1. Introduction and Background

In private sector-led market-oriented economies such as ours, predictability of key market prices such as the exchange rate is of critical importance. In the face of uncertainty, private enterprises are prone to be unwilling or unable to take the long view, preferring to wait and see.

The exchange rate of the Ghana cedi against, for example, the US dollar is quoted as the number of Ghana cedis required to purchase one US dollar (as also for the British pound sterling or the euro — the key major currencies in Ghana's international trade with the rest of the world). An unexpected change in the Ghana cedi/US dollar exchange rate could therefore have an impact on profitability of enterprises operating in the tradable sector of the economy — exporters and importers. It may call for corrective action such as an intervention by the Bank of Ghana (BOG).

In order for the appropriate corrective action to be taken, however, the BOG must determine whether the unexpected change is more the consequence of the policy stance in Ghana or of that of the US Federal Reserve — the corresponding central bank of the United States of America.

Determining the answer is difficult. One of the widely used approaches is to examine other exchange rates, for example, in respect of the British pound and the euro. Thus if the cedi is depreciating/appreciating — falling in value/rising in value — against all three key major currencies, it is reasonable to conclude that the unexpected or undesirable change in the value of the cedi requires corrective action by the Bank of Ghana.

This approach has given rise to the concept of the nominal effective exchange rate (NEER) — also referred to as the multilateral exchange rate. It is computed as the weighted average of the exchange rates of the Ghana cedi against the US dollar, the British pound, and the euro. The weights used by the Bank of Ghana are the shares of international trade — values of imports and exports — of Ghana with the respective trading-partner countries. The weight given to the US dollar is the sum of all the shares of trading partners other than the United Kingdom and the European Union. Weights are revised from time to time to reflect changes in trading patterns. To simplify the discussions here, however, we have used throughout the set of weights given by the BOG for 2009.

The NEER therefore measures the price of a “made-in-Ghana” good relative to the average price of the same good of our trading partners, computed on the basis of the share of international trade with each partner. It provides a much more comprehensive assessment of the cedi than using any one of the major currencies it interacts with. It provides a much more comprehensive assessment than comparing with any one of them. The interpretation of the NEER is that if it rises the cedi is weaker or depreciated against at least one of the currencies of our trading partners – we need more cedis to pay for imports. Similarly, a lower value of the NEER means the cedi is stronger or appreciated against at least one of the currencies of our trading partners — we need less cedis to pay for imports. In other words, domestic producers are placed at a disadvantage against importers in terms of profitability.

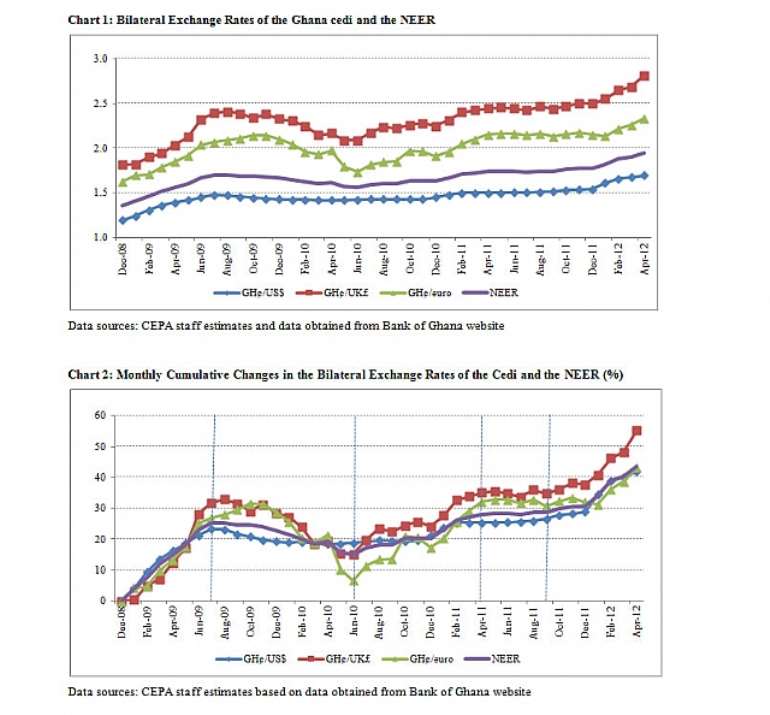

Chart 1 depicts the paths traced by the three major exchange rates and the NEER over the period to date of the present Administration. Chart 2 shows the monthly cumulative changes over the period. They serve to bring home the points in the discussions above.

As evident in Chart 2 above, the cedi depreciated against all three currencies in the first seven months of the period under review. This was on account of the continued persistence of the consequences of the excesses of election year 2008 arising from the political business cycle (PBC). Over the period of the 4th Republic to date, a four-year PBC has been in evidence with marked spending excesses in each election year followed by three years of relative austerity. It is in line with the needed corrective adjustment that the three-year stabilization program was agreed with the IMF under its Extended Credit Facility.

In respect of the Ghana cedi/US dollar exchange rate, a trend reversal occurred after July 2009 with the cedi appreciating almost immediately after the agreement on the stabilization program was signed. Against the British pound and the euro, however, the cedi continued to depreciate beyond July 2009. However, in response to the policy measures in the stabilization programme agreed with the IMF, trend reversals occurred in the Ghana cedi/British pound exchange rate in September 2009 and the Ghana cedi/euro exchange rate from November 2009.

It is discernible that exchange rate policies of trading partners together with the stabilization policies in the programme with the IMF were joint determining factors in the fortunes of the cedi. The appreciating pressure emanating from the stabilization programme had differential impact on the three major bilateral exchange rates.

Chart 2 again reveals dissimilarities in the fortunes of the cedi in the succeeding period of appreciation. The trough – end of the appreciation period – was again reached first against the US dollar in April 2010, followed by the British pound and the euro in June 2010.

We summarize the developments over the period on the basis of the NEER below:

i). In line with the political business cycle, the excesses of election year 2008 resulted in a continued depreciation from the second half of 2008 until July 2009. Thus in the months preceding the stabilization programme, the cedi depreciated by a cumulative 25.1 percent against the basket of three major currencies — the US dollar, the British pound, and the euro;

ii). The agreed stabilization program improved market perceptions favorably and with the positive revised expectations there was a trend reversal which sent the cedi appreciating against the basket, bringing the cumulative depreciation down to 22.7 percent by the end of the year 2009;

iii). The appreciation pressure persisted into the first three quarters of the following year 2010. Thus in the course of that period — up to September 2010 — the cedi appreciated by a cumulative 3.8 percent in spite of increased fiscal stimulus;

iv). A seasonal depreciating tendency has been observed commencing from the fourth quarter of the calendar year to the first quarter of the succeeding year. This has been attributed to the festivities and increased import activity of the yuletide. Thus in the fourth quarter of 2011 the cedi reversed trend and depreciated by a cumulative 1.9 percent against the basket. The depreciation intensified in the first quarter of 2011 — by a cumulative 5.7 percent;

v). As in the previous year, the cedi was relatively stable in the second and third quarters of 2011. Over the period, the total cumulative depreciation amounted to 1.1 percent compared to a cumulative appreciation of 0.4 percent the year before (on account of the stabilization package);

vi). The seasonal depreciation pressures of the yuletide then kicked against the basket, resulting in a cumulative depreciation of 1.6 percent in the fourth quarter of 2011. This was of the same order of magnitude as that of the corresponding quarter of 2010. In the first quarter of 2012 there was a strong intensification of depreciation pressure with the cedi suffering a cumulative depreciation against the basket of a whopping 7.6 percent compared to the 5.7 percent of the first quarter of the preceding year. The observed intensification of depreciation this year is seen to have been sparked off by a repeat of the PBC referred to earlier in respect of election year 2008; and

vii). Finally, for the period December 2008 to April 2012 as a whole, the cedi depreciated by a cumulative 43.4 percent against the basket of currencies in the NEER. It is noteworthy that for the seven-month period to July 2009 — the period prior to signing of the stabilization programme with the IMF — the cumulative depreciation amounted to 25.1 percent. Thus the larger share of the depreciation took place in the pre-stabilization period.

2. Structure of the Exchange Rate Market in Ghana

The foreign exchange market is small in size with only a few active players. The central bank is the most dominant player in the market and it is responsible for 90 percent of the total amount of transactions in the market. There are currently four identifiable segments of the market. These are:

• The interbank market where banks trade foreign exchange among themselves;

• Foreign exchange bureaux which serve individuals, tourists, SMEs, etc.;

• The corporate market through which transactions between banks and their customers are conducted; and

• The unofficial market which comprises of corporations that price their products / services at their own-determined exchange rate.

This means four market rates for each of the major currencies – the US dollar, the British pound, and the euro. In the discussion that follows we focus on the Ghana cedi / US dollar exchange rate in the first two markets.

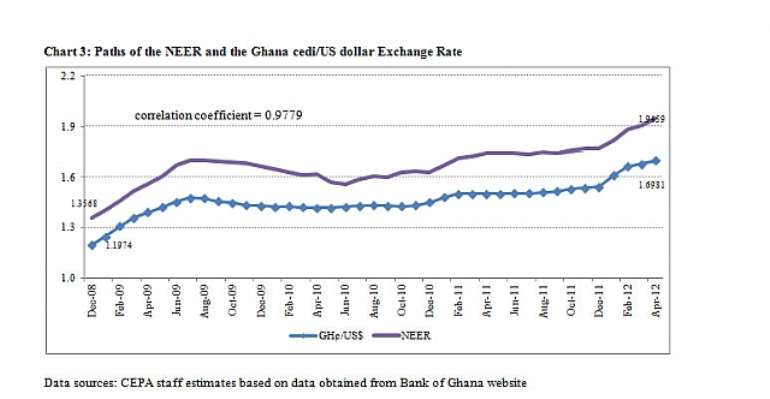

Chart 3, which is carved out of Chart 1, focuses on the paths of the NEER and the bilateral cedi/US dollar exchange rate. The chart shows a close association between the bilateral Ghana cedi / US dollar exchange rate and the NEER – i.e. they tend to trend together. The correlation coefficient between the two rates over the period under review is estimated at 0.98; suggesting that the cedi/US dollar exchange rate can be used as a fairly accurate indicator of the exchange rate policy stance of the BOG. This is quite a convenient finding given the considerations against using a single currency in the discussions above. The US dollar is the dominant transactions currency in global trade. It is the reference currency as well as the currency of intervention in domestic markets by the BOG.

At the beginning of the period, on average, for the month of December 2008, the exchange rate of the cedi against the US dollar in the interbank market was1.1974. In other words, on average GH¢1.1974 was needed to buy one US dollar during the month of December 2008. In that month, it cost an estimated GH¢1.3568 to buy one unit of the basket of currencies constituting the NEER — a ratio of 1.13. In other words it costs 1.13 times the amount of cedis required to purchase one US dollar in order to purchase one unit of the basket of currencies in the NEER.

At the end of the period under review, April 2012, on average, it cost GH¢1.6981 to buy one US dollar in the interbank foreign exchange market. Correspondingly, it cost an estimated GH¢1.9459 to buy a unit of the basket of currencies constituting the NEER — a ratio of 1.15.

These prices of foreign exchange confirm not only the high correlation between the cedi/US dollar exchange rate and the NEER over the period under review; they also bring out the conclusions of the regression analysis done at CEPA namely: that a unit of the basket of currencies cost, on average over the period December 2008 to April 2012, the equivalent of 1.14 times the cost of one US dollar.

The FX market is generally characterized by a structural imbalance in the demand and supply of foreign exchange which exerts depreciating pressure on the cedi and poses a constraint to the development of the foreign exchange market. In CEPA's view, this imbalance stems from a structural savings-investment gap that persists within the economy.

In a capital-poor developing country like Ghana, which also has underdeveloped financial markets, the investment/development needs far exceed the levels of domestic savings available to finance them. Under such circumstances, a current account deficit may be natural; and this might exert pressure on the currency to depreciate.

The large current account deficits are primarily financed by Official Development Assistance (ODA) and private capital flows. Thus, in addition to depreciation pressures on the cedi, there is also inherent vulnerability of the exchange rate to changes in market sentiment. The uncertainty and volatility in the flow of foreign capital, therefore, make it prudent for the BOG to aim at high holdings of international reserves. This is to enable it to buffer the potential pressures that may arise from maintaining an open current account.

3. Current Developments in the Foreign Exchange Market

After two years of relative stability, the cedi is facing intensified depreciation pressures and increased volatility. The pressures, which began in June 2011, became elevated in the last quarter of 2011 and further intensified in the first quarter of this year, especially in January and February.

Structural excess demand pressures in the foreign exchange market normally intensify in the last quarter of each year due to seasonal import demand for the holidays. However, the intensification in the first quarter of 2012 was not normal and as a result the depreciation of the cedi in January 2012 was at a much faster rate of 5.9 per cent compared to only 1.9 per cent in January 2011.

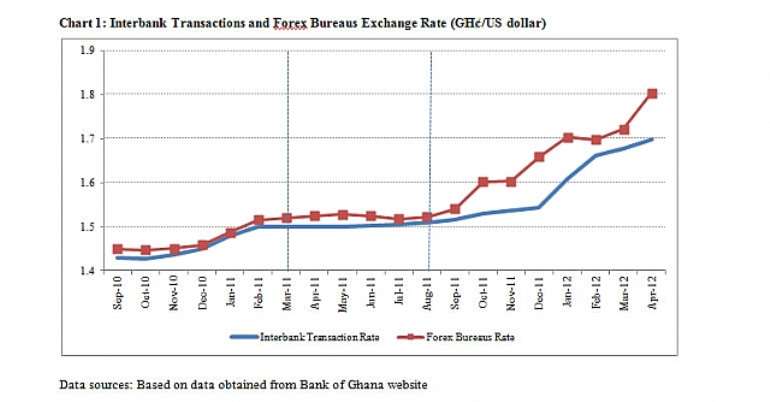

Evidence of seasonality in the movements of the foreign exchange rate is provided in Chart 1 above. The chart depicts the trend in the cedi / dollar exchange rate in the interbank and forex bureau markets from September 2010 to April 2012.

The abnormality of the depreciation that occurred from the beginning of this year to April 2012 can be seen in the steepness of the curves – strength of depreciation – and in the degree of divergence / spread between the interbank and forex bureau rates. The volatility in the first quarter of 2012 has been much higher than in comparative periods of other years. Similarly, the spread between the rates in the interbank and forex bureau markets has also widened.

The unusually strong demand for foreign exchange seen in the first quarter of 2012 can be attributed to the PBC and some of the consequences that have flowed out of that. In the recent period, the factors that have been at play in the foreign exchange market are the following:

The expansion in the Ghanaian economy

The acceleration in GDP growth – from 4.0 percent in 2009 – has resulted in an increase in economic activity and a higher demand for imports. CEPA estimates show that an increase in GDP by one percent generates a rise in imports by as much as 1.14 percent. Thus, the expansion in the economy has resulted in greater demand for foreign exchange and additional pressure on the cedi to depreciate.

Increased trade with China

The rising volume of trade with China has changed the demand patterns for foreign exchange. This is because imports from China are predominantly paid for in cash rather than with Letters of Credit (LCs) which spread out payments over a period of time. As a result, there has been an increased reliance on cash holdings of foreign exchange which has accentuated the seasonal pressures – particularly for the year-end holidays.

Much of the demand for foreign exchange in cash occurs in the forex bureau market. As such, the change in the pattern of trade towards more cash-based transactions, particularly with China, would have a greater impact on forex bureau rates. This could explain the relatively sharper depreciation seen in the forex bureau market and the resulting wider spreads between the forex bureau and interbank markets.

The reassessment of projections for oil production

The stable exchange rate – over the past two years, together with the entry into the oil era, provided good opportunities for foreign investors in the domestic bond market – high (even if falling) interest rates and expectations of currency appreciation. Consequently, the shortfalls in oil production and shipments – a local peak of 85,000 was reached followed by a decline to 70,000 bpd in December before recovering to 80,000 and a projected 90,000 bpd only by end-year 2012 – compared with the initial projection of 120,000 barrels per day by September 2011, coupled with the depreciation pressure of QIV, 11 and delay in raising interest rates in QIV, 11 worsened the risk / return outlook for fixed income debt instruments. Worsened prospects for investments negatively impact net foreign exchange inflows – as foreign investors pull out their investments – and put depreciating pressure on the cedi.

Misalignment in BOG foreign exchange cash flow

Accurate forecasting by the BOG of foreign exchange cash flows – i.e. potential demand and supply of foreign exchange in the market – guides its accumulation of foreign exchange reserves as well as its strategy for intervention (the timing and amount) in the foreign exchange market. The BOG's failure to anticipate the surge in demand for foreign exchange in the last quarter of 2011 – resulting from the rapid rise in imports, the early redemption by foreign investors of their investments in the domestic bond market, and the speculative activities of dealers and traders – therefore meant that it was unable to intervene in the market sooner or adequately enough to curb the depreciation in the cedi.

The ECF program target of 3 months of import cover further constrains the degree of intervention by the BOG as international reserves that are marginally above the threshold would limit how much foreign exchange the BOG can released onto the market.

The PBC and uncertainties about the upcoming 2012 elections

Historically, Ghana's experience in election years has been one of fiscal indiscipline and excessively large fiscal deficits that have resulted in macro instability – high inflation and a depreciation of the currency – in the ensuing years and that have called for painful fiscal adjustment programs to be implemented. World Bank studies have shown that, when compared to the years before, the fiscal balance in election years generally deteriorates by about 1.5 percentage points. Rising government expenditures – wages and subsidies – and public investments, combined with credit-fueled private consumption, raise aggregate demand and may result in rising imports, currency depreciation, and inflation.

Based on Ghana's experience in the 4th Republic with the political business cycle (PBC) and the uncertainties about this election year the foreign exchange market is pricing in a depreciation of the cedi. Unless compensated for by higher interest rates, as the BOG is doing, a depreciation of the cedi would imply a lower return on cedi-denominated investments and a worse risk/return outlook for investors. Foreign investors have, thus, begun to take the necessary precautionary steps to protect their investments. These include:

• Exiting their investments in the domestic bond market;

• Reducing uptake of new issues of securities

• Postponing the commencement of some projects to after the elections

The BOG announced in its February 2012 MPC Press Release that it has “experienced premature redemptions by some foreign investors” which have contributed to the cedi depreciation in January of this year. While foreign investors are only permitted to hold longer dated – 3 or 5 year – cedi denominated bonds, they are not bound to hold them to maturity. In other words they are free to sell these bonds at anytime as the BOG stands ready to rediscount them at a 'market rate'.

The reduction in net capital inflow that results from foreign investors reducing their holdings of domestic assets exerts depreciation pressure and increases the potential for a negative feedback cycle of depreciation.

Excess liquidity in the banking system and the Liquidity Overhang

Banks hold excess reserves when their total reserves – held at the central bank and in vault cash – exceed the required 9 percent of total deposits. When this is the case, the excess reserves may be loaned out to support private consumption or investments – resulting in inflation – or they may be used to purchase foreign exchange – causing depreciation.

The high terms of trade for cocoa and gold that increased foreign exchange inflows and boosted the international reserves of the BOG have also contributed to the excess liquidity in the system. This is because in building its foreign exchange reserves the BOG injects cedis into the system – this is to buy up the foreign currency. The additional cedis in the system, however, need to be mopped up to prevent them from causing inflation and subsequently depreciation of the currency.

Because of the high cost of OMO the BOG has been unable to effectively mop-up excess liquidity from the system. This has led to lower yields / interest rates on cedi assets and has resulted in the excess being channeled into the foreign exchange market; causing further depreciation in the cedi.

Speculation by FX traders

Speculative activity by foreign exchange traders trying to profit from the depreciation of the cedi has put additional pressure on the currency. Other market participants who are also trying to hedge against further depreciation have also contributed towards exacerbating the situation.

4. Mitigating responses by the BOG

The depreciation of the exchange rate remains a major source of concern for the BOG due to its possible consequences for inflation as well as its implication for the accumulation of international reserves. These concerns, thus, call for decisive policy measures to be taken to stem the fall in the cedi and to maintain the gains that have been made in macroeconomic stability.

The Bank of Ghana has taken a number of steps in an attempt to stabilize the currency. These measures have been aimed at:

• Mobilizing and injecting foreign exchange into the market;

• Withdrawing excess liquidity from the banking system; including through the enforcement of regulatory requirements

One way to reduce the excess demand for foreign exchange and hence the depreciation pressure on the cedi is to increase the supply of foreign currency on the market. To this end, the efforts made by the Bank of Ghana have included the following:

Drawing down of international reserves

The BOG has intervened in the foreign exchange market to sell foreign exchange, thereby increasing the supply of foreign exchange onto the market. These interventions have been costly to the BOG in terms of its accumulation of Gross International Reserves (GIR). In 2011, GIR had improved to US $5.4 billion from US $4.7 billion in 2010. By January 2012, however, GIR had declined to US $4.6 billion. Currently, international reserves are only marginally above the threshold of 3 months of imports stipulated by the ECF program with the IMF. Such slim buffers above the agreed program target, therefore, limit the BOG's flexibility to intervene further in the foreign exchange market.

The interventions by the BOG in the foreign exchange market have, however, not been sufficient to stem the downward trend in the cedi; and concerns have been raised by the central bank governor over the divergence in the rates quoted by traders operating in minor segments of the market. In light of these concerns, additional measures have been taken to increase the supply (and reduce the demand) of foreign exchange in the market and hence stabilize the currency.

Reduction in the net open positions of banks

In order to increase the supply of foreign exchange by banks to the market, the BOG has lowered the required single net open position (NOP) of banks from 15 percent to 10 percent of capital and the aggregate NOP from 30 percent to 20 percent. The NOP is the difference between a bank's foreign currency assets and foreign currency liabilities and it can be calculated for assets and liabilities in a single currency (single currency NOP), or for assets and liabilities in all currencies (aggregate NOP). A reduction in the required NOP, therefore, would imply that net foreign currency assets in excess of the requirement would have to be supplied to the market. The increased supply of foreign exchange onto the market would then dampen demand pressures and attenuate the pressure on the cedi to depreciate.

Revision in the Application of the Statutory Reserve Requirement of Banks

For prudential purposes, the BOG requires that 9 percent of bank deposits, both local currency and foreign currency, be held as reserves at the central bank. Previously, reserve balances were held in their corresponding currencies – i.e. required reserves on cedi deposits were held in cedis and those on foreign currency deposits were held in foreign currency. In its press release of April 27, 2012, however, the BOG announced that all banks will now be required to maintain the mandatory 9 percent reserve requirement on domestic and foreign deposit liabilities in Ghana cedis only. This requirement to hold all reserves in local currency is aimed at freeing up foreign exchange locked in reserves, thereby increasing the supply of foreign exchange onto the market. The increase in supply will satisfy some of the excess demand in the market, and depreciation pressures on the cedi will ease.

Other measures that have been taken by the BOG have been targeted at withdrawing excess liquidity from the system – thereby making less cedis available to chase after foreign exchange. These measures will result in a better alignment of monetary policy with exchange rate policy. The measures include:

Increasing in the Monetary Policy Rate (MPR)

After months of steady declines in the MPR, the Monetary Policy Committee, in February 2012, increased the MPR by a hundred basis points from 12.5 percent to 13.5 percent; and further to 14.5 percent in April 2012. The increase in the MPR, which translates into increases in other market interest rates such as Treasury bills and notes, makes cedi assets an attractive alternative to holding foreign currency and as such acts as a means of absorbing excess liquidity in the system and, therefore, reducing the demand for foreign exchange.

Higher yields on Treasury bonds (3 and 5-year bonds) that make them attractive investments to foreign investors also serve as a means of mobilizing foreign exchange to build up the international reserves of the BOG.

Provision of cedi cover for vostro balances of Deposit Money Banks

Vostro accounts are accounts maintained by foreign banks with banks in Ghana that allow the foreign banks to buy local currency. Foreign currency deposits into these accounts are thus meant to represent 'orders' by foreign banks to buy Ghanaian cedis – for transactional or investment purposes. Unless the order for cedis are placed, however, the available foreign exchange in these accounts are not supplied onto the market and can, therefore, be used as a means of speculative attack on the cedi.

BOG regulatory laws require that all banks provide 100 percent cedi cover for their vostro balances, to be maintained at Bank of Ghana; and as of May 1st, 2012, this requirement will be enforced by the BOG. The provision of a 100 percent cedi cover for vostro balances not only reduces the potential for speculative attacks on the cedi, but also acts as means of withdrawing excess liquidity from the system; which otherwise may go into the goods or foreign exchange market, driving up inflation and causing further depreciation in the cedi.

Re-introduction of BOG Bills

The key tool of monetary policy used by the BOG for liquidity management is open market operations (OMO) – the buying and selling of Treasury Bills to manage the supply of money in the system.

In the recent past, the BOG had used Government Treasury bills to perform OMO. As of May 1 of this year, however, the BOG will be using its own bills for OMO. The re-introduction of the BOG bills – with maturities of 30, 60, and 270 days – offers a broader array of instruments for investors to choose from. It also enhances the transparency of monetary policy by providing a clear distinction between the BOG's conduct of OMO, and its actions to satisfy the borrowing requirements of government. Because previously the BOG used Treasury bills for both OMO and borrowing for Government, the amount of T-bills issued for OMO and for Government was not known to the public. The use of BOG bills solely for OMO purposes will, therefore, provides a better indication of monetary policy and fiscal policy requirements.

Despite the increased transparency in monetary policy, the re-introduction of BOG bills still leaves the issue of OMO costs unaddressed. Government borrowing costs are the responsibility of the Ministry of Economic and Financial Planning, but the costs of OMO are borne by the BOG. Thus, unless the BOG is adequately resourced to perform its monetary policy role, high OMO costs will continue to prevent effective sterilization – leaving excess liquidity in the system.

5. Summary

The commencement of oil production in Ghana had generated concerns about currency appreciation and the resulting Dutch Disease – the loss of international competitiveness of Ghanaian exports. However, after a full year of oil production, the challenge facing the economy is not one of an appreciating currency, but a depreciation which, if inadequately unaddressed, has the potential of reversing hard won gains in economic stability and inflation.

Seasonal factors that affect the demand for imports usually cause the value of the cedi to fall from about the last quarter of the year into the first quarter of the following year. The depreciation that occurred in the first quarter of this year, however, has been exceptional. The unusually high demand for imports – due to the expansion in the economy and increased trade with China – has been a contributing factor. However, the PBC and the uncertainties surrounding this election year have also had negative consequences for the value of the Ghana cedi.

The unusually high demand for imports, unanticipated withdrawals by foreign investors of their investments in the domestic bond market and speculation by dealers and foreign exchange traders have negatively affected the cash flow of the BOG; drastically reducing the foreign currency reserves of the BOG. Further depreciation pressure has also come from the excess liquidity that exists in the system.

In spite of the challenges, the medium term prospects for the economy remain strong. Oil production is expected to rise above the current level of 80 barrels a day; and as has been reported by the Ghana Investment Promotion Center (GIPC) foreign direct investment (FDI) inflows to Ghana for the first quarter of 2012 have recorded significant growth of US $ 979.85 – a 178.56 percent increase above the US $351.75 recorded in the first quarter of 2011.

The BOG's efforts to stabilize the cedi have been commendable. These efforts have been targeted at increasing the supply of foreign exchange into the market and at absorbing some of the excess liquidity from the system; and they have resulted in relative stability in the cedi. Given the uncertainties associated with this election year, however, Government must also play a role in alleviating the fears of investors and the pressures that their speculative activity can have on the cedi. This can be done by a credible commitment to fiscal responsibility and expenditure accountability that would ultimately lead to good governance.

Two sustain gun wounds in Mankrong Nkwanta robbery

Two sustain gun wounds in Mankrong Nkwanta robbery

Military personnel deployed to Bawku vehicle crashed STC bus at Nkenkesu

Military personnel deployed to Bawku vehicle crashed STC bus at Nkenkesu

Bohyen chief appeals for fire station to improve emergency response

Bohyen chief appeals for fire station to improve emergency response

Father jailed 20 years for incest with 17-year-old daughter

Father jailed 20 years for incest with 17-year-old daughter

Court jails man 10 years for defiling seven-year-old boy

Court jails man 10 years for defiling seven-year-old boy

'Africa remains rich in promise; our task is to ensure that promise matures into...

'Africa remains rich in promise; our task is to ensure that promise matures into...

Justin Kodua Launches Bid to Retain NPP General Secretary Post Ahead of Crucial ...

Justin Kodua Launches Bid to Retain NPP General Secretary Post Ahead of Crucial ...

Zanetor Demands Continental Action: ‘Africa Cannot Progress While Women Live in ...

Zanetor Demands Continental Action: ‘Africa Cannot Progress While Women Live in ...

Mahama assures transfer of UGMC to University of Ghana

Mahama assures transfer of UGMC to University of Ghana

Wontumi told me he would get 20year jail term before judgment was read – Lawyer ...

Wontumi told me he would get 20year jail term before judgment was read – Lawyer ...