi has depreciated significantly against the major trading currencies in cumulative terms, from January to August 2018.

While the cedi experienced marginal year-to-date depreciation of 2.51 per cent against the US dollar in August 2016, it experienced a higher depreciation of 4.53 per cent inthe same period in 2017.

The 2016 depreciation, however, more than doubled to an alarming rate of 6.53 per cent in August 2018.

Unfortunately, the Head of the EMT says the cedi is in its best shape since 2007. Is Dr Bawumia using data different from what is available?

The cumulative analysis of the depreciation of the cedi against the dollar from January to August shows a consistently worsening cedi, with a depreciation from 3.8 per cent in 2016 to 4.5 per cent in 2017 and 6.5 per cent in 2018.

In terms of the pounds sterling, the cedi deteriorated from a stronger position in 2016, when it appreciated by nine per cent to depreciate at 8.24 per cent in 2017 and 2.7 per cent in 2018.

Although the cedi has recovered from its collapse against the pound, it is still worse off than the strong performance in 2016. Yet, Dr Bawumia says the cedi is in the best it has ever been.

Against the euro, the cedi depreciated by over 15 per cent in the same period in 2017 compared toa depreciation of 5.16in the same period in 2016.

Although it has improved in 2018, it is a herculean task for it to recover the 15 per cent per cent depreciation experienced in 2017. Yet again, Dr Bawumia says the cedi is in top form.

Warped logic

I have heard Dr Bawumia attribute the cedi's troubles to increase in interest rates by the Federal Reserve of the United States.

While it is generally expected that increased rates in a country may lead to capital flight to that country to take advantage of high earnings, it gets curious if one sees this depreciation span several currencies and not just the US dollar, which should be in high demand by investors.

With the cedi losing value to the euro, pound and even the CFA in Francophone West Africa, the questions to ask are:

Did the European Union also increase interest rates to cause the cedi to depreciate by 15 per cent against the euro?

Did the British increase interest rates to cause the cedi to move from a strong position of nine per cent appreciation in 2016 to a depreciation of 8.24 per cent in 2017 and 2.7 per cent in 2018?

It is obvious that the cedi's woes are more than interest rate hikes in America. Needless to say the cedi has depreciated against the Swiss franc, Canadian dollar, New Zealand dollar, Norwegian kroner, South African rand and the Japanese yen.

Are all these caused by interest rate hikes in those countries?

Real causes

A review of BoG data shows that the cedi is suffering from liquidity crunch in the market. This is caused by several factors, some of which are self-inflicted by the BoG, government and the Securities and Exchange Commission (SEC).

The cedi has been badly exposed by lack of appropriate cover for imports, unsustainable borrowing by the central bank to support the cedi and the general slowdown of the real sector of the economy, leaving the minerals and oil and gas subsectors to shoulder the task of forex inflows and liquidity in the market.

Of critical importance are;

- Worsening net international reserves and import cover

The country's trade balance began to see improvement towards the fourth quarter of 2016. This resulted from upscale of oil and gas output from the Jubilee Fields after the turret bearing problem of the FPSO that had affected production negatively in the first half of 2016 had been resolved.

By the end of 2016, Ghana was beginning to become a net exporter of oil and gas. As a result, we significantly relied on our own gas from Atuabo to power our thermal plants, thereby reducing significantly our importation of gas and light crude. This positively impacted our trade balance.

By 2017, we strongly improved our production of crude and gas at the start of production from the TEN and Sankofa Gye-Nyame fields, which made us to register a significant trade surplus. This enhancement was also occasioned by improved world commodity prices that saw the minerals sector see improved earnings.

By 2018, all these gains had stabilised with pressure mounting to find other growth drivers to support inflows since the export earnings from minerals as well as oil and gas are held by foreign investors and do not significantly impact liquidity of forex in the market.

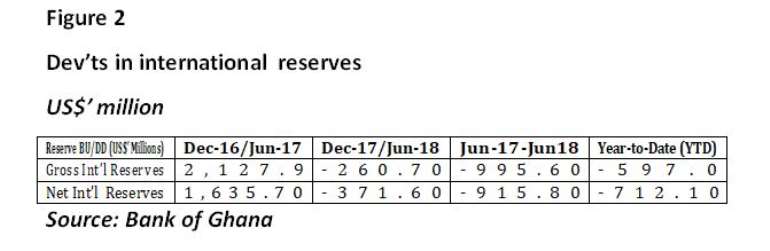

Unfortunately, as we have basked in the glory of improved trade balance, our net reserve position has continued to worsen.

We stopped building up reserves but was constantly drawing down our foreign reserves to support the cedi.

BoG data suggest that our current net foreign reserves as at August 2018 can only cover two months of imports.

What this means is that our net foreign reserves, which increased significantly by June 2017 and demonstrated a healthy export base inherited by the NPP has continuously worsened.

See figure 2 below

Table two shows clearly how the NPP administration has failed to maintain robust flows of reserves it inherited from the NDC administration.

The tremendous increase in reserves in June 2017 were inflows from the work of the NDC administration, with a time lag of six months. These reserves accumulated from January to June even before NPP could have a budget approved by March 31, 2017 and put together a full government of 110 ministers.

Unfortunately, these reserves have declined considerably from June 2017 to July 2018, thereby creating serious liquidity crunch in the market.

The import cover from our net international reserves has declined from 2.9 months to two months despite the massive export earnings from minerals, oil and gas as well as inflows from proceeds of excessive borrowing by the government, of which the forex are ultimately surrounded to BoG.

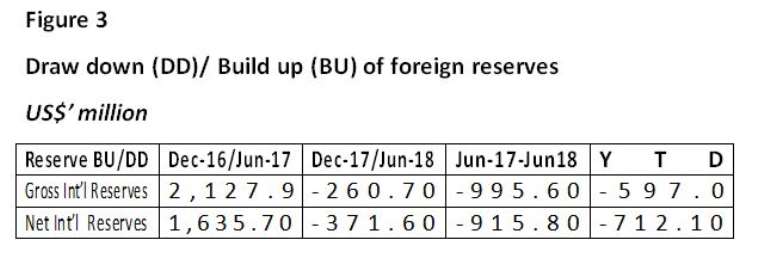

A review of the reserve movements below shows the source of depletion of the reserves and the huge liquidity challenge facing the cedi.

Table three shows how much reserves were built for Dr Bawumia to inherit to manage the cedi.

Unfortunately, as the table indicates, instead of building it further, he and the government have been rapidly drawing down the reserves, much to the detriment of the cedi.

By June 2017, Ghana had built up additional US$2.13 billion in gross international reserves andUS$1.64 billion of net international reserves. What Dr Bawumia and his team has done is to fold their arms and squander these reserves through drawdowns as evidenced in the table.

It is instructive to note that between June 2017 and June 2018, a period of just one year, close to US$1billion (US$995.60 million)has been drawn down.

From January 2018 to July 13, 2018 (less than seven months), a whopping US$712.10 million had been drawn down to support the cedi.

Clearly, if all one does in economic management is to inherit reserves and throw it at the cedi when it is in trouble in the hope that it will find strength, then we are dealing with a truly overhyped economist.

- Capital flight

The Ghanaian banking and financial sector is at its lowest ebb. Confidence is at an all-time low as regulatory ineptitude and self-serving political regulations have created a spate of panic withdrawals, a volatile financial sector and speculative investments of withdrawals in foreign currencies as a hedge.

This is evidenced in the spike in investment in foreign currencies as reported by the BoG. From 15.9 per cent in August 2017, foreign currency deposits increased to 18.3 per cent in August this year, the highest in the 12-month period.

This confirms that investors are moving their funds to safety in foreign markets while Ghanaians who are redeeming their investments with fund management companies and those involved in panic withdrawals are instinctively converting their monies into foreign currencies. These increase demand for foreign currencies and mount pressure on the cedi.

I will not belabour the point about the long-discussed structure of the economy that has created lop-sided import-dependent economy with limited diversification of export earnings.

These must be addressed in the medium-to-long-term to ease volatility and create sustainable buffers for the cedi.

Way forward

- Government may look to fast-track the disbursement of the cocoa syndication loan for 2018 for surrender to the BoG to intervene in the market. This should help to improve reserves and provide a buffer, albeit in the short-term, for the cedi.

- Immediate restoration of confidence in the banking and financial sector through far-reaching confidence-enhancing measures. These should include;

- Immediate extension of the deadline for the recapitalisation of local banks. This will immediately calm the market and reverse the panic withdrawals and speculative build-up of foreign currencies as investment and hedging tool

- Establishment of a stimulus fund immediately to be managed as a venture capital by the Financial Investment Trust (FIT) of BoG. This should be accompanied by a clear policy position to create an enabling environment for owners of local banks to engage in merger talks to leverage shortfalls in meeting the minimum capital through the FIT as equity participation with a clear exit strategy.

The amount of money to be put in the fund will depend on a policy capping of government participation. This way, we will not throw, GH¢12 billion at toxic assets and nationalisation of privately owned Ghanaian banks as we are currently doing. Can you imagine what a stimulus package of GH¢12 billion as a bait for mergers of local banks would have done to the confidence of the banking sector and the strength of balance sheets of local banks?

The SEC to reverse its deliberate policy and directive to fund management companies to wind down their investments. This will stop the panic redemptions and withdrawals and slow down the rate at which people are converting their investments into dollars.

- Improve the business environment immediately to resuscitate dying businesses and restore collapsing manufacturing companies. This will reduce imports and provide alternative sources of foreign exchange earnings. It is worthy to note that both the BoG consumer and business confidence indexes are on record lows of 98.1 and 99.9 as of August 2018. What this means is consumers and businesses have lost confidence in the ability of the government to turn the economy around.

As indicated earlier, currency management is a sacred responsibility resigned to central banks, which are noble institutions in the economic management organograms of countries.

It must, therefore, be allowed to perform its responsibilities, including managing the exchange rate, devoid of unnecessary politicking, which has negative and wider implications on the economy.

By: Isaac Adongo

The writer is the NDC Member of Parliament for Bolgatanga Central

Two Nigerians arrested over alleged murder of compatriot in Tamale

Two Nigerians arrested over alleged murder of compatriot in Tamale

NPP demands Miracles Aboagye's release, condemns EOCO detention

NPP demands Miracles Aboagye's release, condemns EOCO detention

Dennis Miracles Aboagye arrested by EOCO at Accra International Airport

Dennis Miracles Aboagye arrested by EOCO at Accra International Airport

No more removing laptops, shoes and belts at airport as GACL introduces new airp...

No more removing laptops, shoes and belts at airport as GACL introduces new airp...

Child marriage among children aged 12-17 remains high in Oti region – GSS

Child marriage among children aged 12-17 remains high in Oti region – GSS

KNUST student and street preacher clash over early morning noise

KNUST student and street preacher clash over early morning noise

How some women at Inchaban forced resident to join national sanitation day exerc...

How some women at Inchaban forced resident to join national sanitation day exerc...

Massive fire engulfs alcohol warehouse at Tema Community 26

Massive fire engulfs alcohol warehouse at Tema Community 26

'Unity remains our greatest strength and the surest path to victory in 2028' – B...

'Unity remains our greatest strength and the surest path to victory in 2028' – B...

Strengthen ADR to reduce court backlog, improve access to justice – Prof. Asante

Strengthen ADR to reduce court backlog, improve access to justice – Prof. Asante