Abstract

Ghana’s economy has demonstrated notable resilience amid global uncertainty and significant domestic challenges. This article examines recent macroeconomic developments, emphasizing renewed GDP growth, rapid disinflation, and fiscal consolidation under an IMF-supported program. It further analyzes the structure and performance of Ghana’s financial system, focusing on the banking sector, capital markets, and the insurance industry. By exploring the interactions between macroeconomic policy and financial-sector dynamics, the paper highlights prospects for sustainable and inclusive growth while identifying persistent vulnerabilities, including elevated public debt and non-performing loans. Using recent data up to 2026, the study argues that sustained reforms and institutional discipline remain critical to long-term economic stability.

Introduction

Ghana, a West African country with a population exceeding 35 million, transitioned from low-income to lower-middle-income status in 2011. Since then, its economic trajectory has been shaped by commodity-driven expansions primarily in gold, cocoa, and crude oil interspersed with episodes of macroeconomic instability. The post–COVID-19 period proved particularly challenging, culminating in a severe macroeconomic crisis in 2022 marked by rising debt levels, sharp currency depreciation, and surging inflation. In response, Ghana entered an IMF-supported Extended Credit Facility (ECF) programme in 2023, aimed at restoring macroeconomic stability and debt sustainability. By 2025, the economy exhibited signs of recovery, reflecting the impact of policy adjustment and reform. This paper examines Ghana’s recent macroeconomic performance and financial-system developments, highlighting their mutual interactions and implications for sustainable economic transformation.

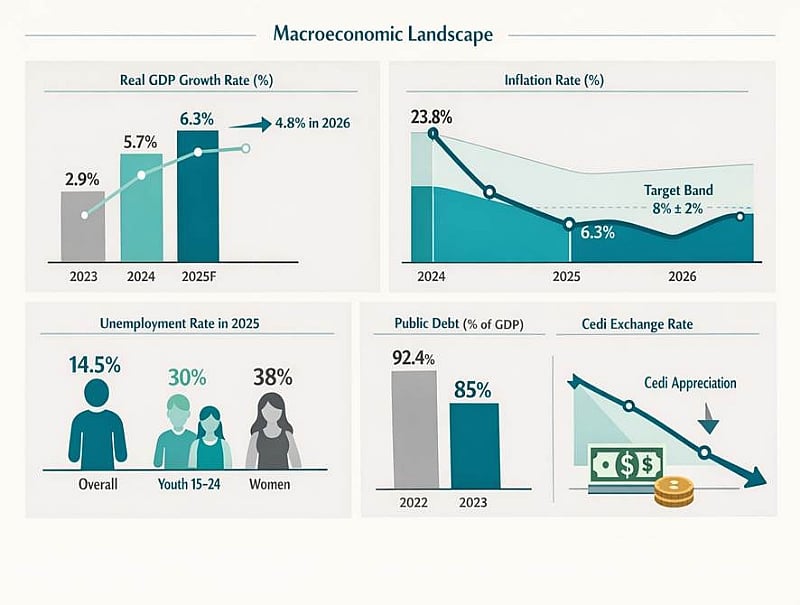

Macroeconomic Landscape

Recent macroeconomic outcomes in Ghana reflect the combined influence of external shocks and domestic policy reforms. Real GDP growth moderated to 2.9 percent in 2023, constrained by tight global financial conditions and disruptions linked to the Russia–Ukraine conflict. Growth rebounded strongly to an estimated 5.7 percent in 2024 and accelerated further in the first half of 2025, reaching approximately 6.3 percent year-on-year. This recovery has been broad-based, with agriculture and services providing significant impetus, supported by improved confidence and relatively favourable commodity prices. Growth is projected to moderate to about 4.8 percent in 2026 as fiscal consolidation dampens domestic demand amid persistent global uncertainties.

Inflation, long a key macroeconomic challenge, declined sharply following the implementation of a tight monetary stance. Headline inflation fell from 23.8 percent in December 2024 to 6.3 percent by November 2025, marking its lowest level since early 2019. This outcome reflected a combination of currency appreciation, easing food prices, and restrictive monetary policy by the Bank of Ghana (BoG). Food and non-food inflation converged at similarly low levels, enabling the BoG to commence a cautious easing cycle in 2025 after inflation returned to its medium-term target band of 8 ± 2 percent for the first time since 2021. Inflation is expected to stabilize in the range of 9–11 percent in 2026, barring major external shocks.

Labour-market conditions remain a structural concern. The unemployment rate stood at approximately 14.5 percent in 2025, with youth unemployment exceeding 30 percent among individuals aged 15–24. Women are disproportionately affected, highlighting the urgency of employment-generating investments, particularly in agriculture, agro-processing, and services.

Fiscal policy has been anchored on consolidation under the IMF programme. The 2025 budget targeted a primary surplus of 1.5 percent of GDP, supported by enhanced domestic revenue mobilisation and expenditure rationalisation. Preliminary mid-year data indicated a primary surplus of about 1.1 percent of GDP by June 2025, exceeding initial expectations. Public debt, which peaked at an estimated 92.4 percent of GDP in 2022, declined to approximately 85 percent by 2023 following domestic debt exchanges and external restructurings. Nonetheless, fiscal risks persist, largely stemming from commodity price volatility and the potential for policy slippages.

The external sector strengthened considerably in 2025. A current account surplus was recorded, driven by robust gold and cocoa exports. The Ghanaian cedi appreciated by more than 40 percent against the US dollar by mid-2025, reversing the sharp depreciation experienced during the crisis period. Gross international reserves increased to cover about 4.8 months of imports, enhancing external buffers and investor confidence. These developments underscore the importance of effective macroeconomic management alongside economic diversification efforts.

Financial Systems

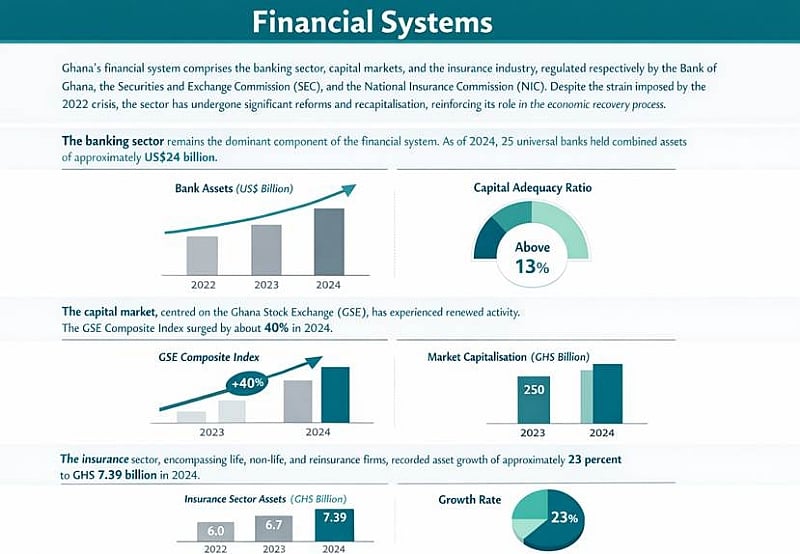

Ghana’s financial system comprises the banking sector, capital markets, and the insurance industry, regulated respectively by the Bank of Ghana, the Securities and Exchange Commission (SEC), and the National Insurance Commission (NIC). Despite the strain imposed by the 2022 crisis, the sector has undergone significant reforms and recapitalisation, reinforcing its role in the economic recovery process.

The banking sector remains the dominant component of the financial system. As of 2024, 25 universal banks held combined assets of approximately US$24 billion. The domestic debt restructuring adversely affected bank balance sheets, necessitating regulatory intervention and recapitalisation measures. By 2025, the majority of banks had restored capital adequacy ratios above the regulatory threshold of 13 percent, supported in part by the Ghana Financial Stability Fund. Although non-performing loans remain elevated, profitability improved markedly, with after-tax profits rising by roughly 33 percent during the first nine months of 2025. Continued emphasis on liquidity management and prudential supervision has underpinned stability amid declining interest rates. Financial inclusion has expanded through mobile money and digital banking platforms, although access gaps persist in rural and underserved communities.

The capital market, centred on the Ghana Stock Exchange (GSE), has experienced renewed activity. The GSE Composite Index surged by about 40 percent in 2024 and continued to rise in 2025, with market capitalisation increasing by more than 50 percent. Despite these gains, market depth remains limited, as only 11 of the 25 universal banks are publicly listed. Regulators have therefore encouraged additional listings to enhance liquidity and long-term financing. The fixed-income market remains active, though secondary trading is relatively shallow. New SEC capital and liquidity requirements introduced in 2025 have strengthened market resilience.

The insurance sector, encompassing life, non-life, and reinsurance firms, recorded asset growth of approximately 23 percent to GHS 7.39 billion in 2024. Premium growth has been supported by regulatory reforms, including the adoption of IFRS 17 and the implementation of risk-based supervision. The NIC’s Insurance Sector Strengthening Strategy, launched in 2025, seeks to improve solvency, deepen penetration, and expand access to products such as microinsurance.

The insurance sector, encompassing life, non-life, and reinsurance firms, recorded asset growth of approximately 23 percent to GHS 7.39 billion in 2024. Premium growth has been supported by regulatory reforms, including the adoption of IFRS 17 and the implementation of risk-based supervision. The NIC’s Insurance Sector Strengthening Strategy, launched in 2025, seeks to improve solvency, deepen penetration, and expand access to products such as microinsurance.

Interconnections and Key Challenges

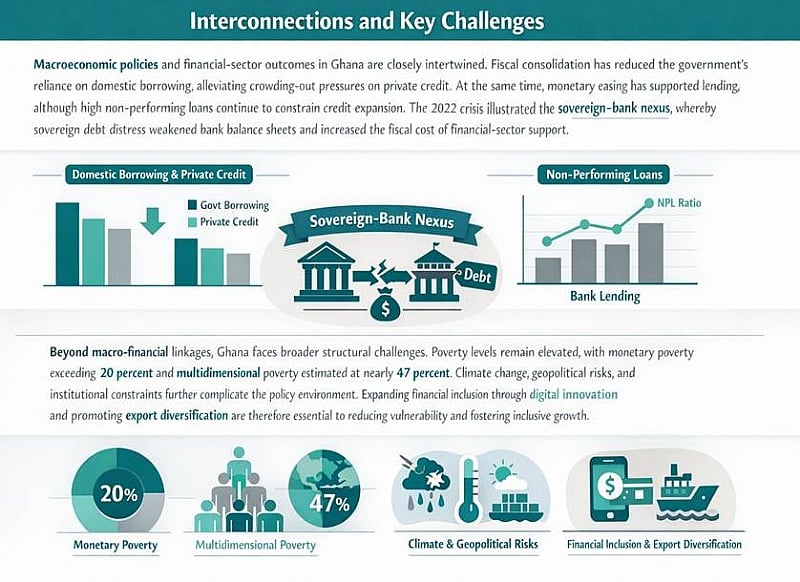

Macroeconomic policies and financial-sector outcomes in Ghana are closely intertwined. Fiscal consolidation has reduced the government’s reliance on domestic borrowing, alleviating crowding-out pressures on private credit. At the same time, monetary easing has supported lending, although high non-performing loans continue to constrain credit expansion. The 2022 crisis illustrated the sovereign–bank nexus, whereby sovereign debt distress weakened bank balance sheets and increased the fiscal cost of financial-sector support.

Beyond macro-financial linkages, Ghana faces broader structural challenges. Poverty levels remain elevated, with monetary poverty exceeding 20 percent and multidimensional poverty estimated at nearly 47 percent. Climate change, geopolitical risks, and institutional constraints further complicate the policy environment. Expanding financial inclusion through digital innovation and promoting export diversification are therefore essential to reducing vulnerability and fostering inclusive growth.

Beyond macro-financial linkages, Ghana faces broader structural challenges. Poverty levels remain elevated, with monetary poverty exceeding 20 percent and multidimensional poverty estimated at nearly 47 percent. Climate change, geopolitical risks, and institutional constraints further complicate the policy environment. Expanding financial inclusion through digital innovation and promoting export diversification are therefore essential to reducing vulnerability and fostering inclusive growth.

Conclusion

Ghana’s recent macroeconomic recovery characterised by renewed growth, disinflation, and external stabilization has reinforced the resilience of its financial system. Banking-sector recapitalisation, capital-market revitalisation, and insurance-sector reforms constitute important pillars of this recovery. Nevertheless, sustaining progress will require continued policy discipline, strong institutions, and proactive risk management in the face of global uncertainty. By strengthening the alignment between macroeconomic policy and financial-system development, Ghana has the potential to achieve inclusive and sustainable growth and to serve as a reference point for other emerging and frontier economies.

Written by: Gaeten Akanwarisage Agbaam (Development Finance Analyst)

References

African Development Bank Group (2025). Ghana Economic Outlook.

Bank of Ghana (2025). Monetary Policy Report.

International Monetary Fund (2025). Ghana: Fifth Review under the Extended Credit Facility.

Ministry of Finance, Ghana (2025). Mid-Year Fiscal Policy Review.

S&P Global Ratings (2025). Research Update: Ghana.

World Bank (2025). Ghana Economic Update.

Accra Is Sinking Yet Again — Time to Be Truthful With Ourselves

Accra Is Sinking Yet Again — Time to Be Truthful With Ourselves

Fire guts rubber factory at Circle Odawna as flooding hampers firefighting effor...

Fire guts rubber factory at Circle Odawna as flooding hampers firefighting effor...

Flooding strands commuters on Winneba Cape Coast Highway

Flooding strands commuters on Winneba Cape Coast Highway

Three feared dead after electrocution in Alajo flooding incident

Three feared dead after electrocution in Alajo flooding incident

Nine missing after floods hit Awutu Senya East

Nine missing after floods hit Awutu Senya East

'Your mother, I should go to heaven and ask Nebuchadnezzar to stop the rain?' — ...

'Your mother, I should go to heaven and ask Nebuchadnezzar to stop the rain?' — ...

Flood victim found dead along Alajo Railway track as rescue operations continue

Flood victim found dead along Alajo Railway track as rescue operations continue

GMet warns more rain as flooding disrupts movement across Greater Accra

GMet warns more rain as flooding disrupts movement across Greater Accra

'You sit on social media and talk nkwasiasem' — Nigel Gaisie blasts critics over...

'You sit on social media and talk nkwasiasem' — Nigel Gaisie blasts critics over...

Osahen Afenyo-Markin accuses NDC of using GoldBod to promote illegal mining

Osahen Afenyo-Markin accuses NDC of using GoldBod to promote illegal mining