Every strong economy reflects its robust Banking and Financial Sector. The Banking industry in Ghana has seen significant developments over the last few years. Key amongst them is the strictest action taken by the Central Bank of Ghana to revoke license of some of the banks in 2017/2018 thereby reducing the number of commercial banks to Twenty-Three (23). The effect of that decisive action to a large extent changed the phase of the financial sector in Ghana

On Thursday, March 13, 2020, Ghana's Ministry of Health confirmed the first two cases of the coronavirus (COVID-19) in Ghana, the numbers escalated, and the country unfortunately lost a few lives. The economy was not spared, the Government and the Bank of Ghana had to put in place some drastic measures to alleviate the situation. From a global perspective, the devastating effect pushed some economics into recession. While some key sectors and businesses were shutting down and struggling to survive, the likes of the Technology, Fintech and the Telecom sectors were booming.

Could that be said of the banking sector in Ghana? I spent some time to delve into the recently published 2021 audited financial statements of 19 out of the 23 banks. In this article I shall attempt an assessment of the impact of the recent challenges on the bank’s performance. I do not intend to show good or underperforming banks, instead, I will present an objective and a holistic view of their performances for the year under review.

Profitability and Earnings

To measure the performance of a bank, every manager, shareholder, or investor would be interested in profitability indicators, since profits are the ultimate goal of banks. The profit a bank makes is also a matter of key interest for managers and investors when making strategic decisions. All strategies designed and the activities implemented are aimed at realising this great goal.

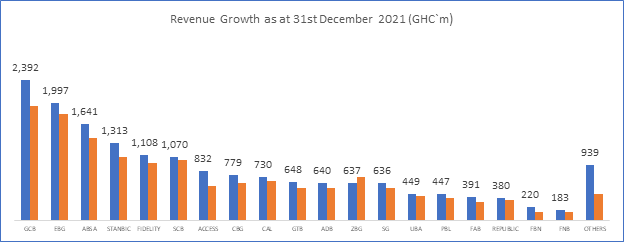

The Banking industry headline revenue for the year ending 2021 grew to Ghs17.43m (2020: Ghs15.2m) representing a 14.6% growth year on year. GCB Bank maintained the top position with a revenue of Ghs2.39m (2020: Ghs1.94m) with an increased market share of 13.7%. GCB performance was up by 23.4% year on year. The second position was closely held by Ecobank who closed the year at Ghs1.99m with marginally declined market share of 11.5% (2020:11.9%). With the exceptions of Zenith Bank Ghana Limited that declined in year-on-year growth by 13% thus from Ghs732m in 2020 to Ghs637m in 2021, the rest of the banks saw an increase in revenue.

Interestingly, the top 6 banks (GCB, Ecobank, Absa Bank, Stanbic, Fidelity and Standard Chartered) crossed the Ghs1m revenue mark and contributed 55% of the overall industry revenue. From a Net Interest Income (NII) and Non-Funded Income (NFI) perspective, while Republic Bank was growing its NII by over 50% to Ghs299m year on year, Stanbic Bank managed to increase transactional fees by 42% to Ghs857m; the highest NFI growth on the market since 2019. It was obvious that, while other banks are given waivers and reduction on pricing to clients, some banks increased their volume of activities to drive its fee income.

Source: Audited Financial Statements as of 31st December 2021

Source: Audited Financial Statements as of 31st December 2021

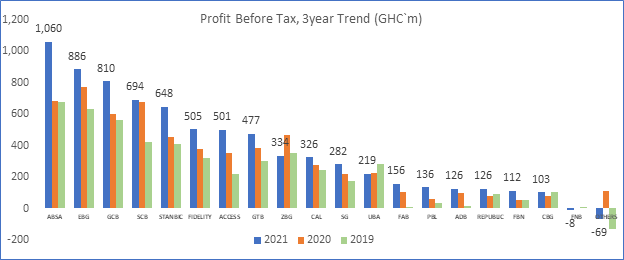

In view of the ongoing pandemic, the industry’s Profit Before Tax (PBT) increased to Ghs7.42m (2020: Ghs6.08m). Despite the various challenges, growth in Operating profit remained impressive across the industry, averaging c. 22% (2020: 27%). However, this double-digit growth could not match the 2020 performance when COVID 19 was at its peak. Banks like Zenith and UBA saw a dip in PBT by 28.4% and 2.3% respectively. Though Ecobank was impressive on its revenue performance, Absa maintained it’s the top position as the most profitable bank, closing the year at Ghs1.06m (2020: Ghs883m) with a market share of 14.3%. It is important to mention that, following the decoupling of Barclays from the Barclays Africa Group Limited`s business few years ago, Financial Analyst were of the view that, this move could have impacted on the bottom line. However, the bank continues to demonstrate strong performance both in revenue and balance sheet. This also reaffirms the need to strengthen Regional and Local Banks to stand the test of time.

Ecobank, GCB and Standard Chartered were ranked 2nd 3rd and 4th respectively. It`s therefore an established fact that while some industries and sectors were struggling to stay afloat amidst the pandemic season, Commercial Banks were generally profitable.

Source: Audited Financial Statements as of 31st December 2021

Source: Audited Financial Statements as of 31st December 2021

| Banks | ABSA | ECOBANK | GCB | STANBIC | SCB | |||||

| Key Profitability Ratios | 2021 | 2020 | 2021 | 2020 | 2021 | 2020 | 2021 | 2020 | 2021 | 2020 |

| Return on equity | 30% | 24% | 22% | 22% | 22% | 21% | 21% | 19% | 27% | 33% |

| Return on assets | 4% | 4% | 3% | 3% | 3% | 3% | 3% | 3% | 4% | 6% |

| Return on earning assets | 6% | 5% | 4% | 5% | 4% | 3% | 4% | 4% | 7% | 11% |

| Net Profit Margin (PAT to Revenue) | 42% | 34% | 29% | 30% | 23% | 23% | 31% | 30% | 41% | 47% |

| EVA | 312 | 140 | 139 | 132 | 135 | 91 | 82 | 41 | 165 | 229 |

| NII to total income | 66% | 69% | 75% | 74% | 79% | 77% | 50% | 57% | 60% | 63% |

| NFI to total income | 34% | 31% | 25% | 26% | 21% | 23% | 50% | 43% | 40% | 37% |

| Ave. cost on interest bearing liabilities | 3% | 4% | 1% | 2% | 3% | 3% | 2% | 2% | 2% | 3% |

| Gross yield on ave. earning assets | 12% | 13% | 13% | 15% | 16% | 15% | 9% | 10% | 13% | 18% |

| Net interest spread (NIM) | 9% | 9% | 11% | 13% | 13% | 12% | 7% | 8% | 11% | 15% |

| Earnings per share (GH₵ per share) | 7.7 | 5.24 | 1.8 | 1.69 | 2.1 | 1.66 | n.a. | n.a. | 3.23 | 3.54 |

Source: Audited Financial Statements as of 31st December 2021

Capital Adequacy

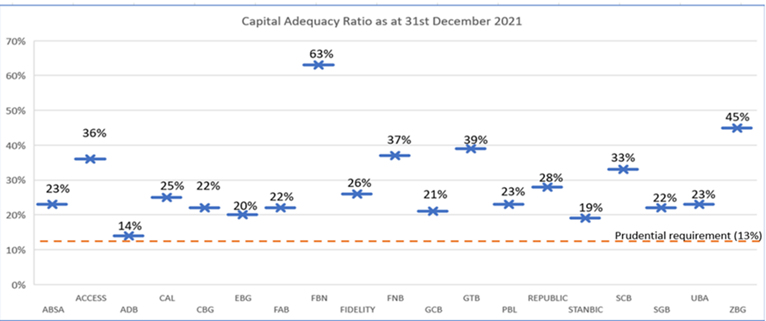

Every bank’s capital adequacy is assessed based on Capital Adequacy Ratio (CAR). It generally reflects the internal wealth of a bank’s ability to withstand losses in case of economic crises just like the situation presented by the ongoing pandemic. The higher value of this ratio reflects the better resilience ability of a bank to crisis situations.

Based on the reviews, Commercial banks continued to demonstrate their commitment to maintaining a strong capital base to protect shareholder interest. They also enhanced capacity to serve their customers, foster investor confidence and absorb current and future risks attendant with the business of banking by instituting a more robust corporate governance structure in the credit appraisal process. This was evident in the attainment of an industry capital adequacy ratio above the regulatory minimum of 13% as at the end of 2021. ADB may have closely looked at the ongoing accumulated losses on balance sheet to return to profit to increase the Tier 1 capital.

Source: Audited Financial Statements as of 31st December 2021

Asset Quality

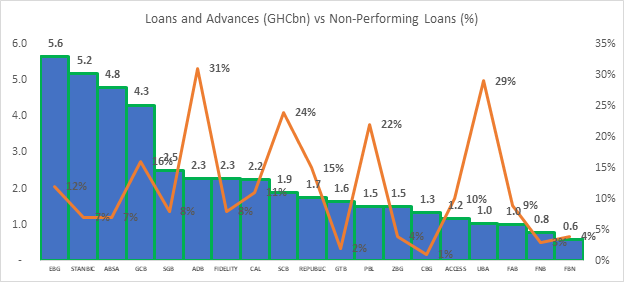

The quality of a loan portfolio has a direct effect on a bank’s profitability. The highest risk that commercial banks face is the losses from overdue debts. Different types of financial ratios are used as proxies for bank performance. One of the major concerns of all commercial banks is keeping the number of Non-Performing Loans (NPL) at the barest minimum. Unsuitable loans will negatively affect bank profitability. Therefore, the more unsuitable the loans, the higher the total amount of loans and the better the health of the bank’s portfolio. What it means is that the lower NPL ratio, the better the bank operates.

In accessing the financials, one would have thought that the ongoing pandemic would have slowed down asset growth however, the Industry Asset growth saw an increase to 20% in 2021 (2020: 16%) from Ghs149.3bn from 2020 to Ghs179.8bn in 2021.Interestingly only 24% (Ghs43.4bn) were held in Loans and Advances and this demonstrated that, even though some commercial banks were lending, they took a cautious stance on credit or lending. While Banks like GCB and Ecobank held 10.2% and 9.9% market share respectively. Stanbic, CBG, Zenith etc dropped market share of Total Assets to 7.8%, 6% and 4.9% respectively. Absa, Fidelity, SCB etc also saw an increase in Asset market share position to 8.9%, 7.4% and 5.6% respectively. In all, GCB retained the top bank with biggest Total Assets of Ghs18.3bn with 19% year on year growth while Ecobank ranked 2nd with a Total Assets of Ghs17.86bn but with a 12% growth.

Furthermore, as observed by the Monetary Policy Committee (MPC) of the Central Bank, the volume of funding channeled into investments continued to experience marked increases mainly triggered by ‘elevated credit risk’ and ‘high yields offered on Government securities due to increased Government borrowing. Total Investments increased by 29%year on year to Ghs82.9m (2020: Ghs64.2bn) and accounted for 46% of the Total Assets. What this means is that over 70% of the Assets were held in Loans and Advances and Earning Assets. This confirms the general assertion made by industry analysts that, banks continue to run to secured investments as against increasing risk exposures to the private sector. The higher investments growth was attributed to banks’ portfolio reallocation in favour of these less risky assets due to the elevated credit risks and somewhat sluggish credit demand due to the impact of the pandemic.

Source: Audited Financial Statements as of 31st December 2021

Liquidity positions

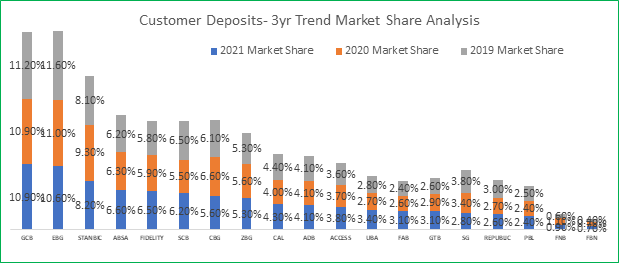

Generally, Liquidity refers to a commercial bank’s ability to perform its obligations, primarily to the depositors who have funds with them. Though there are several ratios such as Liquidity and Coverage ratios, the most widely used ratios reflecting the commercial bank’s liquidity position are the ratio of customers’ deposit to total assets and total customer deposits.

While Total Assets grew by 20%, Industry Liabilities saw a 17% year on year growth to Ghs121.1bn (2020: Ghs103.8bn). GCB ranked no. 1 with the highest deposit of Ghs13.2m, maintaining a flat market share of 10.9%. UBA and First Atlantic Bank significantly grew their deposit base by 46% and 42% respectively. This is also a reflection of their strategy to drive deposits through various products and customer initiatives. With the exceptions of CBG, Société General and FNB who dipped on deposit mobilisation by 2%, 3% and 7% respectively, all other banks increased their liquidity position. Most of the banks sitting on huge deposits are largely on the back of Mobile Money partnerships with the Telcos.

Source: Audited Financial Statements as of 31st December 2021

Management Efficiency

The quality of Bank managers is a significant component in sustaining a bank as a going concern. The competence and working style of a Board of Directors and Management, has a ripple effect on a bank’s operating profit over its total revenue. The various Board of Directors in the banks continued to have full oversight in several areas including Risk, Capital, Credit Risk Management Frameworks etc. Though there were few changes in the management and Board of Directors in 2021, this was done in accordance with statutory requirements and the various banks’ regulations. The roles of the Chief Executive Officers and Board Chairmen continue to be separated for all the banks.

Conclusion and recommendations

While there is keen competition, The banking sector was strong, solvent and profitable amid the COVID-19 pandemic in 2021. The sustained increases in deposits, total assets, profits, and shareholder funds have significantly contributed to the industry’s resilience. It is important to highlight that, the policy measures and regulatory reliefs introduced by the Bank of Ghana to cushion the sector from the COVID-19 effects moderated the adverse impact of the pandemic on the industry.

Some of these response measures can remain in force to support activities of corporates and households, particularly those that were adversely hit by the pandemic. The outlook for the banking industry in 2022 therefore remains positive, and supportive of the economic recovery in the medium-term.

It was also observed that the Earning Assets (i.e., Investments in bills, securities and equity remained the largest component of total assets) increased by 30% year on year while loan and advances to customers grew by only 13% year on year. It is therefore recommended that Banks should make a conscious effort to open credit to private sector to boost and stimulate the growth of the real economy.

Mobile Money has come to stay and changing the payment landscape significantly. The banks who have taken advantage to partner with the Telcos were seen with huge floats. Banks should therefore work closely with the various Fintechs to deliver innovative products and solutions.

While NPLs seem to be watered-down for some of the banks, conscious effort and good Credit Risk management framework, controls should be adhered to bring the NPLs further down.

Thank you for reading.

Disclaimer: The views expressed are personal views and doesn’t represent that of the media house or institution the writer works.

About the writer

Carl Odame-Gyenti, PhD is a Banking, Finance, and Investment professional. Director, Banks & Broker Dealers with an International Bank in Ghana. Contact: [email protected] , Cell: +233 200301110

Gov't to invest GH₵2.5bn into second-cycle education infrastructure

Gov't to invest GH₵2.5bn into second-cycle education infrastructure

NDC to rename national headquarters after Rawlings, unveil bust on 79th birthday

NDC to rename national headquarters after Rawlings, unveil bust on 79th birthday

V/R: Two dead, farmlands destroyed as floods ravage Ketu North

V/R: Two dead, farmlands destroyed as floods ravage Ketu North

V/R: Flood waters submerge acres of farmland in Anloga

V/R: Flood waters submerge acres of farmland in Anloga

Al-Qaeda-linked jihadists attack Niger airport, 11 soldiers killed

Al-Qaeda-linked jihadists attack Niger airport, 11 soldiers killed

Ghana pushes for concrete slavery reparations

Ghana pushes for concrete slavery reparations

Fire destroys five-bedroom house; family, tenants rendered homeless

Fire destroys five-bedroom house; family, tenants rendered homeless

Timber Millers accuse, demand arrest of trade association members behind attack ...

Timber Millers accuse, demand arrest of trade association members behind attack ...

Two Christ the King SHS students injured in machete attack by suspected gang in ...

Two Christ the King SHS students injured in machete attack by suspected gang in ...

Controller plans salary deductions of 4,000 public sector workers who still owe ...

Controller plans salary deductions of 4,000 public sector workers who still owe ...