Access to quality financial services is essential to inclusive economic growth and poverty alleviation. In the last decade, the African continent has recorded significant growth in financial inclusion. The progress in financial inclusion is spearheaded by innovations in digital technology, which is transforming financial services and the nature of financial transactions in the region.

This current change in the financial sector is enhancing access to financial services for the underserved and the unbanked population, which is reducing gender and income inequality. Financial inclusion in Africa almost doubled in 2017 when compared to 2011 (23% of the population had bank accounts or mobile money accounts), as 43% of adults had accounts at the bank or with mobile money service providers.

The growth in financial inclusion is largely attributed to mobile money adoption. Mobile money services in Africa have become indispensable, particularly in lifting women from poverty. Boosting women’s financial inclusion is vital to economic growth and poverty alleviation in Africa, where women experience a disproportionate level of poverty as a result of limited access to economic resources.

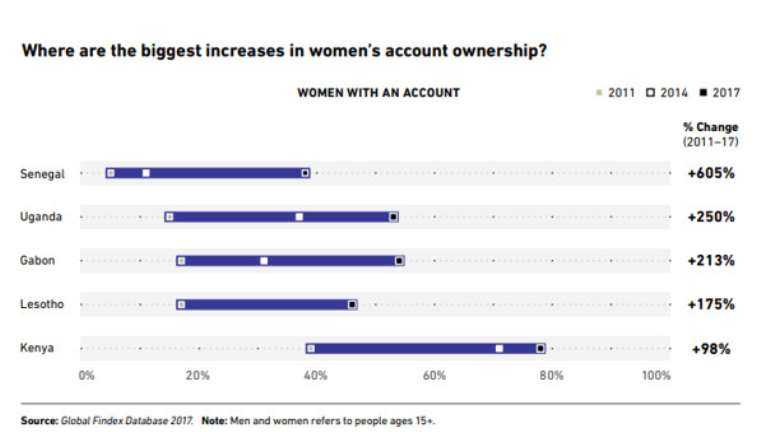

For instance in Côte d'Ivoire, where the gender gap for access to financial institutions increased by 90% between 2014 and 2017, the gender gap in mobile money dropped by 35% within the same period. Women’s financial inclusion in Africa has improved significantly in recent times. Between 2011 and 2017, the share of women with bank accounts or mobile money accounts increased significantly among African countries. Within this duration, women with bank accounts have increased by seven-fold in Senegal and double in Ghana and Kenya. Other African countries such as Uganda, Lesotho, and Gabon also recorded remarkable growth in financial inclusion.

As the epicentre of mobile money services, account ownership among adults in sub-Saharan Africa (SSA), continues to soar mainly as a result of enhanced access to mobile money services. According to the Global Findex database, in 2017, about 43% of adults in SSA had accounts at the bank or with a mobile money service provider - up from 34% in 2014.

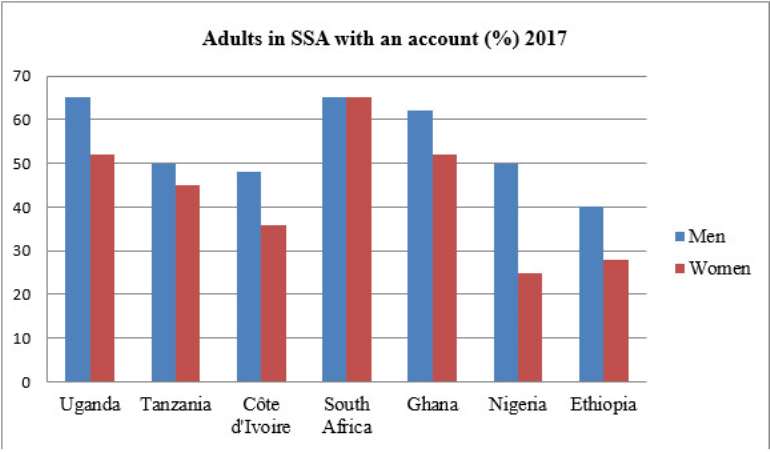

Although the proportion of adults with an account at a financial institution in SSA increased by 4 percentage points from 2014 to 2017, the share of adults with mobile money accounts was almost double, thus from 12% to 21%. With a gender gap of 11% in SSA, men represent the largest percentage of account ownership, thus 48% of men have accounts and 37% of women also own accounts at a bank or a mobile money service provider. The size of this gender gap varies across different countries in SSA.

For example in South Africa, women and men are equally likely to own an account at a bank or mobile money account. This is not the same situation in most countries in SSA. With significant gender gaps in countries such as Ethiopia, Mozambique, Uganda, and Côte d'Ivoire, men in Nigeria are twice as likely as women to own accounts.

In North Africa, progress in financial inclusion has been relatively slow, as two-thirds of the adult population in the region are unbanked and the gender gap for access to financial services is 18%, the largest in the world.

Africa has a high incidence of poverty, in spite of the fact that extreme poverty declined from 54% in 1990 to 41% in 2015, a large percentage of the population are living in poverty - currently, more Africans are living in poverty than in 1990. The population living in poverty increased from 278 million in 1990 to 413 million in 2015 with 82% of the poor population living in rural areas.

High level of poverty among countries in Africa makes women’s economic empowerment a daunting task. However recent studies have shown that providing low-income women with the appropriate financial services that enable them to access credit, save part of their income, conduct business transactions and manage risks is pertinent for women’s economic empowerment.

Furthermore, improving access to secure savings accounts for women could stimulate economic resilience and increase control over financial resources for women in Africa. This improves the household decision-making power of women which ultimately leads to a better outcome for children, household nutrition, and the community as a whole. Despite the importance of financial inclusion in women’s economic empowerment, women in Africa are disproportionately excluded from formal financial services.

Complex cultural, economic, social, and legal barriers continue to retard growth in financial inclusion for women in African countries. For instance, in Gabon Cameroon, Chad and Niger there are regulations that deter women from opening bank accounts in the same way as men.

To ensure that women are adequately empowered through financial inclusion, Governments in Africa together with relevant stakeholders should reform and enforce regulations on asset ownership. For most African countries, asset ownership is a constraint to women’s access to credit and other financial services as women usually do not have complete ownership to assets such as land that could serve as collateral when seeking financial assistance.

Again, policymakers in Africa should implement evidence-based policies that have the potential to accelerate women’s financial inclusion. With the largest percentage of Africa’s poor population living in rural areas, it will be a step in the right direction for governments and development organizations to provide customized programs that focus on improving the quality of education and access to financial information for women living in rural areas. Financial institutions can also provide tailor-made financial services for women living in rural areas.

Lastly, for Africa to achieve an effective regulatory framework for gender-sensitive financial inclusion that could enhance the economic empowerment of women in the region, it is imperative for development partners and relevant stakeholders to invest adequately in financial infrastructure. Appropriate investment in financial infrastructure will foster interoperability among different mobile financial service providers which will eventually increase the penetration of digital financial services among women.

About the Author

Alexander Ayertey Odonkor is an economic consultant, chartered financial analyst, and a chartered economist with a keen interest in the economic landscape of countries in Asia and Africa.

Mid-Year Review: 'Ghana's economy moved from emergency room to the wellness cent...

Mid-Year Review: 'Ghana's economy moved from emergency room to the wellness cent...

Mid-Year Budget Review: Gov't earmarks GH¢400m to purchase high-occupancy buses

Mid-Year Budget Review: Gov't earmarks GH¢400m to purchase high-occupancy buses

Pursue economic transformation to address youth unemployment — Solomon Owusu tel...

Pursue economic transformation to address youth unemployment — Solomon Owusu tel...

Mid-Year Review: 'About 950,000 Ghanaians moved out of multidimensional poverty ...

Mid-Year Review: 'About 950,000 Ghanaians moved out of multidimensional poverty ...

Mid-Year Review: 'Gov't collected more taxes in 2025 despite abolishing e-levy, ...

Mid-Year Review: 'Gov't collected more taxes in 2025 despite abolishing e-levy, ...

Mid-Year Review: 'Economic recovery a result of superior economic management' — ...

Mid-Year Review: 'Economic recovery a result of superior economic management' — ...

Mid-Year Budget Review: 'NDC inherited an economy on its knees' — Finance Minist...

Mid-Year Budget Review: 'NDC inherited an economy on its knees' — Finance Minist...

Mid-Year Budget Review: It has been excellent six months — Joe Jackson

Mid-Year Budget Review: It has been excellent six months — Joe Jackson

Wontumi's 20-year sentence is ridiculous, punishment for his criticism of NDC — ...

Wontumi's 20-year sentence is ridiculous, punishment for his criticism of NDC — ...

KMA reports Police Officer over alleged gun threat during vehicle towing dispute

KMA reports Police Officer over alleged gun threat during vehicle towing dispute