On the 15th of December, 2018, I published an article on the ‘Future of the Ghanaian bond market’ where I indicated that the Ghanaian capital market has great prospects and a huge opportunity thereof.

Similarly, on the 7th May 2019, I further published another article on my joyonline.com and Business Financial Times focusing on ‘Funding MMDA's Infrastructure Development with Municipal Bonds in Ghana’. These articles shed some light on how capital markets could help in economic development through the implementation of prudent financial management.

In recent times, the international capital market has accepted risk on Sovereign issuances. Ghana has issued billions worth of long-dated maturity bonds running into 2051 tenors.

In April 2019, the Government of Ghana through the Ministry of Finance went to the market and successfully priced its $3bn Eurobond issuance which was oversubscribed by 7 times more. All these developments to an extent give an idea that there is appetite and comfort from investors.

However, amidst all these good developments, how do we leverage on this to deepen the domestic corporate bond market in Ghana, tapping into the Emerging Market (EM) investors who are beginning to take key interest and monitoring African issuances.

There are several reasons why most corporate firms in Ghana have not tapped into either the domestic cedi bond market or the Eurobond Market.

The Cedi bond market will offer corporates the opportunity to raise funding in a locally denominated currency in Ghana.

The Eurobond market is also a bond issued in one`s country that is traded outside of that country. To issue bonds in the domestic market or the international market largely depends on corporates’ use, sources of cash and size of the transaction.

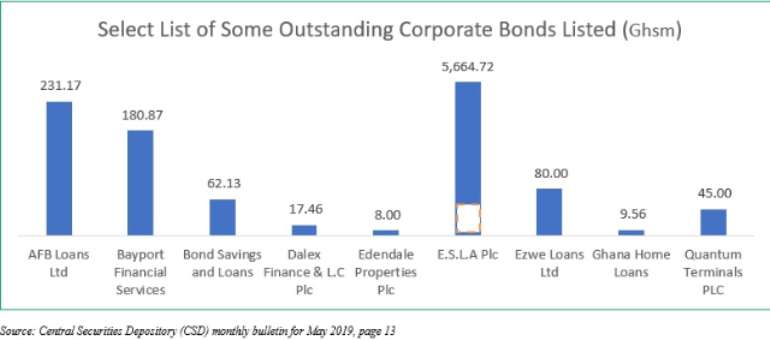

Currently, there are nine (9) corporate clients who have issued corporate bonds amounting to about GHS7.3bn ( USD1.5bn) with E.S.L.A Plc accounting for over 90% (Ghs5.66bn) of the issuance. Compared to other markets, there is still room for improvement as it suggests underdevelopment. It is interesting to note that, in aggregate, the face value of outstanding debt held under the custody at the Central Securities Depository (CSD) increased by 18.43% to Ghs81bn in 2018 from Ghs68.4bn in 2017.

Government of Ghana securities formed about 77% of the outstanding stock at the end of the year. Securities issued by Bank of Ghana, Cocobod and these corporate firms also constituted closed to 8%, 7% and 8% respectively of the outstanding stock in 2018.

A lot of corporates today have huge exposures on their balance sheets due to their medium to long-term working capital needs. This has resulted in huge and high-interest payments coupled with cash flow volatility. The question will always arise; should companies raise funding through bank loans or through debt capital market? For corporates looking for cheaper sources of funding for expansion, mergers and acquisition as well as working capital needs, the bond market may be highly recommended.

General market conditions

Globally, low rates coupled with limited supply and high investor cash holdings have led to a return to “hunt for yield” by some investors. Accordingly, investors are keen to deploy liquidity despite recent market volatility. Banks are generally more likely to access the foreign markets before other real sectors of the economy.

It has become the trend for all EM for Financial Institutions (FI) to follow sovereigns into the Eurobond market and then the companies. The key thing to note is that there are huge diversified investors who are ready to provide long term and ‘stable’ source of financing to help companies grow. Are companies ready?

Why must corporate issue Bonds?

· Bonds usually have longer maturity (5yr-10yr/more) and larger funding size due to the more liquid global or domestic investor pool

· There is no amortization requirement which reduces the pressures on short term cashflow

· Bonds help in extending the maturity profile of the debt

· It widens the issuer’s institutional investor base which will benefit future equity and capital markets activities

· Usually, incurrence covenants provide greater operational flexibility and mitigate any liquidity concerns.

What do investors want?

The ideal corporate issuer who wants to issue a bond should consider that, an investor; be it domestic or international looks out for some key metrics.

· Investors prefer to see the right story of the company, the right price of the bond so that they are not worse off, good credit quality and relatively large amount (benchmarked around USD350m - USD500m).

· Market prefers sound financial record and stable earnings over a period (Minimum EBITDA of USD50m and above) with a good leverage 3.5x (5x recommended for capital intensive projects companies like Airport, Seaport etc

· Market prefers issuers who are receptive to public disclosures and this is based on the fact that bonds are public securities and require extensive disclosures for a good public profile prepared by legal counsel.

· Investors look for historical audited financials for the last 3years for 144a deals formats and 2years for Reg S deals formats. The 144a deal formats option provides the issuer with increased distribution to investors within the United State of America (USA) and targets Qualified Institutional Buyers (QIB). Reg S format are bonds not issued to the USA but still watched by the SEC and falls within the regulation S exemptions.

· Investor prefer issuers with an internationally recognized audit firms such as KPMG, PricewaterhouseCoopers, Deloitte and Touché, Ernest and Young etc)

· Market prefers Issuers with good Credit Ratings. Credit quality to a large extent determines the financial flexibility and provides issuers larger investor base, diversified funding, enhanced liquidity and sometimes better pricing. Whenever credit ratings go down, some investors may consider selling their bonds. Preferred raters include Standard and Poor’s, Fitch, Moody etc. The basic rationale for corporate rating are to examine the cash flows, level of leverage, hedging strategy, auditor’s opinion, changes in ownership structure -M&A etc.

Timing to Market

This has to do with when to go the market and whether investors are ready for you. Getting the timing right to market matters. For example, in an election year, since the outcomes of most elections are usually unknown, a lot of institutional investors shy away from either sovereign or corporate bonds as they remain sceptical.

More importantly, it is crucial for issuers to embark on a deal and non-deal roadshows before debut issuance. This enhances investor familiarity with Issuer ahead of a potential bond and also allows investors an “early look” and an opportunity to front-load their preliminary credit analysis. Early investor engagement can generate goodwill with accounts and has the potential to generate early demand ahead of the transaction (thereby reducing execution risk).

The role of banks in the process

Banks play an important role in supporting corporate bond issuance process. This involvement cannot be underestimated. Some banks have access to a wide range of investors both local and globally and support with the distribution end to end. Corporates may start speaking to their bankers today to understand the process of debt capital market issuance. The banks are appointed as Lead arrangers/managers or book runners.

For instance, a global bank like Standard Chartered Bank (SCB), a leading bond book runner with extensive footprint and unique access to EM investors, based on unparalleled distribution network can lead any corporate on a series of non-deal and deal roadshows to formally introduce a corporate before a debut issuance. SCB also has a very experienced DCM team across Africa, Asia and the Middle East.

Potential challenges and recommendations.

Most foreign investors would not invest in domestic corporate bonds because they see the market to be illiquid and availability of FX is not guaranteed when they need to exit. This calls for managers of the economy to address the fast depreciation of the local currency against the major trading currency.

The local cedi bond market has over 85% of local investors who are usually Fund Managers, Insurance and others, issuers should ensure that the funds are used for the intended purposes.

Issuers should also ensure that there is no default on obligations (i.e. coupon payment on maturity date) and that any recorded event of default has a very serious ripple effect on the entire bond market. There is, therefore, the need to ensure good corporate governance and further ensure that good accounting practices are strictly adhered to.

The stakeholders within the capital market must continue the dialogue and come out with practical and feasible solutions to deepen the industry.

In summary, we can learn some few things from the US market where corporate borrowers financed 67% of their needs through the bond market and 33% via the loan market. Ghanaian Companies and management may prefer to be more receptive to capital market-based financing. Again, there is high investor demand for corporate bond issuance fuelled by high yields. There is, therefore, the need to take advantage of investor needs. The remarkable growth in debt capital markets points to a structural change in corporate financing. This is the time, let`s increase corporate issuance in Ghana

Credit: Central Securities Depository (CSD) 2018 annual report, Ghana Stock Exchange, Netufo Tayo, Miriam Amoako

Disclaimer: The views expressed are personal views and doesn’t represent that of the hotel mentioned, the institution the writer work for or the publishing firm.

About the writer

Carl Odame-Gyenti is a third-year PhD (Financial Management) candidate, a Finance and Telecom enthusiast, managing local and global Investors, Intermediaries, Non-Bank Financial and Financial Institution relationships with an international bank in Ghana. He has embarked on several international assignments in London, Singapore, Dubai, Kenya, Nigeria and Southern African markets. He has a passion for youth and community development.

Former Kotoko Player George Asare elected SRC President at PUG Law Faculty

Former Kotoko Player George Asare elected SRC President at PUG Law Faculty

2024 elections: Consider ‘dumsor’ when casting your votes; NPP deserves less — P...

2024 elections: Consider ‘dumsor’ when casting your votes; NPP deserves less — P...

You have no grounds to call Mahama incompetent; you’ve failed — Prof. Marfo blas...

You have no grounds to call Mahama incompetent; you’ve failed — Prof. Marfo blas...

Don’t exchange your life for wealth; a sparkle of fire can be your end — Gender ...

Don’t exchange your life for wealth; a sparkle of fire can be your end — Gender ...

Ghana’s newly installed Poland train reportedly involved in accident while on a ...

Ghana’s newly installed Poland train reportedly involved in accident while on a ...

Chieftaincy disputes: Government imposes 4pm to 7am curfew on Sampa township

Chieftaincy disputes: Government imposes 4pm to 7am curfew on Sampa township

Franklin Cudjoe fumes at unaccountable wasteful executive living large at the ex...

Franklin Cudjoe fumes at unaccountable wasteful executive living large at the ex...

I'll 'stoop too low' for votes; I'm never moved by your propaganda — Oquaye Jnr ...

I'll 'stoop too low' for votes; I'm never moved by your propaganda — Oquaye Jnr ...

Kumasi Thermal Plant commissioning: I pray God opens the eyes of leaders who don...

Kumasi Thermal Plant commissioning: I pray God opens the eyes of leaders who don...