Access to decent and adequate housing is often considered a basic human right. The World Bank Group estimates that by 2030, three billion people, or 40 percent of the world’s population will need new housing units. In Ghana, low-income households face difficulties in accessing not only affordable housing solutions but also housing of good quality. The informal and formal sector supply of housing continues to be inadequate to meet the increasing demand. This has resulted in acute and persistent housing deficits — a situation that presents a complex mix of both challenges and opportunities. This article with the help of the findings by the iBAN Housing Reports and Sikadan Homes sets out the major issues affecting affordable housing provision and seeks to unfold a business case for both government and private sector interventions in affordable housing in the country.

Since 2010, Ghana has been tagged as experiencing a housing deficit of 1.7 million units. However, present trends show that the probable increase in deficit may not be because of an increase in population but due to the inability of citizens to afford houses. About 1.5 million low-income households need affordable housing solutions in Ghana with about 12.4 Million Ghanaians living in slums(UN-HABITAT).

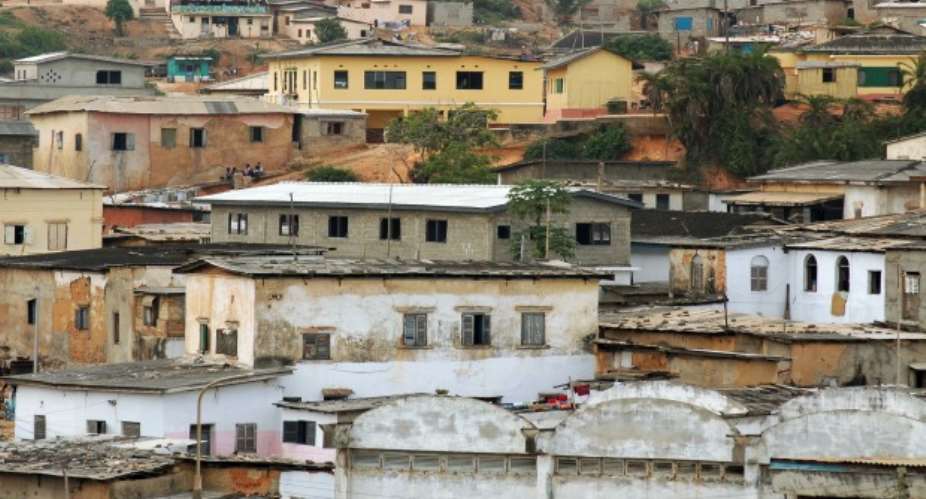

Ghana’s real estate market is largely based on informal sector activities to supply and allocate housing units. The housing market currently appears to be experiencing significant investment and growth, arising from the country’s economic growth, oil discovery and exploration, and remittances. Consequently, the Housing supply has undoubtedly enjoyed positive growth rates over the years.

However, this level of production only addresses about 35% of the annual demand for new housing (UN-HABITAT 2008). Given that the recent boom in the real estate market distinctly favors high-income households, which constitute only 5% of the population, this deficit appears to mainly affect the larger part of the housing market that is persistently overlooked by market supply forces and/ or developers.

According to the iBAN Ghana Housing report, a limited survey of selected stakeholders was carried out to explore what constitutes ‘affordable’ housing. For private developers, affordability is both a function of the quality of the building fabric and the price relative to the income of a target group. For financiers, it is linked to a certain, arbitrarily-set price point related to the cost of housing. For low-income households, it is determined by price, build quality, and location. These different perspectives suggest that affordability means different things to different people. Affordability is thus seen differently by different stakeholders depending on their function along the housing value chain.

But should this be the case if we really want to anchor our housing market with a uniform structured standard of quality and pricing model?

According to Sikadan Homes www.sikadanhomes.org , the best way to assess the challenges in the housing market is to analyze them from two perspectives; the rental and homeownership perspectives:

The HomeOwnership Perspective

According to the iBAN Ghana Housing 2016 Report, Housing sold on the formal real estate market is beyond the financial means of most households, with only about 1% of households able to afford the cheapest houses offered by formal developers. For example, in 2015 the cheapest house cost USD 24,297. After paying the 20% deposit, the mortgagee is required to make a monthly payment of USD 245 over a 20-year period and must have a monthly income of USD 612 to qualify. Meanwhile, the monthly income of households averages USD 347.

Bank lending rates are standing at around 30% per annum and thus housing finance is out of reach of virtually all but those on high incomes households. For example, average household incomes reported in 2014 stood at GHS 16,644 (GSS 2014). Using the housing cost-to-income metric, households able to spend three times their annual incomes would be able to afford accommodation worth USD 14,000.

The Rental Perspective

Conversely, 99% of the remaining households that couldn't afford the cheapest houses offered, per the iBAN Report therein, end up on the house rental market. These categories are surely within the low-income bracket with most of them renting every year whiles the remaining people find themselves occupying relatives' rooms for free. This is the true state of the Ghanain house rental market as it stands now. When the annual carrying cost of a home exceeds thirty percent (30%) of household income, then it is considered unaffordable for that household.

According to Sikadan homes, the following are the barriers or market challenges that make house rental more unaffordable for the low-income households in Ghana ;

- Burdensome Rent Advance

In Ghana, Landlords do not accept monthly payments for rent; tenants have no option but to raise funds to pay their year advance rent

- High Bank Interest Rate

Due to high rent advances, most tenants pre-finance their home rental with bank loans. Unfortunately, bank interest rates are a bit high

making their rent more expensive and unaffordable. For Example, if Kofi is to pre-finance his rent using a loan at 2.5% per month, it means Kofi is going to increase his rent amount by 30% by the end of the year simply because of the interest rate of the loan he took.

- High Valuation of Rooms: There's no standard rent pricing hence overpricing or unguided setting of rent value by the Landlords. An average decent single room in a good location in Ghana will cost you not less than $80 per month

Proposed Solution

I will share that in the next episode of this article, the Rent Crisis II

By

JUSTICE OFFEI JR.

Ghana Medical Trust Fund briefs Otumfuo on progress, vision for expanding specia...

Ghana Medical Trust Fund briefs Otumfuo on progress, vision for expanding specia...

KGL partners Ghana Medical Trust Fund to build ultra-modern diagnostic centre at...

KGL partners Ghana Medical Trust Fund to build ultra-modern diagnostic centre at...

Finance Ministry tables six bills in Parliament to tighten revenue collection, r...

Finance Ministry tables six bills in Parliament to tighten revenue collection, r...

Second batch of Ghanaians evacuated from South Africa expected home today

Second batch of Ghanaians evacuated from South Africa expected home today

Indian education minister resigns after mass protests over exam paper leaks

Indian education minister resigns after mass protests over exam paper leaks

Gbese Court Orders Extradition Of Alleged Abu Trica Accomplice To U.S. In $8m Ro...

Gbese Court Orders Extradition Of Alleged Abu Trica Accomplice To U.S. In $8m Ro...

Gov’t Taskforce Storms Accra With Demolitions, Dredging In Massive Anti‑Flood Bl...

Gov’t Taskforce Storms Accra With Demolitions, Dredging In Massive Anti‑Flood Bl...

Wontumi Sentence A “Turning Point” In Galamsey Fight — UESD Lecturer Says Financ...

Wontumi Sentence A “Turning Point” In Galamsey Fight — UESD Lecturer Says Financ...

Health Minister Updates Asantehene On Sweeping Reforms: “No Ghanaian Should Be D...

Health Minister Updates Asantehene On Sweeping Reforms: “No Ghanaian Should Be D...

Afenyo‑Markin Explodes In Parliament: “Mahama’s Mid‑Year Budget Is A Third‑Term ...

Afenyo‑Markin Explodes In Parliament: “Mahama’s Mid‑Year Budget Is A Third‑Term ...