The African continent should be concern about the need for a robust Financial Safety Nets(FSNs) in the banking sector, particularly in the current state of fast-changing digitalization and technologies in the face of Artificial Intelligence (AI) and Machine Learning (ML). Available database on Deposit Insurances Schemes (DIS) updated in 2013 shows that the region has not embrace financial safety enough since 2003, and post-financial crisis (2009/2010).

Inasmuch as, some member countries has taken post-crisis (since 2009) steps to safeguard their financial and banking industry with DIS frameworks through the adoption and implementation of Explicit Deposit Insurance Schemes (EDIS) yet still the statutory coverage limit of depositors funds is not sufficient except Libya which has 100% of first LYD10,000, 50% for next LYD90,000, 25% of next LYD300,000, 12.5% of next LYD600,000, and 10% for amounts above LYD1,000,000, up to a maximum of LYD250,000.

I think it’s the high time policy makers reconsiders the debate and take actionable measures with respect to Explicit Deposit Insurance Schemes from regional policy implication perspectives, given the fact that oftentimes bank runs or distress becomes contagious. Countries that has implemented EDIS from 2003 & 2009 so far are: Algeria, Chile, Kenya, Libya, Morocco, Nigeria, Sudan, Tanzania ,Uganda , and Zimbabwe . In 2009, Cameroon, the Central African Republic, Chad, the Republic of Congo, Equatorial Guinea, and Gabon, which shares a regional central bank established the Fonds de Garantie des Dépôts en Afrique Centrale (FOGADAC), a regional deposit insurance scheme that officially became operational in 2011.Thus, 16 out of 55 countries, we need to do more and expand the coverage.

Highlighting key significance of implementing financial safety nets (EDIS),[1] it enhances public confidence by reassuring depositors that their savings are protected, which encourages greater participation in the formal banking system. This is crucial in a region that is more profitable than other regions in the world and at the same time the only region that has not experienced any financial crisis in recent decades but suffers most economically in any global crisis (financial, pandemics) as suggested by Darko.E et al. 2025. [2] Promotes financial stability by mitigating the risk of bank runs during economic distress. Assuring depositors of their funds' security helps stabilize the banking sector, creating an environment conducive to investment and economic growth. Aligning EDIS with global banking standards enhances the reputation of African banks by attracting foreign investment. [3] Can increase the funds available for lending, driving economic development. As African nations pursue greater economic integration, a unified approach to DIS can enhance trust among regional banks and facilitate cross-border transactions especially with the upcoming African Continental Free Trade Area (AfCFTA).

In one of our ongoing scientific paper, we’re exploring the effects of financial safety nets[ Deposit Insurance Schemes (DIS)] on bank profitability in the African banking industry. Our research aims to provide groundbreaking insights into how adopting Explicit Deposit Insurance(EDIS) could enhance bank stability and profitability in the region.

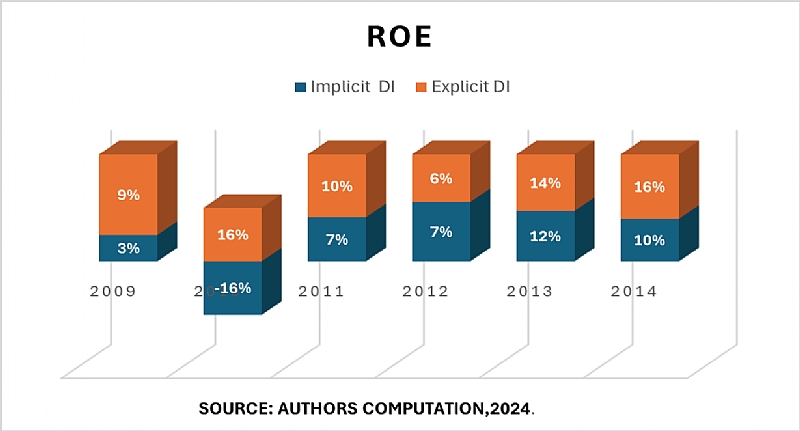

Initial findings indicate a positive correlation between DIS and bank stability , as evidenced by an average return on equity (ROE) analysis between implicit and explicit deposit insurance(DI) systems below.

All things being equal, during the early post-financial crisis in 2009, banks in countries with implicit DI recorded an average ROE of 3%, while those in explicit DI countries averaged 9%. In normal times, such as in 2014, banks with implicit DI averaged 10% ROE compared to 16% for those with explicit DI. These findings emphasize that the potentials of EDIS is not only for stabilizing banks but also could enhance their profitability.

In conclusion, as shown graphically above, EDIS are essential for strengthening the African banking sector, boosting public confidence, ensuring financial stability, and promoting sustainable economic growth across the continent.

Author: Evans DARKO, Doctoral Researcher, CREM Lab, France.

Sources: World Bank Survey, IADI, Laeven and Valencia (2012), FSB (2010, 2012), IMF staff reports, and national deposit insurance agencies.

Woman loses temper, fights mentally challenged lady over alleged disrespect

Woman loses temper, fights mentally challenged lady over alleged disrespect

WHO welcomes UK's move to ban social media access for children under 16

WHO welcomes UK's move to ban social media access for children under 16

June 15: Cedi appreciates, sells at GHS12.30 on forex market, GHS11.06 on BoG in...

June 15: Cedi appreciates, sells at GHS12.30 on forex market, GHS11.06 on BoG in...

Samreboi case: How rejection of Appiah Kubi's withdrawal could offer Wontumi a p...

Samreboi case: How rejection of Appiah Kubi's withdrawal could offer Wontumi a p...

UK to ban under-16s from social media over safety and mental health concerns

UK to ban under-16s from social media over safety and mental health concerns

Samreboi case: Appiah Kubi cites disappointment with court in withdrawal applica...

Samreboi case: Appiah Kubi cites disappointment with court in withdrawal applica...

ECOWAS mourns demise of former Commission President James Victor Gbeho

ECOWAS mourns demise of former Commission President James Victor Gbeho

Andy Appiah Kubi's application to withdraw as Lawyer for Wontumi in Samreboi ill...

Andy Appiah Kubi's application to withdraw as Lawyer for Wontumi in Samreboi ill...

I’ll file a notice of withdrawal and leave the case—Appiah Kubi on next line of ...

I’ll file a notice of withdrawal and leave the case—Appiah Kubi on next line of ...

Don't Compare GHS44.9m to GHS173m: GLOA acknowledges KGL's dominance in revenue ...

Don't Compare GHS44.9m to GHS173m: GLOA acknowledges KGL's dominance in revenue ...