OVERARCHING POLICY QUESTIONS

- This new formula is clearly a policy direction towards direct control as opposed to market-based indirect control in the spirit of market liberalization. Is this the policy intent of the Central Bank?

- Is the new BOG formula applicable to only Deposit Money Banks?

- Would Return on Equity (ROE) be used on projected or historical basis?

The issue of financing cost, according to many research reports including the current Business Barometer Survey 2013 by Association of Ghana industry (AGI), is on the front burner as far as business challenges in Africa and particularly Ghana is concerned. The history of monetary policy development in Ghana since independence shows a rough path with many phases in between the extremes of direct official control to full liberalization in 1992. Prior to the introduction of World Bank's sponsored Economic Recovery Program (ERP) in 1983 the objective and direction as far as monitory policy was concerned, was to ensure that the financial markets were aligned with the government's economic objectives. Credit was allocated to certain sectors with little regard for sector risk as the primary basis of resource allocation. Foreign exchange was rationed on the basis of certain criteria which was at best subject to the changing whims of bureaucrats and politicians. Suffice to say, ultimately, the end result was the country's inability to realize its policy objective thus creating an inefficient and dysfunctional resource allocation mechanism. Many years passed whilst new arguments emerged to support a policy of market liberalization mediated by strong institutional regulation. That argument clearly contrasted the inefficiencies of official control with the proposed benefits of markets as a more efficient allocator of resource for developmental purposes. It seemed apparent, that the hope and expectation of interest rates, exchange rates and other asset prices that formed a key component of enterprise cost structure would trend downward to levels that would make Ghanaian enterprises competitive, both regionally and globally.

In 2013, private businesses, the government and indeed the financial sector regulator, continue to grapple with high interest rate amidst other business challenges that threatens to undermine GDP growth projections for the current fiscal year. It is important to acknowledge however, the tremendous improvement in Deposit Money Bank's credit allocation to the private sector in recent years notwithstanding the notoriously burgeoning Public Sector Borrowing Requirement (PSBR) over the years as a result of poor fiscal management.

POLICY ISSUES

Freedom Centre strongly believes, the recent announcement by the Bank of Ghana concerning a new formula to be used by Banks as a guide for loan asset pricing, is a commendable policy attempt to address a seemingly intractable economic problem. However, there are major concerns and issues as far as expected policy impact is concerned. The following issues equires clarity to enable build confidence in the current supervisory approach of BOG:

First, the lack of transparency and the scantiness of details regarding policy implementation exacerbates this public concern that such a commendable measure may only be exercise in appearance.

* Secondly, this new formula is clearly a policy direction towards price control as opposed to market intervention. As the case was, prior to the introduction of Economic Recovery Program in 1983 and Structural Adjustment Program in 1986, unintended consequences of central direct control created unpleasant gaps between policy aims and outcomes. Direct control in those era involved the imposition of ceilings, both global and sectoral, on individual commercial banks' lending. The policy objective was to achieve consistency with national macroeconomic targets such as growth, inflation and external balance. It's a matter of public record that time proved these mechanisms to be ineffective and inefficient in realizing the policy goals as originally intended.

To help address these concerns it's imperative that BOG take steps to build public confidence especially at the backdrop of skepticism expressed by certain financial sector bigwigs. We believe that BOG should clarify the HOW of this policy initiative and what institutional compliance would look like. Providing regular updates and impact assessment reports to enable Civil Society Organizations (CSOs) and interest groups provide an independent opinion on policy effectiveness or otherwise would also help build momentum for implementation.

ANALYZING RELATIONSHIPS

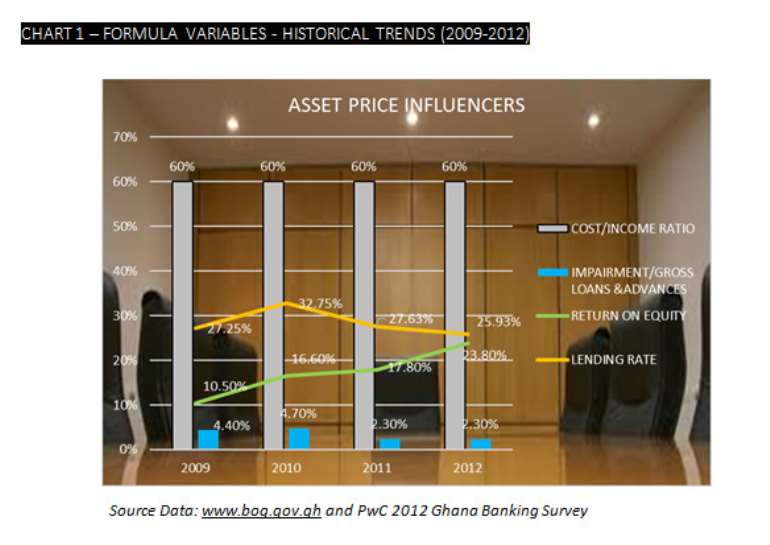

With declining impairment charge to gross loans and advances, it is clear that the industry has improve tremendously in credit risk management, particularly at the origination side where credit reference bureau hits has gone up according to official data. As at end-December 2011, all Deposit Money Banks (DMBs) had signed up for credit reference services and were sharing data, while twenty-seven NBFIs submitted data to the bureau. (Source: www.bog.gov.gh)

Notwithstanding year-on-year decline in average industry lending rate from 2010, high cost/income ratio still poses tremendous upward price pressure. There is no question that better cost management would have wider benefits for not just shareholders but for key stakeholders in the economy.

THE MISSING VARIABLE

The financial sector has inextricable linkage and interactivity with public sector fiscal management in a manner that affects both volume and price in the money market. Thus budget deficits creating bigger PSBR with its attendant crowding out effect on the markets, no doubts influences funding cost. It stands to reason therefore, that any formula which does not explicitly account for this public sector variable, creates doubt regarding its usefulness as an effective control mechanism for addressing asset price volatility.

QUESTIONS FOR BOG

Given these concerns, it is imperative for BOG to reassure all stakeholders especially the AGI, that this policy initiative would serve the general good by helping manage lending.

Specifically, BOG must answer the following questions in order to dispel doubts regarding policy viability:

1. Is the formula applicable to only Deposit Money Banks?

2. What is the expected impact of each variable on asset price?

3. Would each variable carry same/different weight and how much?

4. Would Return on Equity (ROE) be used on projected or historical basis?

These are important questions that we believe when answered, would enhance public understanding and would create parallel pressure points on the money markets to respond to private sector demands for more competitive pricing.

Nkunimdini Asante-Antwi

VP, Markets and Policy Research

233 (202) 952658

233 (242) 564143

[email protected]

Kindly send comments and feedback to [email protected] or visit www.freedomcentreghana.com for other papers.

GJA Applauds Ghana’s Sharp Rise in Global Press Freedom Rankings

GJA Applauds Ghana’s Sharp Rise in Global Press Freedom Rankings

US Embassy Cautions Against Censorship in Fight Against Misinformation

US Embassy Cautions Against Censorship in Fight Against Misinformation

Interior Minister Blames Weak Enforcement by Assemblies After Avenor Building Co...

Interior Minister Blames Weak Enforcement by Assemblies After Avenor Building Co...

Gov’t Warns Against Rising Misinformation, Calls for Stronger Journalistic Stand...

Gov’t Warns Against Rising Misinformation, Calls for Stronger Journalistic Stand...

Ramaphosa Warns Against Vigilante Crackdowns on Foreign Nationals

Ramaphosa Warns Against Vigilante Crackdowns on Foreign Nationals

Global InfoAnalytics Boss Rejects Claims Polls Are Destabilising NDC

Global InfoAnalytics Boss Rejects Claims Polls Are Destabilising NDC

Bawumia to Propose Policy Alternative as Cocoa Sector Tensions Deepen

Bawumia to Propose Policy Alternative as Cocoa Sector Tensions Deepen

ECG Announces Scheduled Outages and Technical Fault Affecting Multiple Regions o...

ECG Announces Scheduled Outages and Technical Fault Affecting Multiple Regions o...

Investigation committee uncover GH¢19.5m loss at Bolgatanga Technical University...

Investigation committee uncover GH¢19.5m loss at Bolgatanga Technical University...

Afenyo-Markin calls for protection of journalists, warns against suppression of ...

Afenyo-Markin calls for protection of journalists, warns against suppression of ...