The speed with which we criticise should match the speed with which we acknowledge success.

Public debate over the Bank of Ghana’s 2025 financial results has been dominated by a single headline: a GH¢15.6 billion loss. But that headline obscures the real story. What the Bank recorded was not an economic loss. It was the financial cost of delivering one of the most dramatic stabilisation turnarounds in Ghana’s recent history.

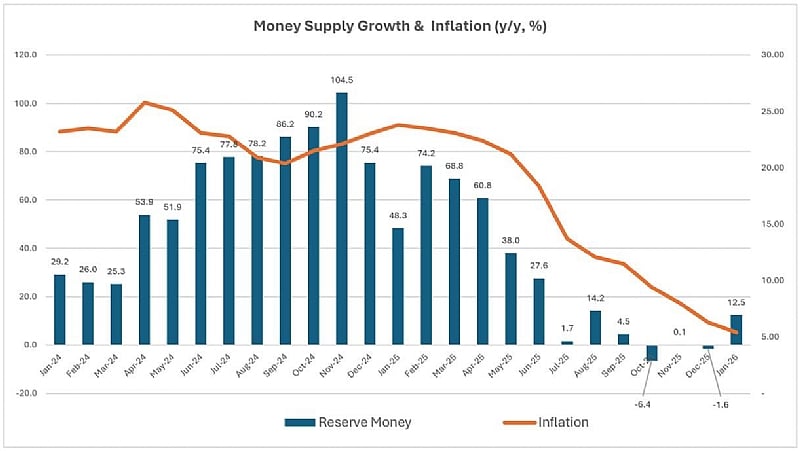

The evidence is visible in the Bank’s own data. The graph on Money Supply Growth and Inflation shows a near‑perfect mirror movement: as reserve money growth plunged from 104.5% in late 2024 to just 2.6% by December 2025. Inflation followed, falling for 13 consecutive months from 23.8% to 5.4%, and further to 3.2% by March 2026.

This is the clearest demonstration of decisive monetary policy in action.

Data: BoG & GSS

Data: BoG & GSS

This stabilisation was necessary because Ghana entered 2025 with a 3.1% of GDP fiscal deviation, representing over GHS36 billion in overspending. That single slippage was equivalent to the entire IMF programme loan at today’s rates. The banking system was flooded with excess liquidity, and inflationary pressure was entrenched. The Bank of Ghana had no choice but to act.

And it did.

The Loss Was the Cost of Fixing the Economy

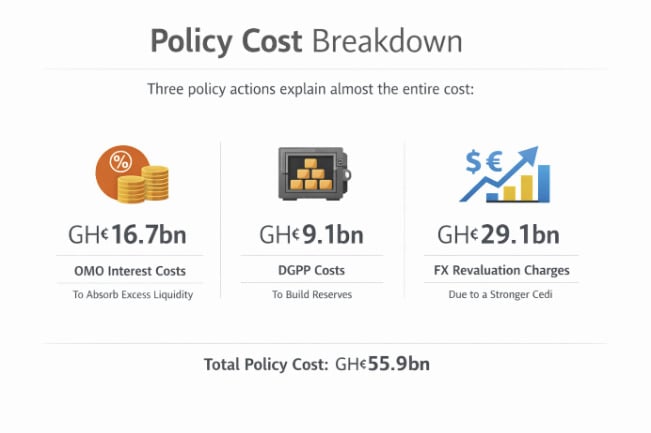

Three policy actions explain almost the entire loss:

- GH¢16.7 billion in OMO (Open Market Operations) interest costs to absorb excess liquidity;

- GH¢9.1 billion in DGPP (Domestic Gold Purchase Programme) costs to build reserves; and

- GH¢29.1 billion in FX revaluation charges due to a stronger cedi.

These are not commercial losses. They are policy costs; the price of reversing years of fiscal slippages and monetary expansion. Central banks are not profit‑maximising enterprises. They are policy institutions. Their mandate is to stabilise prices, protect the currency, and maintain financial‑system confidence. When they act forcefully to restore stability, the financial statements reflect the cost of those actions. But the economic value created far exceeds the accounting charge.

OMO: The Weapon That Broke Inflation

OMO was the Bank’s most powerful tool. By issuing instruments to pull excess money out of the system, the Bank engineered the collapse in reserve money growth shown in the graph. Without this, inflation would not have fallen. The GH¢16.7 billion OMO cost was therefore not a loss; it was an investment and it paid off. It was also effective because fiscal managers at the Ministry of Finance maintained discipline, avoiding new slippages that would have undermined the Bank’s efforts.

The FX Revaluation Charge Was Not a Cash Loss

The FX revaluation charge has also been misunderstood. The cedi strengthened 40.7% in 2025. That strength reduced the cedi value of the Bank’s foreign assets, creating a GH¢29.1 billion accounting charge. But no reserves were lost. No cash left the Bank. The same accounting rule produced a GH¢12.7 billion gain in 2024 when the cedi weakened. The accounting treatment did not change. The exchange rate did. In simpler terms, while in 2024, every $100 on the financials was booked as Ghs1,470, the same $100 was now booked as Ghs1,045 because the cedi strengthened. The $100 remained the same but in cedi terms, Ghs425 was lost; a paper loss.

The DGPP Built the Highest Reserves in Ghana’s History

The DGPP’s GH¢9.1 billion cost must likewise be viewed alongside its outcome: reserves rose from $9.1 billion to $13.8 billion, import cover reached 5.7 months, and the programme expanded to 111 metric tonnes of gold in 2025. This was a strategic investment in resilience and ultimately contributing to the strong appreciation of the Ghana cedi by about 40%.

The Economic Gains Were Productive

The economic gains were substantial: single‑digit inflation, a 40% appreciation of the cedi, over GHS60 billion in import‑cost savings for households and firms, over GHS12 billion savings in government FX‑linked expenses, public debt falling from 61.8% to 45.3% of GDP, record reserves, lower lending rates, and renewed confidence in the currency.

The ‘Loss’ Was the Price of Stability; And It Worked

The Bank of Ghana’s 2025 loss is not evidence of mismanagement. It is evidence of a central bank doing exactly what its mandate requires: stabilising the economy, restoring confidence, and protecting the value of money.

Governor Asiamah and his deputies, Dr. Zakaria and Mrs. Asante, deserve recognition for the boldness and discipline that made this turnaround possible.

GeePapa

Entrepreneur, Finance & Economic Policy Analyst

4th May 2025

Accra Is Sinking Yet Again — Time to Be Truthful With Ourselves

Accra Is Sinking Yet Again — Time to Be Truthful With Ourselves

Fire guts rubber factory at Circle Odawna as flooding hampers firefighting effor...

Fire guts rubber factory at Circle Odawna as flooding hampers firefighting effor...

Flooding strands commuters on Winneba Cape Coast Highway

Flooding strands commuters on Winneba Cape Coast Highway

Three feared dead after electrocution in Alajo flooding incident

Three feared dead after electrocution in Alajo flooding incident

Nine missing after floods hit Awutu Senya East

Nine missing after floods hit Awutu Senya East

'Your mother, I should go to heaven and ask Nebuchadnezzar to stop the rain?' — ...

'Your mother, I should go to heaven and ask Nebuchadnezzar to stop the rain?' — ...

Flood victim found dead along Alajo Railway track as rescue operations continue

Flood victim found dead along Alajo Railway track as rescue operations continue

GMet warns more rain as flooding disrupts movement across Greater Accra

GMet warns more rain as flooding disrupts movement across Greater Accra

'You sit on social media and talk nkwasiasem' — Nigel Gaisie blasts critics over...

'You sit on social media and talk nkwasiasem' — Nigel Gaisie blasts critics over...

Osahen Afenyo-Markin accuses NDC of using GoldBod to promote illegal mining

Osahen Afenyo-Markin accuses NDC of using GoldBod to promote illegal mining