1.0 Introduction

The global shift toward sustainability and climate-related financial disclosures has seen the International Financial Reporting Standards (IFRS) Foundation introduce two new sustainability standards: IFRS S1 (General Requirements for Disclosure of Sustainability-related Financial Information) and IFRS S2 (Climate-related Disclosures). In Ghana, State-Owned Enterprises (SOEs) are required to adopt these standards to align with global practices and enhance transparency, governance, and resilience in their operations.

This article explores the roles of SOE Boards, State Interests and Governance Authority, Institute of Chartered Accountants Ghana, and other regulators in implementing IFRS S1 and S2, emphasizing the need for capacity building and outlining the interaction between SOEs and the broader business ecosystem. The operational dynamics of Metro Mass Transit (MMT) and Intercity STC Coaches Limited serve as practical illustrations.

2.0 The Board's Role in Implementation

SOE boards play a critical role in ensuring the successful implementation of IFRS S1 and S2. These responsibilities include:

- Strategic Oversight: Boards must align corporate strategy with sustainability goals, ensuring that long-term planning integrates climate-related and broader ESG (Environmental, Social, and Governance) considerations.

- Policy Development: Boards should develop or refine policies on sustainability reporting, risk management, and stakeholder engagement to meet IFRS S1 and S2 disclosure requirements.

- Monitoring and Evaluation: Continuous assessment of sustainability performance and disclosure quality is vital. Boards must demand regular reports and verify that management applies the standards appropriately.

- Capacity Support: Boards must ensure that management and staff are adequately trained and that resources are allocated to support sustainability disclosures.

- Accountability and Governance: Boards must uphold ethical leadership, transparency, and accountability in sustainability practices.

3.0 Role of SIGA and Other Regulators

The State Interests and Governance Authority (SIGA), as the oversight body for specified entities, has a mandate to promote good corporate governance and ensure value for money in SOEs. In the context of IFRS S1 and S2, SIGA’s roles include:

- Guidance and Standardization: Issuing directives that guide SOEs on uniform implementation and reporting structures.

- Performance Contracting: Embedding sustainability and climate-related KPIs in performance contracts.

- Monitoring Compliance: Evaluating implementation progress and ensuring SOEs meet their reporting obligations.

- Coordination with Regulators: Working with the Institute of Chartered Accountants, Ghana (ICAG), the Ministry of Finance, the Environmental Protection Agency (EPA), and the Securities and Exchange Commission (SEC) to enforce sustainability standards.

4.0 ICAG’s Directive and Capacity Building

The ICAG, as the accounting standards setter in Ghana, issued a directive mandating all entities under its jurisdiction to begin preparations for adopting IFRS S1 and S2. It emphasizes phased implementation, beginning with high-impact sectors such as transport, energy, and extractives. ICAG’s support includes:

- Training Programs: Building the competence of finance professionals through workshops, certifications, and knowledge-sharing platforms.

- Technical Guidance: Providing tools, templates, and advisory notes on interpreting and applying the new standards.

- Collaboration with Academia: Partnering with tertiary institutions to integrate sustainability accounting into curriculum and professional development programs.

Capacity building is pivotal. Boards, accountants, operational managers, and internal auditors must understand the implications of sustainability risks and opportunities on financial performance. This requires sustained investment in people, systems, and processes.

5.0 Value Chain Implications: Example the Case of STC and Metro Mass Transit

IFRS S1 and S2 will impact the entire value chain of SOEs. Consider the operations of Metro Mass Transit and Intercity STC:

- Fuel and Fleet Management: These entities must disclose emissions data, fuel efficiency metrics, and strategies for reducing environmental impact.

- Procurement: Suppliers will be required to provide sustainability credentials, influencing the selection of partners and products.

- Customer Services: Climate risks affecting routes, infrastructure, or customer safety must be disclosed under IFRS S2.

- Human Resources: Disclosures must include how employee training, welfare, and diversity contribute to sustainability objectives.

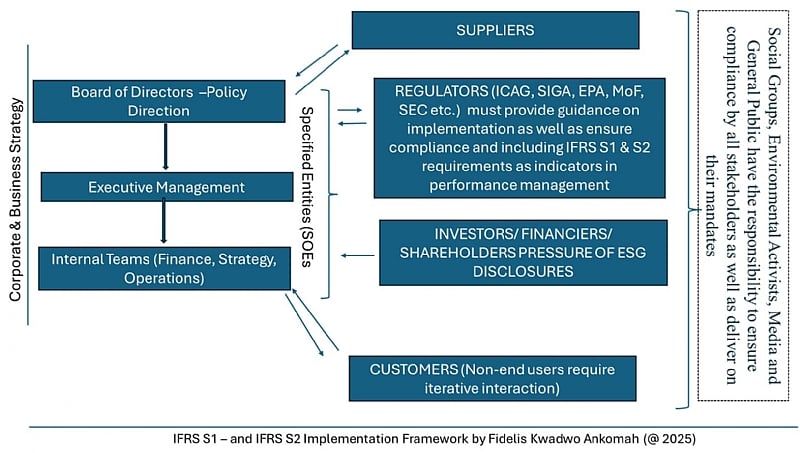

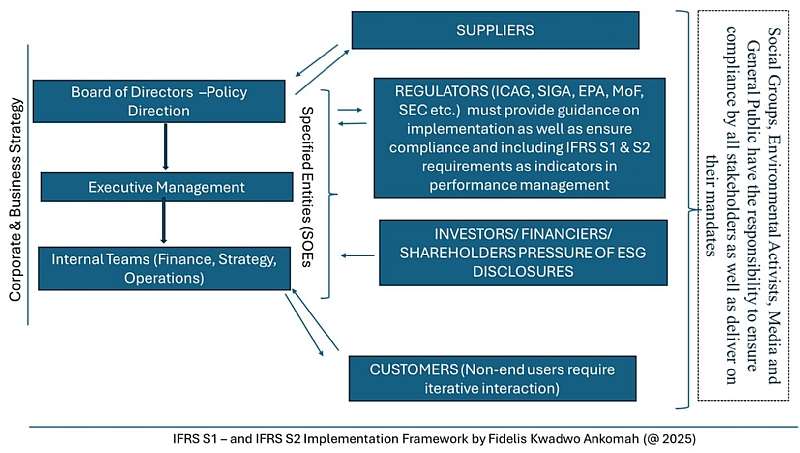

6.0 Stakeholder Ecosystem in the Implementation of IFRS S1 and IFRS S2 by State-Owned Enterprises

The implementation of IFRS S1 and IFRS S2 - sustainability-related financial disclosure standards developed by the International Sustainability Standards Board (ISSB) requires a coordinated, multi-stakeholder approach. This is especially critical within State-Owned Enterprises (SOEs), where governance, transparency, and accountability are essential for achieving public interest outcomes. The stakeholder interaction framework below provides a visual representation of how key players align in the successful adoption of these standards.

Figure 1: IFRS S1 – and IFRS S2 Implementation Framework: Proposed Guide for SOEs in Ghana

At the core of implementation is the internal governance structure of SOEs. The Board of Directors plays a strategic leadership role by setting policy direction and sustainability priorities. Their mandate flows through to Executive Management, who are responsible for operationalizing this direction and aligning resources and systems to support compliance. The Internal Teams, such as Finance, Strategy, and Operations, are tasked with embedding IFRS S1 and S2 principles into business processes, collecting relevant data, and preparing sustainability disclosures.

Externally, the role of regulators is pivotal. Institutions like the Institute of Chartered Accountants, Ghana (ICAG), State Interests and Governance Authority (SIGA), Environmental Protection Agency (EPA), Ministry of Finance (MoF), and the Securities and Exchange Commission (SEC) are charged with guiding the implementation process. They are expected to issue technical guidance, monitor compliance, and include IFRS S1 and S2 metrics as part of SOE performance evaluation frameworks.

Investors, financiers, and shareholders are increasingly demanding Environmental, Social, and Governance (ESG) disclosures, putting pressure on SOEs to demonstrate sustainability performance. This not only impacts capital access but also affects public trust and legitimacy.

Suppliers, as integral parts of the value chain, must align with the SOE’s sustainability goals. This means the SOE must engage them to ensure that upstream and downstream activities comply with IFRS S1 and S2 expectations, such as climate-related risk disclosures and sustainability-related opportunities.

Customers, particularly non-end users, play a more iterative role. These stakeholders require ongoing engagement and transparency to meet their own sustainability objectives or reporting requirements.

Finally, broader societal actors—including social groups, environmental activists, media, and the general public—serve as accountability agents. Their role is to ensure all stakeholders not only comply with mandates but also contribute meaningfully to sustainable development and climate resilience.

This ecosystem-based approach underscores that the implementation of IFRS S1 and S2 is not just a compliance exercise, but a transformation in how SOEs operate, report, and relate to their environments. It demands robust governance, institutional coordination, and sustained stakeholder engagement across the value chain.

7.0 Conclusion

The implementation of IFRS S1 and S2 marks a transformative era for SOEs in Ghana. With proactive leadership from Boards, oversight from SIGA, technical direction from ICAG, and cross-sector capacity building, Ghanaian SOEs can lead the continent in sustainable governance and disclosure. STC and Metro Mass Transit exemplify how transport SOEs can embed sustainability into their core operations, ensuring resilience and public accountability in an era defined by climate and ESG imperatives.

References:

- IFRS S1 - General Requirements for Disclosure of Sustainability-related Financial Information

- IFRS S2 - Climate-related Disclosures

- The Institute of Chartered Accountants Press Release on IFRS Sustainability Disclosure Adoption Roadmap For Ghana

AG withdraws charges against former buffer stock CEO Hanan and wife as EOCO re-a...

AG withdraws charges against former buffer stock CEO Hanan and wife as EOCO re-a...

Images and videos of military clearing lands for Accra–Kumasi expressway project

Images and videos of military clearing lands for Accra–Kumasi expressway project

What should give you satisfaction is that your work has helped saved Ghana from ...

What should give you satisfaction is that your work has helped saved Ghana from ...

ECG announces emergency maintenance in Ashanti, Western Regions today

ECG announces emergency maintenance in Ashanti, Western Regions today

Police arrest two cocoa purchasing clerks for allegedly short-changing farmers i...

Police arrest two cocoa purchasing clerks for allegedly short-changing farmers i...

Korle-Bu doctors strike suspended, OPD services resume Tuesday

Korle-Bu doctors strike suspended, OPD services resume Tuesday

May 5: Cedi sells at GHS12.15 on forex market, drops to GHS11.23 on BoG interban...

May 5: Cedi sells at GHS12.15 on forex market, drops to GHS11.23 on BoG interban...

NAiMOS cracks down on multinational galamsey syndicate in Mankraso

NAiMOS cracks down on multinational galamsey syndicate in Mankraso

Amin Adam runs to IMF to take action on BoG recapitalisation, gold sales and mon...

Amin Adam runs to IMF to take action on BoG recapitalisation, gold sales and mon...

PNDC era second gravest crime against humanity after slavery — Miracles Aboagye

PNDC era second gravest crime against humanity after slavery — Miracles Aboagye