Lending rates in Ghana continue to be high. While the Bank of Ghana has maintained the monetary policy rate at 13.5% for the third time since May 2021. The various commercial banks continue to lend at an average interest rate of 20.6% which may in a way hurt the ability to deploy capital to private businesses. This is not new to businesses in Ghana and indeed there have been several calls by industry watchers and players to ensure that the yawning gap between the Central Bank’s monetary policy rate and the lending rate of commercial banks is bridged. While this may be true, efforts are being made by these financial institutions to bridge the seemingly huge gap.

The focus of this piece is to examine and explore how corporate organisations can leverage on their good standing or ratings with their respective commercial banks, to obtain cheaper sources of funding to support their internal supply chain management and take advantage of recent technologies and innovations in the space to provide such services to their clients.

A lot of companies are increasingly becoming aware that supplier relationship management is key to ensuring a strong supply base and now putting more emphasis on supply chain sustainability and good sourcing practices. This means that having a stronger collaboration with your key suppliers, yields greater value than having distant relationships. And here a supplier may refer to vendor providers such as those providing raw materials, water, tissue, stationaries, etc.

Global Outlook

Globally, a lot more companies have adapted to supply chain finance solutions to support their supply management. In fact, according to a report by Mckinsey in 2015, global supply chain finance revenue grew by 20% per year from 2010 to 2015, with a projected income growth of 15% per year expected within the next 5years. These numbers might have even been increased now.

Moreover, the supply chain finance market has outpaced the traditional trade finance market– as of 2016, supply chain finance comprised 54% of the total trade finance revenue pool and was expected to increase to up to 57% by 2020. With over $2 trillion in financeable payables globally as of 2016, supply chain finance represents potential revenue of over $20 billion. One of the most common solutions that has made it possible is payables finance.

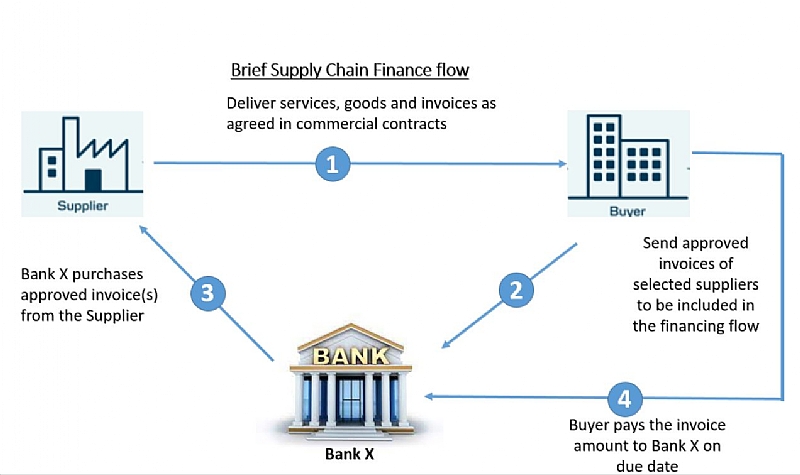

The concept of supply chain finance scheme.

The real challenges faced by the Corporate Treasures and Finance Directors today are that, suppliers who are mostly Small and Medium Enterprises (SMEs) have weak financials and hence unable to source for the needed funding from traditional banks. They are also given some 30, 60 to 90days credit on the back of the goods supplied which eventually ties up their working capital. This is also due to the fact that, there is a receivable and payable cycle challenge which eventually needs to be bridged.

The commercials banks therefore become a factor that act as an intermediary that provide cash or financing to companies by purchasing their accounts receivables . The Financial Institution essentially become a funding source that agrees to pay the company the value of the invoice less a discount for commission and fees. Factoring helps companies to improve their short-term cash needs by selling their receivables in return for an injection of cash from the Banks. The practice is also known as factoring finance, and accounts receivable financing . Basically, it is a supplier financing solution that enables Corporates to offer suppliers the opportunity to receive early payments for the approved invoices.

How does it work?

Most banks who provide these payables finance programmes help suppliers’ access liquidity on the back of their accepted invoices by means of a receivables purchase. These programmes incur less risk as finance is given after the companies have accepted the invoices. In invoice discounting, suppliers are given the option to receive the discounted value of the receivables before the invoice due date. They will typically get access to this liquidity at a more attractive rate than they would otherwise get on their own – due to the higher credit standing of the corporate client.

I have had few interactions with some key suppliers to most companies on the Ghanaian market, and indeed the working capital challenges in today’s highly competitive marketplace can never be underestimated – most of them need funds early in the procurement process. While most banks try to bridge this gap on their standalone basis through payables financing, the high interest rate regime and low appetite by some financial institutions is a major cause of concern to them.

Thankfully, some international banks are leaving up to expectation and supported the factoring process so well. They even offer the services via an end-to-end electric solution to its clients. Offering such a service has helped to bank the entire ecosystem and value chain, thus from the smallest of suppliers to the largest of the multinationals. So this really presents an opportunity for commercial banks who are not offering such solutions to explore and design solutions to meet client’s need?

Typical Supply Chain Finance process flow

Some benefits to Corporate Clients (Buyer)

For a corporate under such discounting programme, you enjoy better pricing in the form of reduced facility fee for the suppliers on the back of their improved access to liquidity. The large number of clients offers the opportunity to a reduced pricing from the bank.

There is also a stable and sustainable supplier base by giving your suppliers access to liquidity when they need it. They will remain loyal and increase your brand promise.

So far as the corporate enrols these suppliers on the scheme, there is a stronger supplier relationship by providing them access to financing at rates they are unlikely to obtain on standalone basis.

The best Supply Chain Financing are usually implemented via electronic banking channels. This ensures greater efficiency as creating a single file will serve as payment instructions for all suppliers included in such programme. Efforts are made to ensure minimal manual processes by seamlessly integrating to in house accounting systems such as SAP, JD Edwards etc and with various connectivity options via a simple file upload process.

Information is very critical and as an Anchor client, you can process transparency with real-time reporting available to your suppliers. For example, some of these corporates could be the likes of Guinness Ghana Limited, Nestle, and Unilever etc.

Some benefits to the Suppliers

Ordinarily, any supply will be obtaining higher interest rates on standalone facilities from a funding bank, however, being part of an invoice discounting programme helps to obtain funding at favourable rates based on the corporate’s creditworthiness.

There is also the opportunity to have the flexibility to receive funds when needed to support business growth. As soon as your invoices are accepted, the factoring bank will pay without delays. The interesting aspect is that the discounted invoice payments can be made irrespective of the supplier domiciled bank.

There is less manual effort as the discounted invoices automatically received are discounted (auto-finance) or so it can be designed online submissions requests for prepayment (selective finance) accepted. Definitely this gives an improved visibility of trade cycle with real-time reports.

The good thing is that, a supplier can select which payment instructions they want financing for. They have the flexibility to; receive prepayment for the full amount automatically and immediately upon acceptance, or selectively at any time until maturity. They also have the flexibility to submit selective prepayment requests for a future date (until maturity) via online channels.

Since this is done online a supplier doesn’t necessarily have to sign up or log in to an online portal before accessing the services.

Recent developments and trends

Some banks are going into partnership with some leading FinTechs specialised in working capital solutions, to transform access to the Bank’s supplier finance programmes, allowing easier enrolment for thousands of suppliers through an online portal while delivering a world-class experience for the Bank’s customers.

The partnership seeks to commence with the roll out of a fully digitised end-to-end supplier enrolment portals. Such portals definitely changes how suppliers are enrolled in supply chain finance programmes by using a digital front-end while providing the Bank’s enrolment team with intuitive dashboards for monitoring and sending updates to anchor companies.

In conclusion, the corona virus pandemic has exacerbated and pushed the need for corporate clients to meet the changing needs of their clients and stay more connected. Commercial Banks are generally liquid and ready to finance the corporates value chain. It is therefore imperative for lenders to rethink the funding approach to deploy working capital within the eco-system.

Every supplier is an engine of growth to the economy and that of the companies they provide services. It is important they come together and take advantage of such innovative financing solutions to ease pressure on cash flows. Corporates must rethink and embed such innovative financing solutions to manage the entire supply chain. The Chartered Institute of Purchasing and Supply and its stakeholders must continue the education, embrace the changes in the world of supply finance and collaborate with corporate organisations to achieve the needed objective.

Thank you for reading.

Disclaimer: The views expressed are personal views and doesn’t represent that of the media house or institution the writer works.

Credit: Michael Sugirin , lawyer, Miriam Amoako, Andrews Adu-Osei.

About the writer

Carl Odame-Gyenti, PhD is a Finance and Investment professional, Country Head (Ag) Client Coverage of an International Bank in Sierra Leone. Contact: [email protected] , Cell: +232 33240467

Site for Adaklu District 24-hour economy market handed over to contractor

Site for Adaklu District 24-hour economy market handed over to contractor

Govt to complete over 1,000MW power expansion in Kumasi — John Jinapor

Govt to complete over 1,000MW power expansion in Kumasi — John Jinapor

Amin Adam made co-chair of Buwumia's Finance and Economy Committee

Amin Adam made co-chair of Buwumia's Finance and Economy Committee

NPP appoints Akosua Manu as spokesperson for gender and social protection commit...

NPP appoints Akosua Manu as spokesperson for gender and social protection commit...

GHS activates national surveillance following hantavirus outbreak on Cape Verde ...

GHS activates national surveillance following hantavirus outbreak on Cape Verde ...

South Africa denies xenophobia claims as Ghana pushes AU action

South Africa denies xenophobia claims as Ghana pushes AU action

Kennedy Agyapong rejects co-chair appointment by Bawumia

Kennedy Agyapong rejects co-chair appointment by Bawumia

Police arrest six suspects over alleged child trafficking syndicate in Kasoa

Police arrest six suspects over alleged child trafficking syndicate in Kasoa

Former Deputy AG urges GJA to resist return to ‘Culture of Silence’

Former Deputy AG urges GJA to resist return to ‘Culture of Silence’

Four killed in Savannah Region road crash involving tipper truck

Four killed in Savannah Region road crash involving tipper truck