When the 2018 budget and economic policy was read last year with its accompanying commendable policy initiatives and the nation was geared up and prepared to help promote such agenda. Among other things, were some tax policy initiatives particularly income tax that were also highlighted. Most of the tax initiatives have already been passed into acts of provisions as amendment to the Income Tax Act, 2015 (Act 896) by the Income Tax (Amendment) (No. 2) Act, 2017 (Act 956). However, there are some of the income tax policy initiatives that I think its intention of helping taxpayers and ensuring fairness in income tax administration is more of a mirage than a reality. In no particular order, I share my opinion on some of such as follows.

Policy 1 - Income Tax Threshold

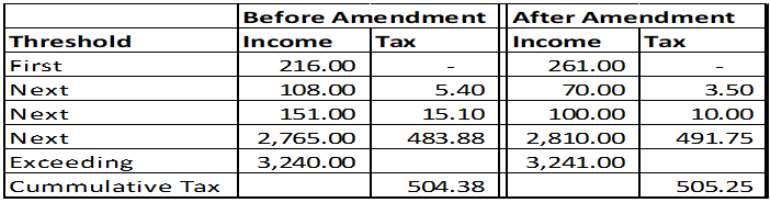

The 2018 budget highlights envisioned to review the current income tax thresholds by pegging the tax-free threshold to the new minimum wage to protect low income earners and ensure fairness in our income tax administration. In achieving same, the tax-free threshold as per the First Schedule of the Income Tax Act 2015, (Act 896) has been amended, with the tax-free threshold now increased from GHS216 to GHS261, resulting from the 10% increase in the daily new minimum wage (i.e. GHS8.80 to GHS9.68). This is a commendable tax policy for income earners especially for the “low-income earners” as stated in the 2018 budget keynotes. My concern is why open the tax-free threshold only to close the other thresholds to increase tax if the rational is to ensure fairness in the income tax administration? Or must we pretend to be doing something? Besides, it is also not clear how much a person earns is considered a low income for which such income tax review was done but from analysis it appears it relates to people who earn less than GHS500. Could that be the definition of a low-income earner for this purpose? And how many people in the formal sector (who are already paying tax) earn below such amount?

For instance, below is the chargeable income and corresponding tax payable (using monthly PAYE) before and after the amendment of Income Tax Act 2015 (Act 896) as contained in Income Tax (Amendment) (No.2) Act, 2017 Act 956.

It is obvious that tax payable in the supposed income tax review has increased from GHS504.38 to GHS505.25, of about GHS0.87. Though, in absolute terms it appears insignificant, consider a situation where there are about 3,000,000 or more people in the formal sector and if your calculation is correct, the government is now making additional tax revenue of about GHS2.6m from the same people this amendment is intended to help. Also, by extension, for those who earn above GHS500, their minimum wage is no more the mandated GHS9.68 but rather GHS8.81. How can this be fair? If you cannot give us more, why take what we already have?

Mr. Finance Minister, should taxpayers indeed be jubilating over this tax policy initiative as a step in the right direction for making money available to the citizenry? And if this tax policy initiative had made income better, aren’t taxpayers likely to increase their consumption with its associated more VAT collections? “Me I can’t think far”

Policy 2 - Tax Exemptions for Private Universities

Part of the 2018 budget tax initiatives is to offer Tax Breaks to help position Ghana as a Higher-Education Hub and in accordance with that, the Income Tax Act, 2015 (Act 896) was amended accordingly with Income Tax (Amendment) (No.2) Act, 2017 (Act 956) to cater for such policy drive.

According to the new Act (i.e. Act 956), privately-owned universities shall be exempted from tax when they plough back a hundred percent of their profit-after-tax into the business. This means that a university that ploughs back less than a hundred percent profit-after-tax automatically becomes liable to the usual tax.

I find it difficult to agree that this is considered a tax incentive to the supposed universities for which the privately-owned universities should be happy about because I wonder if there is any such privately-owned university to meet this criterion. Besides, are there entities in the global economies that will do this hundred percent profit-after-tax plough back when shareholders have personal interest in the declared profit? And if there are, for how long will this be? Or are we concluding that the universities are individually owned and that there are no other individual and/or institutional investors that might expect some returns via dividend from their investment?

Mr. Finance Minister, I think you need to come again on this supposed tax incentive for the private universities as it appears this is more of a tax incentive possibly only on paper than in practice because I can hardly see any privately-owned university benefiting from this. Besides, is so discretionary to say, plough back hundred percent of profit-after-tax whiles you don’t specify the type of activities such profit-after-tax should go into. Why not attach this exemption to some defined expenditures in business?

Policy 3 - Tax Exemption for Young Entrepreneurs

The sixth schedule of Act 896 has also been amended by the same Act 956 to include that the income of young entreprenuers from the business of manufacturing, information and communications technology, agro processing, energy production, waste processing, tourism and creative arts, horticulture and medical plants shall be exempted from tax for a period of five years, after which concessionary tax rates will be applied depending on the location of the business. The act specifically says, “young entrepreneurs” and goes further to define “young entrepreneurs” for this purpose as one who is not more than thirty-five years old. It also provides that, the person may carry forward an unrelieved loss for a five years basis period. Simply put, such an entrepreneur will not pay tax for the entire five years of operation whiles income and corresponding profits are made in those periods and where losses are made, the person can carry forward the loss for a five-year basis period. A “young entrepreneur” therefore has the potential to enjoy more than five years of tax exemption (say 5yrs tax exemption and 5yrs losses carry over) which is a highly commendable and welcoming news for these entrepreneurs. So, entrepreneurs who are say 36 years are called what? Maybe “old entrepreneur”?

That notwithstanding, let me hasten to add that, a similar tax exemption is provided under Regulation 19 of the Income Tax Regulations, 2016 (LI. 2244). Under the regulation, a person operating in a “priority sector” is allowed to deduct an unrelieved loss of the person for any of the five (5) previous years of assessment. The priority sectors as per the said regulations are minerals and mining operations, petroleum operations, energy and power business, manufacturing business, farming business, agro processing business, tourism business and information and communication business. How different are these priority sectors from what is stated for the “young entrepreneurs”? Yet these businesses do not enjoy any tax exemption and after the five-year period that unrelieved losses are deducted, the usual corporate taxes are applicable unlike the “young entrepreneurs” who have preferential locational tax rebates ranging from 5% to 15%. I guess this is where the “old entrepreneurs” years fall into. A good policy?

But one will wonder, is this very tax exemption policy not very discriminative in nature though taxation is supposed to be fair? And has the definition of entrepreneurs currently been modified to include age of persons or entrepreneurship has now become the reserved right of people who are not more than thirty-five years old? Why not set some criteria (like say create some number of employment etc.) for granting the exemption like is done for the privately-owned universities? Do we intend to use this to ensure fairness in tax administration? I can only imagine!

Mr. Finance Minister, don’t you think this “young entrepreneur” tax exemption is a duplication of an already existing tax policy as such provision already exists for all type of business be it “young entrepreneur” or “old entrepreneur” in the Income Tax Regulation, 2016 (LI. 2244)? And don’t you also think this kind of policy will create an unfair playing ground for people in the same business environment or in the entrepreneurship space? What if the business liquidates after the exemption period, the loss carry forward period or both?

Conclusion

There are no doubt other tax policy initiatives such as the Alternative Dispute Resolution, Voluntary Disclosure Procedure, One-off Tax Amnesty etc. has a long-term effect on income tax administration in Ghana. Taxpayers are ready to help improve income tax administration for increased tax revenue and to move Ghana beyond aid as envisioned by the President, but if such tax policies are structured like this, then your guess will be as good as mine.

About the Author

A Financial Reporting/Analysis, Audit and Tax professional, a Consultant at Danisa Consult (Accounting, Audit & Tax) and a Facilitator for Accounting, Tax and Audit at Global Institute of Resource Development (GiRD), a Capacity Development and Training Institution. A member of the Institute of Chartered Accountant, Ghana; Chartered Institute of Taxation, Ghana; Association of International Accountants, UK; International Association of Accounting Professionals, UK; Association of Certified Fraud Examiners, US; Southern African Institute for Business Accountants, SA.

Comments and suggestions to [email protected] /0242844114

Atta Akyea takes over from Andy Appiah Kubi as lawyer for Wontumi’s Samreboi cas...

Atta Akyea takes over from Andy Appiah Kubi as lawyer for Wontumi’s Samreboi cas...

Woman loses temper, fights mentally challenged lady over alleged disrespect

Woman loses temper, fights mentally challenged lady over alleged disrespect

WHO welcomes UK's move to ban social media access for children under 16

WHO welcomes UK's move to ban social media access for children under 16

June 15: Cedi appreciates, sells at GHS12.30 on forex market, GHS11.06 on BoG in...

June 15: Cedi appreciates, sells at GHS12.30 on forex market, GHS11.06 on BoG in...

Samreboi case: How rejection of Appiah Kubi's withdrawal could offer Wontumi a p...

Samreboi case: How rejection of Appiah Kubi's withdrawal could offer Wontumi a p...

UK to ban under-16s from social media over safety and mental health concerns

UK to ban under-16s from social media over safety and mental health concerns

Samreboi case: Appiah Kubi cites disappointment with court in withdrawal applica...

Samreboi case: Appiah Kubi cites disappointment with court in withdrawal applica...

ECOWAS mourns demise of former Commission President James Victor Gbeho

ECOWAS mourns demise of former Commission President James Victor Gbeho

Andy Appiah Kubi's application to withdraw as Lawyer for Wontumi in Samreboi ill...

Andy Appiah Kubi's application to withdraw as Lawyer for Wontumi in Samreboi ill...

I’ll file a notice of withdrawal and leave the case—Appiah Kubi on next line of ...

I’ll file a notice of withdrawal and leave the case—Appiah Kubi on next line of ...