This shift in digital behaviour has compelled banks to satisfy customer expectations by providing online transactional platforms and interactive digital channels, allowing customers to access services and resolve issues without visiting a branch (Deloitte, 2023; KPMG, 2023). Social media has evolved from its early role as a space for simple profile pages and connection services into critical platform for marketing, customer service, and even direct financial transactions. The banking sector in Ghana is leveraging platforms like Facebook, X (formerly Twitter), Instagram, LinkedIn, and WhatsApp to engage customers, promote products, resolve service issues, and enhance brand presence.

Historically, Ghana’s banks relied heavily on branch networks, traditional advertising, and face-to-face relationship management to attract and retain customers. However, shifts in customer behaviour, coupled with the impact of the COVID-19 pandemic in accelerating digital adoption, have pushed the industry toward online engagement. Customers now expect near-instant responses to inquiries, personalised communication, and the ability to resolve issues without visiting a branch. Social media platforms particularly Facebook, X , Instagram, LinkedIn, and WhatsApp have become central to meeting customer expectations.

Globally, the technological trends are similar to the Ghanaian situation. Financial institutions in markets such as Nigeria, South Africa, UK, and the United States of America are using social media to drive product awareness, deliver customer service, and monitor brand sentiment in real time. In Ghana, this shift is being driven by regulatory frameworks such as the Data Protection Act, 2012 (Act 843) and the Cybersecurity Act, 2020 (Act 1038), where both influence how banks collect, store, and process data from social interactions.

The current happenings particularly in the banking sector, is a critical wakening to banks to embrace contemporary banking practices through social media platforms. Hence this article examines the role of social media in Ghana’s banking industry through three lenses – social media on banking operations and customer engagement, social media on bank growth and efficiency, and the challenges including reputational, cybersecurity, and compliance risks that banks must navigate. Using recent industry data, examples from Ghanaian banks, and lessons from other markets, the analysis provides insights into how financial institutions can strategically leverage social media while safeguarding trust and operational integrity.

Impact of Social Media on Banking in Ghana

Social media’s influence on Ghana’s banking sector is multi-dimensional, touching on marketing, customer engagement, product innovation, and brand perception. The shift is not merely cosmetic; it is structural, redefining how banks connect with and serve their customers.

Social Media Penetration and Usage Trends in Ghana

Recent data shows that social media penetration in Ghana continues to expand rapidly, providing banks with a large and growing audience. According to DataReportal (2025), Ghana had 8.4 million active social media users in January 2025, representing 25.1% of the total population. Mobile connectivity is driving this growth, with 43.2 million mobile connections in the country (about 129% SIM penetration), indicating that many individuals own more than one SIM card.

The most widely used platforms are:

- WhatsApp – used by 94.9% of internet users aged 16–64

- Facebook – 81.8%

- Instagram – 70.6%

- TikTok – 65.2%

- LinkedIn – 18.4%

(Source: DataReportal, 2025)

From a device perspective, StatCounter (July 2025) reports that mobile devices account for 74.3% of all web traffic in Ghana, followed by desktops (24.5%) and tablets (1.2%). This confirms that any bank seeking digital engagement must optimise for mobile-first interactions. This implies that high mobile and social media penetration creates a strategic opportunity for banks to deliver services, market products, and engage customers through channels they already use daily.

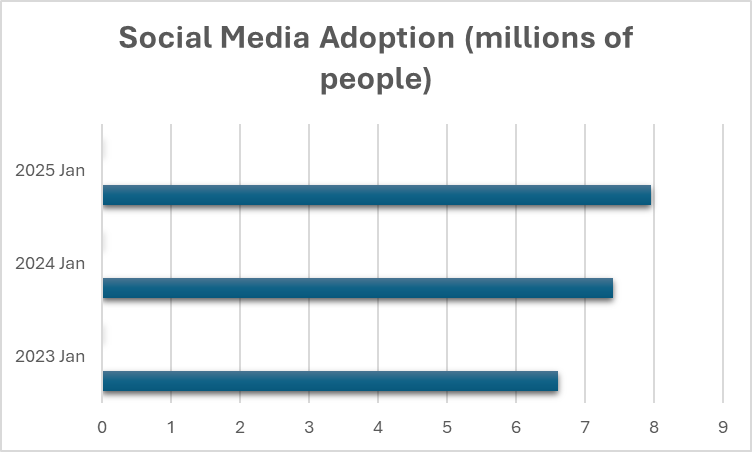

Moreover, the growth in active social media users in Ghana has been remarkable in recent years. As shown in Figure 1, adoption trends from January 2023 to January 2025 reveal a steady and consistent expansion of the country’s digital audience. This growth signals an ever-widening opportunity for banks to connect with customers where they already spend much of their time on social platforms.

Figure 1: Growth in Active Social Media Users in Ghana, January 2023–January 2025

Source: DataReportal (January 2023, January 2024, January 2025)

Source: DataReportal (January 2023, January 2024, January 2025)

Figure 1 illustrates the steady growth in the number of active social media users in Ghana over the past three years. In January 2023, there were approximately 6.6 million active users. This increased to 7.4 million in January 2024, representing a 12.1% year-on-year growth. By January 2025, the figure reached 7.95 million, a further 7.4% increase from the previous year.

Overall, Ghana recorded a cumulative increase of about 20.5% in active social media users between 2023 and 2025. This sustained growth reflects the country’s expanding internet penetration and increasing mobile connectivity. For banks, this trend signals a continually enlarging digital audience, providing opportunities to scale up online marketing, customer engagement, and mobile-based service delivery.

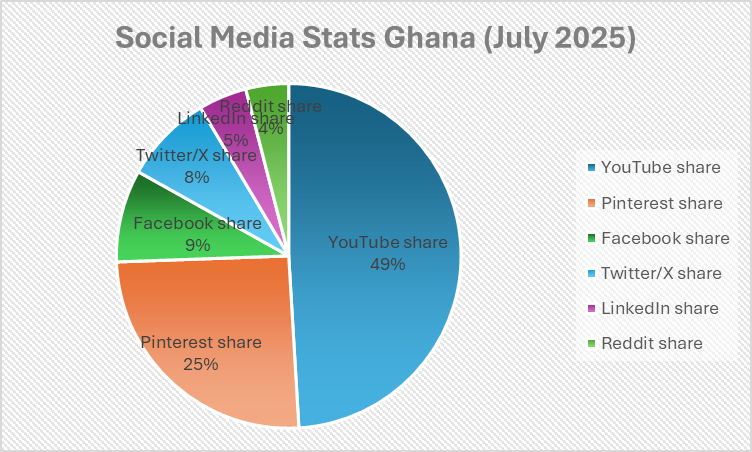

Further, understanding which platforms dominate usage is essential for shaping effective social media strategies. Figure 2 presents the share of social media platforms in Ghana as of July 2025, illustrating the clear dominance of YouTube and the continued strength of visual and video-driven engagement across audiences.

Figure 2: Share of Social Media Platforms in Ghana, July 2025

source: StatCounter July 2025

source: StatCounter July 2025

Figure 2 shows the distribution of social media platform usage in Ghana as of July 2025. YouTube holds the largest share of activity at 47.45%, highlighting the strong appetite for video-based content among Ghanaian internet users. Pinterest ranks second with 24.55%, indicating a notable interest in visual discovery and content curation platforms.

Facebook and X (formerly Twitter) maintain moderate shares of 8.39% and 8.06%, respectively, serving as important channels for community engagement, news, and customer interaction. LinkedIn (4.39%) plays a smaller but strategic role, particularly for professional networking and B2B engagement, while Reddit (3.88%) caters to niche communities and interest-based discussions.

For banks, these statistics emphasise the value of prioritising video and visual content in digital marketing strategies, while also leveraging Facebook and X (formerly Twitter) for ongoing engagement, and LinkedIn for targeting professional segments.

Marketing and Brand Awareness

Social media has emerged as a primary marketing channel for banks in Ghana, complementing traditional advertising such as TV, radio, and billboards. Platforms like Facebook and Instagram allow banks to target campaigns at specific demographics based on age, location, income, and interests. For example, Absa Bank Ghana’s “My Moments” campaign used Instagram storytelling and influencer partnerships to promote its personal loan offerings, attracting high engagement from young professionals.

Statistics underscore the scale of this impact. In 2024, Facebook accounted for 55.4% of social media traffic in Ghana, followed by X (formerly Twitter) (18.3%) and Instagram (12.5%) (StatCounter, 2024). These platforms offer cost-effective reach; compared to TV or print media, the cost per impression on social media can be as low as 10% of traditional channels, enabling banks to stretch marketing budgets while maintaining visibility.

Customer Service Transformation

Banks have transitioned from viewing social media as a broadcast tool to recognising it as a frontline customer service channel. Leading institutions such as Stanbic Bank Ghana and Ecobank Ghana operate active customer care handles on X (formerly Twitter), responding to queries, complaints, and service requests in real time.

A 2024 survey by PwC Ghana found that 67% of banking customers aged 18–35 preferred using social media or instant messaging apps to reach customer service rather than calling or visiting a branch. This shift is not only improving customer satisfaction but also reducing operational costs associated with branch traffic and call centre volumes.

Product Development and Innovation

Social media feedback provides banks with valuable insights for product development. By monitoring customer discussions, banks can identify pain points, unmet needs, and emerging trends. For instance, persistent online discussions about high remittance charges prompted several banks to launch reduced-fee remittance products in partnership with fintech companies in 2023 and 2024.

Moreover, social media polls and feedback campaigns such as Fidelity Bank Ghana’s online customer suggestion forum have accelerated the development cycle for new products.

Reputation and Crisis Management

The speed and reach of social media can amplify both positive and negative narratives. While customer praise can enhance a bank’s reputation instantly, complaints can spread quickly, risking reputational damage if not addressed promptly.

A notable example occurred in early 2024, when a service outage at a major Ghanaian bank trended on X (formerly Twitter) under the hashtag #BankFailGH. Although the bank resolved the technical issue within hours, the reputational fallout persisted for weeks due to slow initial communication. This incident underscored the importance of proactive, transparent, and empathetic crisis management strategies.

Opportunities for the Banking Sector

Beyond its impact on day-to-day banking operations, social media also opens new pathways for inclusion, market insight, and revenue growth. While it introduces certain risks, its strategic adoption can deliver significant gains for Ghana’s banking sector.

Expanding Financial Inclusion

Social media offers banks a cost-effective way to reach unbanked and underbanked populations, particularly in rural and peri-urban areas where traditional branch infrastructure is limited. According to the World Bank Global Findex Database (2023), about 32% of Ghanaian adults remain unbanked. Mobile-friendly campaigns on Facebook and WhatsApp can educate these groups about banking products, digital payment solutions, and savings options.

For example, GCB Bank’s financial literacy series on Facebook Live has successfully reached thousands of first-time account holders in less than a year, using interactive Q&A sessions to build trust and awareness.

Cost-Effective Market Research

The interactive nature of social media enables banks to gather customer feedback rapidly, often in real time, without the expense of large-scale surveys. Polls, hashtags, and comment threads serve as instant focus groups, providing insights into customer sentiment, satisfaction, and demand for new services.

This method is particularly relevant given Ghana’s high mobile penetration with mobile internet penetration standing at 68.1% in January 2024 (DataReportal, 2024). Banks can harness this connectivity to engage customers continuously and adjust strategies promptly.

Strengthening Brand Loyalty Through Engagement

Unlike traditional advertising, which is largely one-way communication, social media allows for sustained, two-way dialogue between banks and customers. Consistent engagement through personalised messages, recognition of customer milestones, or showcasing customer success stories — builds emotional connections that can translate into brand loyalty.

For instance, Absa Bank Ghana’s #AbsaInYourCorner campaign celebrated small business clients on Instagram, boosting client retention rates and generating significant positive sentiment online.

Cross-Selling and Upselling Opportunities

Social media algorithms allow banks to target existing customers with tailored offers based on their digital interactions. A customer engaging with mortgage-related content, for instance, can be served ads for home insurance, property investment webinars, or renovation loan products.

This data-driven targeting is proving effective: a 2024 Accenture Ghana report found that targeted social media ads in the banking sector generated conversion rates up to 40% higher than generic online ads.

Challenges and Risks

While social media presents vast opportunities for Ghana’s banking sector, it also brings significant risks that require careful management. A bank’s ability to harness the benefits often depends on how well it anticipates, mitigates, and responds to these challenges.

Cybersecurity Threats and Fraud

Social media platforms have become fertile ground for phishing scams, fake promotions, and identity theft. Fraudsters often impersonate reputable banks, luring customers into revealing sensitive information. According to the Bank of Ghana’s Fraud Reports, cyber and technology-related fraud losses rose from GH¢5.4 million in 2022 to GH¢8.9 million in 2023, before edging further to just under GH¢10 million in 2024 (Bank of Ghana, 2023; 2024; 2025).

The upward trend highlights the growing sophistication of fraudsters, many of whom exploit social media as a convenient channel for impersonation and misinformation. The reputational damage from such incidents can be severe, particularly when false information spreads rapidly before official clarifications are issued.

Misinformation and Brand Reputation Risks

In the age of instant sharing, false or misleading content about a bank can go viral within minutes. A minor service disruption, if misrepresented on social media, can trigger panic withdrawals or loss of public confidence.

For example, in early 2024, a Ghanaian bank faced a brief liquidity rumour on X (formerly Twitter), which trended nationwide despite being false. The bank’s delayed response led to increased customer queries and a temporary dip in share price.

Regulatory and Compliance Challenges

Banks operating on social media must comply with both banking regulations and data protection laws. Ghana’s Data Protection Act, 2012 (Act 843) imposes strict requirements on how customer information can be collected, stored, and shared online.

Additionally, advertising on social media must adhere to the Bank of Ghana’s Market Conduct Rules, which prohibit misleading claims about products and services. Violations can attract penalties and reputational harm.

Managing Customer Expectations

Social media has conditioned customers to expect instant responses. Delayed replies to complaints or inquiries especially when the customer can see that the message has been “read” can negatively impact brand perception.

According to Hootsuite’s 2024 Social Customer Service Benchmark Report, 78% of Ghanaian banking customers expect responses within one hour of sending a query on social media. Meeting these expectations requires trained teams and clear escalation procedures.

Resource and Skills Gaps

Some banks struggle to maintain a consistent, strategic presence online due to limited budgets, inadequate in-house expertise, or over-reliance on third-party agencies. This can lead to fragmented communication, inconsistent branding, or missed engagement opportunities.

Recommendations

The integration of social media into Ghana’s banking ecosystem offers transformative potential, but it also demands deliberate strategy, robust governance, and continuous adaptation. The following recommendations are proposed for banks, regulators, and industry stakeholders to maximise benefits while mitigating risks:

Develop a Comprehensive Social Media Strategy

Banks should create formal, board-approved social media strategies that define objectives, target audiences, key platforms, and performance metrics. This strategy must align with the bank’s overall business goals and risk appetite, ensuring a coherent approach across marketing, customer service, and brand management.

Strengthen Cybersecurity and Fraud Prevention Measures

Given the rise in social media-related fraud, banks must integrate cybersecurity protocols into their social media operations. Measures should include:

- Verified “blue tick” accounts to enhance authenticity

- Real-time monitoring for fraudulent content

- Multi-channel customer alerts about scams

- Mandatory staff training on phishing and impersonation risks

Enhance Real-Time Customer Engagement Capabilities

To meet growing expectations for fast responses, banks should:

- Deploy dedicated social media service teams with authority to resolve issues promptly

- Use AI-powered chatbots for first-line responses during peak periods

- Implement escalation protocols to ensure complaints are addressed within agreed service-level timelines

Build Staff Capacity and Digital Skills

Continuous training in digital marketing, online reputation management, and compliance is essential. Partnerships with training institutions such as the National Banking College can equip bank staff with the latest social media and customer engagement competencies.

Establish Robust Crisis Communication Frameworks

Banks should have pre-approved crisis communication playbooks for social media, covering:

- Early detection and verification of emerging issues

- Rapid, transparent public responses

- Coordinated messaging across all platforms to prevent misinformation spread

Use Social Media for Financial Literacy and Inclusion

Banks can leverage platforms like Facebook Live, WhatsApp groups, and YouTube to deliver financial literacy programmes targeting unbanked and underbanked populations. This strengthens public trust, supports regulatory inclusion goals, and creates new customer pipelines.

Strengthen Regulatory Collaboration

The Bank of Ghana, Data Protection Commission, and the Cyber Security Authority should work with industry players to develop sector-specific guidelines for social media use in banking. This could include model policies, compliance checklists, and best practice frameworks.

Conclusion

Social media is no longer a peripheral communication tool for Ghana’s banking sector; it is now a core channel for customer engagement, marketing, and service delivery. Its influence extends beyond brand visibility to shaping customer perceptions, driving product innovation, and expanding financial inclusion.

However, the same platforms that offer growth opportunities also present significant risks from cyber fraud and misinformation to regulatory non-compliance and reputational damage. The ability of banks to thrive in the social media age will depend on how effectively they integrate robust strategies, build in-house capacity, invest in real-time engagement, and collaborate with regulators to establish clear governance frameworks.

By adopting proactive, data-driven, and customer-centric approaches, Ghanaian banks can leverage social media not only as a marketing and service tool but as a core pillar of strategy, trust-building, and competitive advantage. Those that embed social media deeply into their operations will lead the sector’s digital transformation, forge stronger relationships, and sustain customer loyalty in an increasingly connected economy.

References

- Bank of Ghana. (2024). FinTech sector report 2024 (full year). Accra: Bank of Ghana.

- Datareportal. (2024). Digital 2024: Ghana. Retrieved from https://datareportal.com/reports/digital-2024-ghana

- Deloitte. (2023). Digital banking in Africa: Strategic priorities for banks. Johannesburg: Deloitte Africa.

- KPMG. (2023). Ghana banking industry customer experience survey. Accra: KPMG Ghana.

- PwC. (2022). Social media risk management in financial services. Retrieved from https://www.pwc.com

- StatCounter. (2025, July). Social media market share in Ghana. Retrieved from https://gs.statcounter.com

- Statista. (2024). Social media usage in Ghana – Statistics & facts. Retrieved from https://www.statista.com

- World Bank. (2023). Digital economy diagnostic: Ghana. Washington, DC: World Bank.

Justin Kodua Launches Bid to Retain NPP General Secretary Post Ahead of Crucial ...

Justin Kodua Launches Bid to Retain NPP General Secretary Post Ahead of Crucial ...

Zanetor Demands Continental Action: ‘Africa Cannot Progress While Women Live in ...

Zanetor Demands Continental Action: ‘Africa Cannot Progress While Women Live in ...

Mahama assures transfer of UGMC to University of Ghana

Mahama assures transfer of UGMC to University of Ghana

Wontumi told me he would get 20year jail term before judgment was read – Lawyer ...

Wontumi told me he would get 20year jail term before judgment was read – Lawyer ...

Sarkodie Warns Gov’t: ‘Explain the 24-Hour Economy or Risk Voter Backlash’

Sarkodie Warns Gov’t: ‘Explain the 24-Hour Economy or Risk Voter Backlash’

‘Ofori-Atta Must Account’: COPEC Boss Warns NPP of 2028 Backlash Over Lingering ...

‘Ofori-Atta Must Account’: COPEC Boss Warns NPP of 2028 Backlash Over Lingering ...

UG Economist Slams Gov’t: “24-Hour Economy Implementation Far From Reality”

UG Economist Slams Gov’t: “24-Hour Economy Implementation Far From Reality”

Ghana Flags 1.8m Housing Gap at UN Forum, Says Urban Pressures Demand Urgent Act...

Ghana Flags 1.8m Housing Gap at UN Forum, Says Urban Pressures Demand Urgent Act...

NDC Draws Red Line: Gov’t Appointees Who Don’t Resign Barred from Executive Elec...

NDC Draws Red Line: Gov’t Appointees Who Don’t Resign Barred from Executive Elec...

Kpebu Warns: “Judicial Independence Won’t Come From Law Alone — It Needs Judges ...

Kpebu Warns: “Judicial Independence Won’t Come From Law Alone — It Needs Judges ...